Emergency Loans For 500 Credit Score

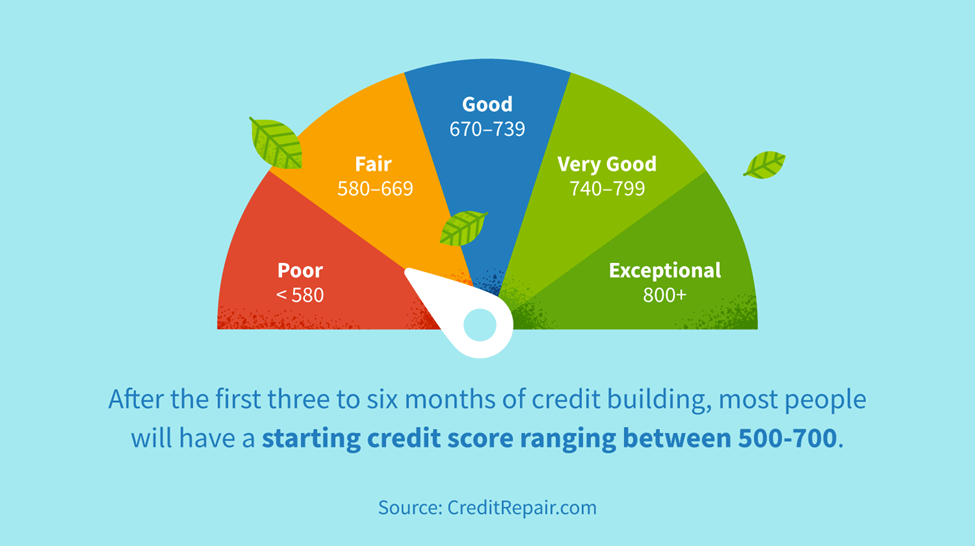

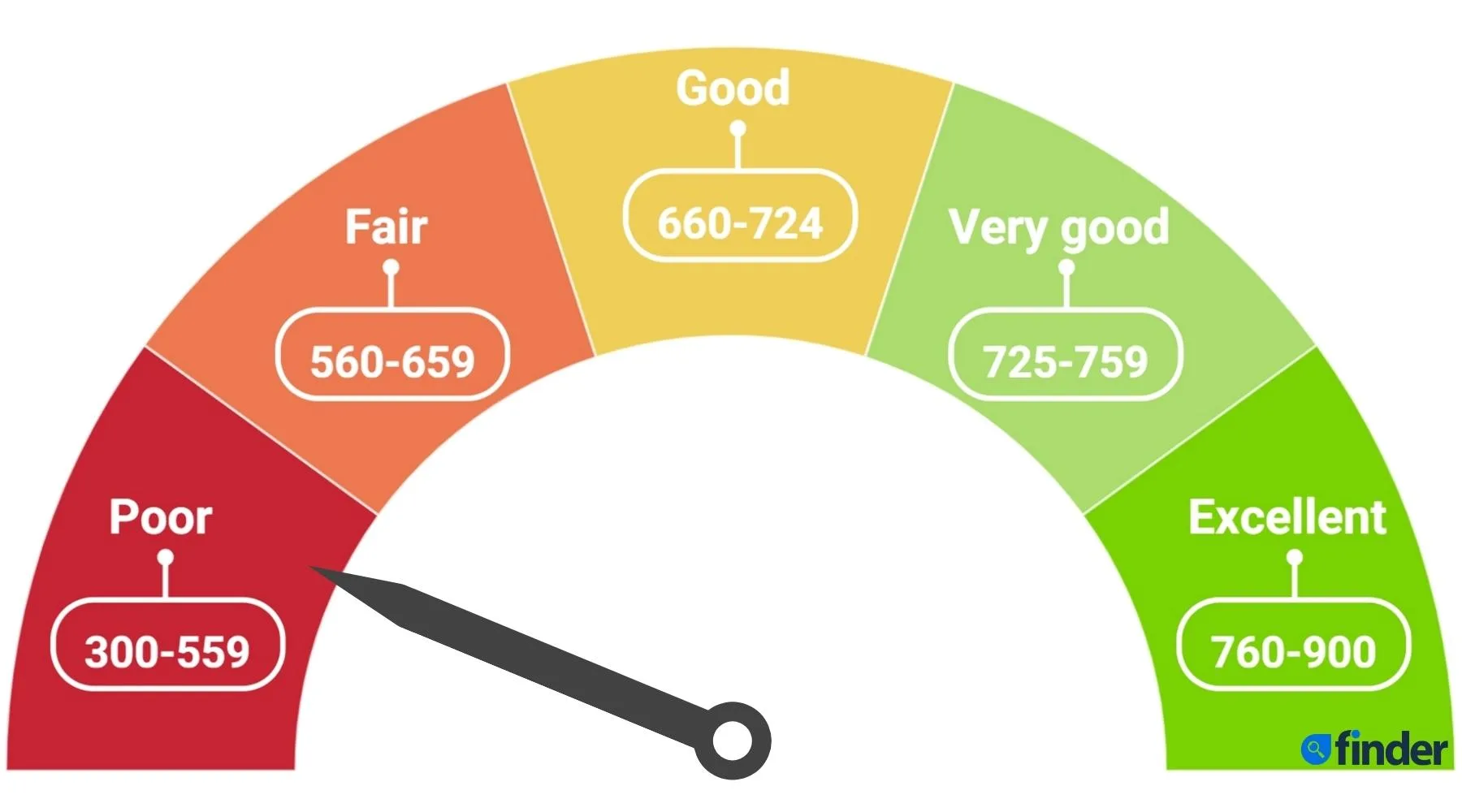

Securing a loan with a credit score of 500 can be challenging, particularly when facing a financial emergency. A 500 credit score falls within the "poor" or "very poor" range, signaling to lenders a higher risk of default. This article provides an overview of emergency loan options potentially available to individuals with a 500 credit score, along with considerations and alternatives.

Understanding the Landscape of Emergency Loans

Emergency loans are designed to provide quick access to funds to cover unexpected expenses such as medical bills, car repairs, or urgent home repairs. Traditional lenders, such as banks and credit unions, typically require a higher credit score for loan approval. Therefore, individuals with a 500 credit score often need to explore alternative lending sources.

Types of Emergency Loans to Consider

Several types of loans may be accessible, though they often come with higher interest rates and less favorable terms compared to loans offered to borrowers with good credit.

Must Read

- Payday Loans: These are short-term, high-interest loans designed to be repaid on the borrower's next payday. While easily accessible, they carry extremely high interest rates and fees, potentially leading to a cycle of debt. It is crucial to understand the full cost of a payday loan before agreeing to the terms.

- Installment Loans: These loans offer a fixed amount of money that is repaid in regular installments over a set period. Some installment loan lenders cater to borrowers with lower credit scores. However, interest rates are typically higher than those offered to borrowers with good credit.

- Secured Loans: These loans are backed by collateral, such as a vehicle or other valuable asset. The collateral reduces the lender's risk, potentially increasing the chances of approval, even with a low credit score. If the borrower fails to repay the loan, the lender can seize the collateral.

- Credit Union Loans: Credit unions may offer loans with more favorable terms than traditional banks, especially to their members. If you are a member of a credit union, it is worth exploring their loan options. Some credit unions offer "payday alternative loans" (PALs) which are structured to be more affordable than typical payday loans.

- Online Lending Platforms: Many online lenders specialize in providing loans to borrowers with less-than-perfect credit. These platforms often offer a faster application process and may be more willing to approve loans for individuals with a 500 credit score. However, it's vital to thoroughly research the lender and compare interest rates and fees.

Factors Affecting Loan Approval

Even with alternative lenders, several factors influence the likelihood of loan approval for someone with a 500 credit score:

- Income: Lenders want to ensure that borrowers have sufficient income to repay the loan. Proof of stable income is essential.

- Employment History: A consistent employment history demonstrates financial stability.

- Debt-to-Income Ratio (DTI): This ratio compares monthly debt payments to gross monthly income. A lower DTI indicates a better ability to manage debt.

- Collateral (for Secured Loans): The value and condition of the collateral will influence the loan amount and approval.

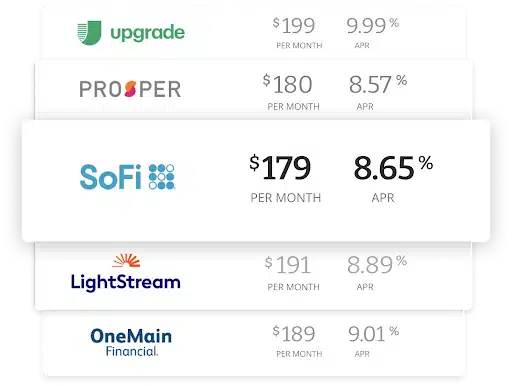

Navigating High Interest Rates and Fees

Borrowers with a 500 credit score should expect to pay significantly higher interest rates and fees compared to those with good credit. Before accepting a loan, carefully review the following:

- Annual Percentage Rate (APR): The APR represents the total cost of the loan, including interest and fees, expressed as an annual rate. Compare APRs from different lenders to find the most affordable option.

- Fees: Be aware of origination fees, late payment fees, prepayment penalties, and other potential fees.

- Loan Term: The length of the loan term affects the total amount of interest paid. Shorter loan terms typically result in lower total interest costs but higher monthly payments.

Important Note: Always read the loan agreement carefully before signing. Ensure you understand all the terms and conditions, including the repayment schedule, interest rate, and any associated fees. If anything is unclear, ask the lender for clarification.

Alternatives to Emergency Loans

Before resorting to a high-interest emergency loan, explore alternative options:

- Negotiate with Creditors: Contact creditors to explain your situation and ask if they can offer a payment plan or temporarily reduce your payments.

- Seek Assistance from Charities: Local charities and non-profit organizations may offer financial assistance for specific needs, such as rent, utilities, or food.

- Borrow from Friends or Family: If possible, consider borrowing money from friends or family. Be sure to establish clear repayment terms to avoid damaging relationships.

- Sell Unwanted Items: Selling unwanted items online or at a pawn shop can generate quick cash.

- Consider a Credit Counseling Agency: These agencies can help you create a budget, manage debt, and explore debt relief options.

Improving Your Credit Score

While addressing immediate financial needs is crucial, it's equally important to focus on improving your credit score for long-term financial health. Here are some steps you can take:

- Pay Bills on Time: Payment history is the most significant factor in determining your credit score.

- Reduce Credit Card Balances: Aim to keep credit card balances below 30% of the credit limit.

- Dispute Errors on Credit Reports: Review your credit reports regularly and dispute any inaccuracies.

- Become an Authorized User: Ask a friend or family member with good credit to add you as an authorized user on their credit card.

- Consider a Secured Credit Card: This type of credit card requires a cash deposit as collateral, which can help you build credit.

Avoiding Predatory Lending

Individuals with poor credit scores are often targeted by predatory lenders who offer loans with extremely high interest rates and fees. These loans can trap borrowers in a cycle of debt. Be wary of lenders who:

- Guarantee approval regardless of credit score.

- Charge excessively high interest rates and fees.

- Use aggressive or deceptive marketing tactics.

- Do not clearly disclose loan terms.

- Pressure you to borrow more than you need.

Always research lenders thoroughly and check their reputation with the Better Business Bureau (BBB) and online reviews.

The Importance of Financial Literacy

Improving financial literacy is crucial for managing finances effectively and avoiding debt traps. Consider taking financial education courses or consulting with a financial advisor to learn about budgeting, saving, and credit management.

Conclusion

Obtaining an emergency loan with a 500 credit score is challenging but not impossible. While options like payday loans, installment loans, and secured loans may be available, they often come with high interest rates and fees. Carefully consider all alternatives, such as negotiating with creditors, seeking assistance from charities, or borrowing from friends or family. Improving your credit score is essential for long-term financial stability and accessing more favorable loan terms in the future. Prioritizing financial literacy and avoiding predatory lending practices will contribute to better financial outcomes.