Oceanfirst Bank Home Equity Loan Rates

Okay, so you’re thinking about a home equity loan from OceanFirst Bank, huh? Smart cookie! You’ve got equity sitting there, like a pile of cash just…waiting. But before you dive headfirst into renovations, debt consolidation, or that dream vacation (Tahiti, maybe?), let's chat about those OceanFirst Bank home equity loan rates. Because let’s be honest, that’s the real nitty-gritty, isn’t it?

Think of me as your friendly neighborhood finance guru, armed with a lukewarm latte and a whole lot of (hopefully) helpful info. I'm not a financial advisor, mind you! Just a pal sharing what I've dug up. So, grab your own beverage of choice, settle in, and let's decode this rate situation together.

What Exactly Is a Home Equity Loan Anyway? (Just a Quick Refresher!)

Alright, alright, some of you might be thinking, "Duh, I know what a home equity loan is!" But for those who are a little fuzzy (no judgment!), here's the super-simplified version: It's basically borrowing money against the equity you've built up in your home. That’s the difference between what your home is worth and what you still owe on your mortgage. Like a second mortgage, but cooler… mostly because you can use the money for, well, pretty much anything! Think of it as your home lending you some cash. Pretty generous, right?

Must Read

You get the loan as a lump sum, and then you pay it back over a set period, with interest. And that's where those lovely (or not-so-lovely) OceanFirst Bank home equity loan rates come into play. It's like the price you pay for borrowing that sweet, sweet equity. Got it? Good! Let’s move on.

Okay, Spill the Tea: OceanFirst Bank Home Equity Loan Rates

So, here's the thing: getting a specific rate for you without actually applying is a bit like trying to predict the weather a month from now. It's tricky! Rates are always changing based on, well, a million different things. The economy, the Fed, the phase of the moon… okay, maybe not the moon phase. But you get the idea!

OceanFirst Bank, like most lenders, doesn't just publish a single, universal rate and say, "Here you go, everyone!" They look at a bunch of factors specific to your situation. But, fear not! We can still get a general idea of what to expect.

Here’s what typically influences those rates (and what OceanFirst will likely consider):

- Your Credit Score: This is the big one, folks. The higher your credit score, the lower your rate will likely be. It's like the golden ticket to interest rate paradise. Aim for a score in the "excellent" range (740+) for the best possible rates. If your credit score needs some TLC, don't despair! There are things you can do to improve it. But that’s a chat for another day.

- Your Loan-to-Value (LTV) Ratio: This is fancy talk for how much you're borrowing compared to the value of your home. If your home is worth $500,000 and you owe $200,000 on your mortgage, you have $300,000 in equity. If you want to borrow $50,000, your LTV would be 50% ([$200,000 + $50,000] / $500,000). The lower your LTV, the better your rate. Basically, the more equity you have, the less risky you are to the bank. And less risky = better rates!

- The Loan Amount: Sometimes, the amount you borrow can affect the rate. Larger loans might have slightly different rates than smaller loans. Why? Well, banks have their reasons. Let's just say it's complicated and leave it at that.

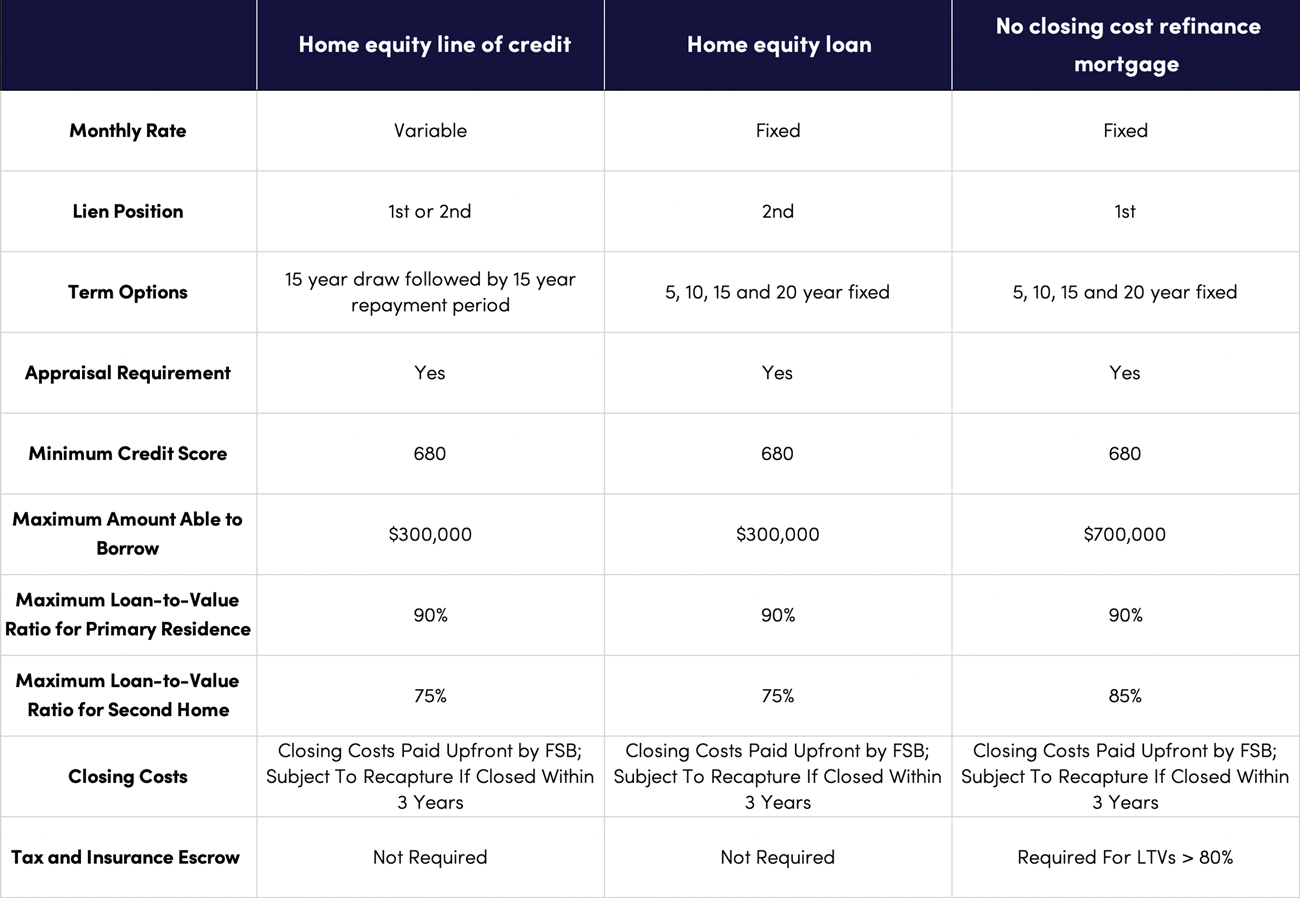

- The Loan Term: This is how long you have to pay back the loan. Shorter terms usually mean lower interest rates, but higher monthly payments. Longer terms mean lower monthly payments, but you'll pay more interest over the life of the loan. It's a trade-off! Which do you prefer? Pay more now and less later, or pay less now and more later?

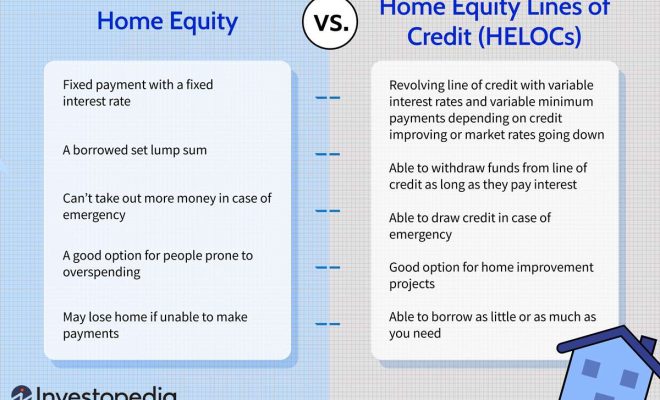

- The Type of Rate (Fixed vs. Variable): This is a huge one! A fixed-rate means your interest rate stays the same for the entire loan term. Predictable and stable! A variable-rate means your interest rate can go up or down depending on market conditions. Potentially lower starting rate, but…risky business! We'll dive deeper into this in a minute.

- Current Market Conditions: Interest rates are influenced by the overall economy and what's happening in the financial world. When the economy is booming, rates tend to be higher. When things are a little shaky, rates might be lower. It's a constant dance!

Fixed vs. Variable Rates: A Head-to-Head Showdown!

Okay, let's break down the fixed vs. variable rate thing a little more. This is important! It's like choosing between a steady, reliable friend (fixed) and a fun, unpredictable adventurer (variable).

Fixed-Rate Home Equity Loans: The Predictable Pal

Pros:

- Predictability: Your interest rate stays the same for the entire loan term. No surprises! You know exactly what your monthly payments will be, which makes budgeting a breeze.

- Peace of Mind: No need to worry about interest rates suddenly spiking and your payments going through the roof. Whew!

Cons:

- Potentially Higher Starting Rate: Fixed rates often start out a little higher than variable rates. You're paying for that predictability!

- Missed Opportunity?: If interest rates go down, you're stuck with your original rate. Sad trombone!

Variable-Rate Home Equity Loans: The Adventurous Spirit

Pros:

- Potentially Lower Starting Rate: Variable rates often start out lower than fixed rates. Woohoo!

- Potential Savings: If interest rates decrease, your payments could go down. Extra money for that dream vacation!

Cons:

- Unpredictability: Your interest rate can go up (or down) depending on market conditions. Yikes!

- Risk of Higher Payments: If interest rates rise, your monthly payments could become significantly higher. Budgeting nightmare!

- Often Tied to an Index: Variable rates are usually tied to a benchmark interest rate, like the Prime Rate or the LIBOR (though LIBOR is being phased out). So, you're at the mercy of whatever that index does!

Which one is right for you? It depends on your risk tolerance, your financial situation, and your crystal ball (kidding... mostly!). If you like predictability and can't handle the thought of fluctuating payments, a fixed-rate is probably the way to go. If you're a bit of a gambler and think interest rates might go down, a variable-rate could be a good option. But be warned: it's a gamble! So always carefully consider the risks.

How to Snag the Best OceanFirst Bank Home Equity Loan Rate: Tips and Tricks!

Alright, so you're armed with all this knowledge. Now, how do you actually get the best possible OceanFirst Bank home equity loan rate? Here are a few tips:

- Shop Around: Don't just settle for the first rate you see! Get quotes from multiple lenders (including other banks and credit unions) to see who offers the best deal. It's like comparison shopping for a new car – you wouldn't buy the first one you see without looking at other options, right?

- Improve Your Credit Score: This is the most important thing you can do. Pay your bills on time, keep your credit card balances low, and avoid opening too many new accounts at once. A higher credit score = lower interest rates = happy dance!

- Lower Your LTV: If possible, try to pay down your mortgage a bit before applying for a home equity loan. The more equity you have, the better your rate will be. Plus, it's always a good feeling to owe less on your house!

- Negotiate: Don't be afraid to haggle! Once you have a few quotes, see if OceanFirst Bank is willing to match or beat the lowest rate you've found. The worst they can say is no. And even if they say no, you haven't lost anything.

- Consider a Shorter Loan Term: If you can afford the higher monthly payments, a shorter loan term will usually result in a lower interest rate. You'll also pay off the loan faster and save money on interest in the long run. It's a win-win!

- Look for Discounts: Sometimes, banks offer discounts for things like being a long-time customer, having a checking account with them, or enrolling in automatic payments. Ask about any potential discounts that might be available. Every little bit helps!

- Read the Fine Print: Before you sign anything, make sure you fully understand all the terms and conditions of the loan. Pay attention to things like prepayment penalties, late fees, and any other hidden costs. Knowledge is power!

Beyond the Rate: Other Fees to Consider

Don't just focus on the interest rate! There are other fees associated with home equity loans that you need to be aware of. These can include:

- Application Fees: Some banks charge a fee just to apply for the loan.

- Appraisal Fees: You'll likely need to get your home appraised to determine its current value.

- Closing Costs: These can include things like title insurance, recording fees, and attorney fees.

- Origination Fees: This is a fee that the bank charges for processing the loan. It's usually a percentage of the loan amount.

Make sure you factor these fees into your calculations when comparing different loan offers. A slightly lower interest rate might not be worth it if the fees are significantly higher!

Okay, So... What's the Bottom Line?

Figuring out OceanFirst Bank home equity loan rates (or any lender's rates, for that matter) can feel like navigating a maze. But hopefully, this little chat has shed some light on the process. Remember, your credit score, LTV, loan amount, and loan term all play a role in determining your rate. And don't forget to shop around, negotiate, and read the fine print!

The key takeaway? Do your homework, understand your options, and don't be afraid to ask questions. And maybe… just maybe… you'll be sipping Mai Tais on that Tahitian beach sooner than you think. Just remember to send me a postcard!

Disclaimer: I'm just a friendly voice offering some informal guidance. I am not a financial advisor, and this information is not financial advice. Always consult with a qualified professional before making any financial decisions. Happy borrowing!