Writing Off Bad Debt In Quickbooks

Okay, so picture this: I'm at a local coffee shop, "supporting small businesses," naturally, and eavesdropping (as one does) on the conversation next to me. Two folks, clearly small business owners, are lamenting over unpaid invoices. One sighs dramatically, “I swear, Brenda owes me, like, six hundred bucks from last year! I’m never seeing that money.” The other nods sympathetically, then whispers something about "writing it off." My ears perked up! It's like hearing a secret code phrase for recovering from a financial gut punch.

And that, my friends, is what brings us here today. Let’s talk about writing off bad debt in QuickBooks. Because let's be honest, we've all been there. You did the work, you sent the invoice, and...crickets. That beautiful, shiny revenue you were counting on is now just...a mirage in the desert of accounts receivable. Ouch. But fear not! Writing off bad debt isn't just admitting defeat; it's a strategic move to clean up your books and get a tiny bit of tax relief. Maybe even feel a little less stabby when you think about Brenda. (Just kidding...mostly.)

What Exactly IS "Bad Debt," Anyway?

Good question! Bad debt, in simple terms, is money owed to you that you’ve determined is uncollectible. This isn't just a late payment; this is a debt you’ve essentially given up on ever receiving. We're talking about invoices that are way past due, collection attempts that have failed, and maybe even a bankruptcy filing on the customer's end. Basically, if it walks like a duck, quacks like a duck, and refuses to pay like a duck…it's probably bad debt.

Must Read

Think of it like this: you've tried everything. You've sent polite reminders, not-so-polite reminders, maybe even considered sending a carrier pigeon (though I wouldn't recommend it). You've exhausted your options. It's time to acknowledge the reality and move on. And more importantly, it's time to get that debt off your books.

Why Bother Writing Off Bad Debt in QuickBooks?

Okay, I get it. It feels like admitting failure. But trust me, there are some seriously good reasons to go through with it:

- Accurate Financial Reporting: Leaving uncollectible debts on your books inflates your assets and gives a false impression of your company's financial health. Writing them off gives you a more realistic picture of your financial position. You don't want to be making decisions based on numbers that aren't true, right?

- Potential Tax Deduction: In many cases, you can deduct bad debt from your taxable income, which can reduce your tax liability. Hallelujah! But remember to always consult with a tax professional to confirm eligibility and proper handling. (Seriously, don't skip this step.)

- Clean Up Your Accounts Receivable: All those old, unpaid invoices clutter up your reports and make it harder to track what's actually owed to you. Cleaning up your AR makes it easier to manage your finances and see where you need to focus your collection efforts. Think of it as a spring cleaning for your QuickBooks file!

- Emotional Closure (Okay, Maybe a Little): Let's be real. Holding onto bad debt can be stressful and frustrating. Writing it off can provide a sense of closure and allow you to move on. It's like saying, "Okay, Brenda, I'm letting you go...and good riddance!" (Again, mostly kidding.)

Before You Write It Off: Due Diligence is Key

Hold your horses! You can't just write off any old invoice you feel like. You need to be able to demonstrate that you've made a reasonable effort to collect the debt. This usually means:

- Sending Multiple Invoices and Payment Reminders: Keep a record of when you sent invoices and reminders. This shows you were proactive in seeking payment.

- Making Phone Calls and Documenting Conversations: Log every phone call you made, including the date, time, and who you spoke with. Note the outcome of the conversation.

- Sending a Demand Letter: A formal demand letter from you or a lawyer can show you were serious about collecting the debt.

- Working with a Collection Agency (Optional): Hiring a collection agency demonstrates that you went the extra mile. Keep records of your communications with them.

- Assessing the Customer's Financial Situation: If you know the customer is bankrupt or insolvent, that’s pretty good evidence that the debt is uncollectible.

Basically, you need to be able to show the IRS (or your equivalent tax authority) that you did your homework. The more documentation you have, the better.

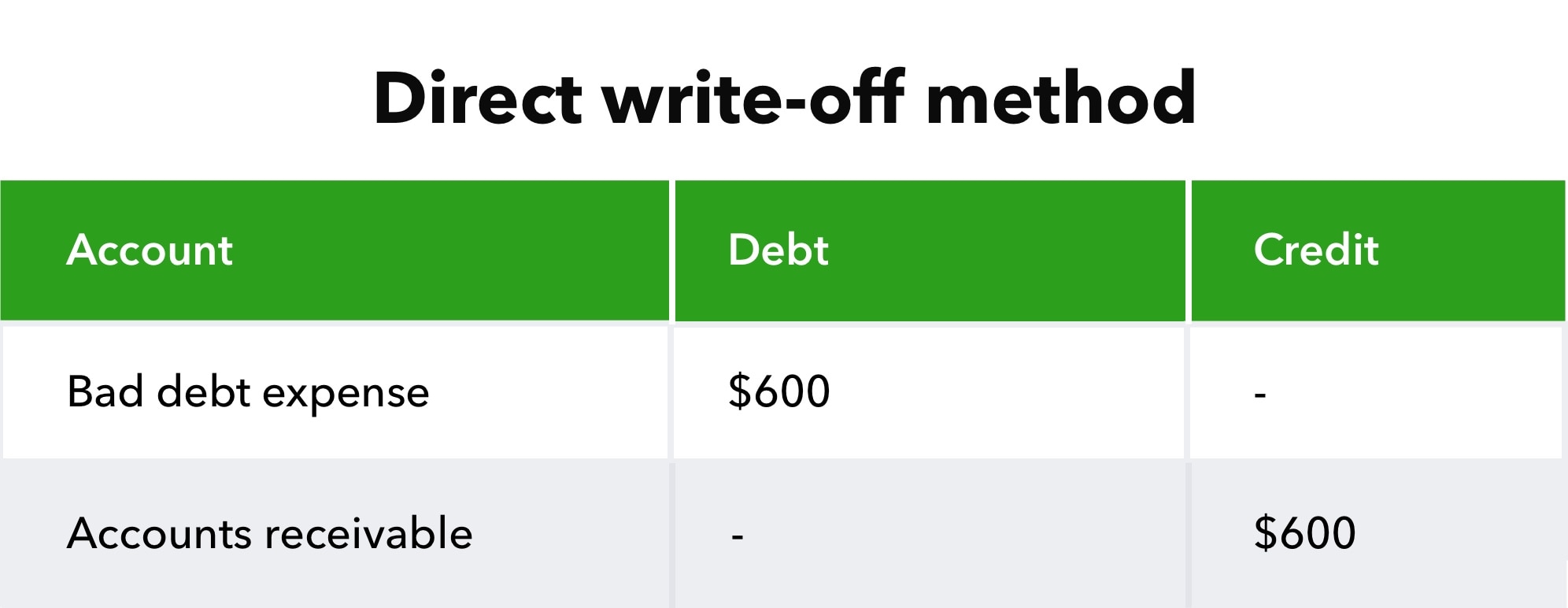

How to Actually Write Off Bad Debt in QuickBooks Online (QBO): The Direct Write-Off Method

Alright, let's get down to the nitty-gritty. There are a couple of ways to write off bad debt in QuickBooks, but the most common method is the direct write-off method. This method is simpler, and it's generally used by smaller businesses.

Here's how to do it in QBO:

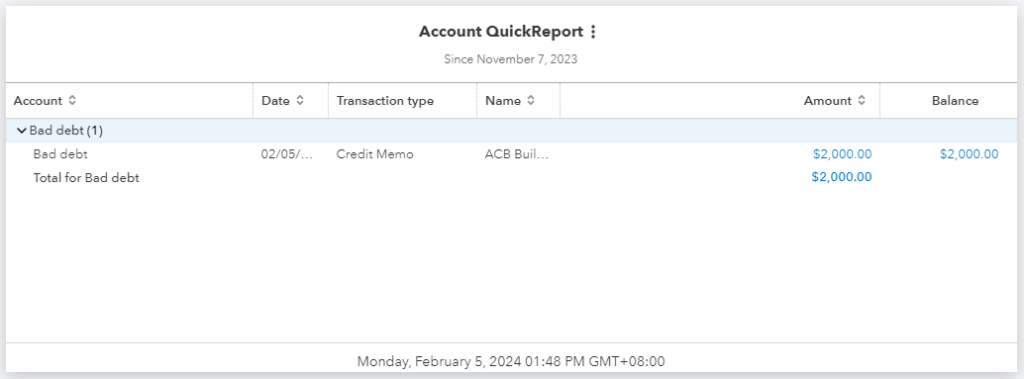

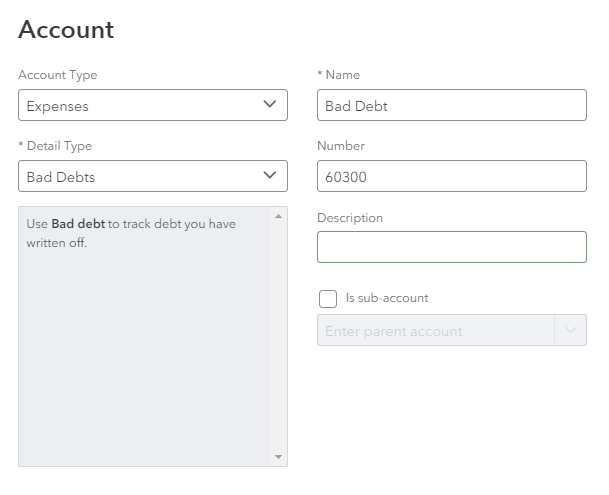

- Create a "Bad Debt Expense" Account: First, you need an account to record the expense. Go to Chart of Accounts (you can find it in the "Accounting" section on the left-hand navigation). Click "New." Choose "Expense" as the account type and "Bad Debts" as the detail type. Give it a name like "Bad Debt Expense" or "Uncollectible Accounts Expense." Save it! This is where the money will go that represents the lost income.

- Create a "Bad Debt Relief" item (Optional, but recommended): Go to "Sales", then "Products and Services", then "New", and then "Non-inventory". Name it "Bad Debt Relief" and make the income account "Bad Debt Expense". Why should you create this item? Because if you don't, you'll have to fill in the line details every time, which could lead to mistakes down the road.

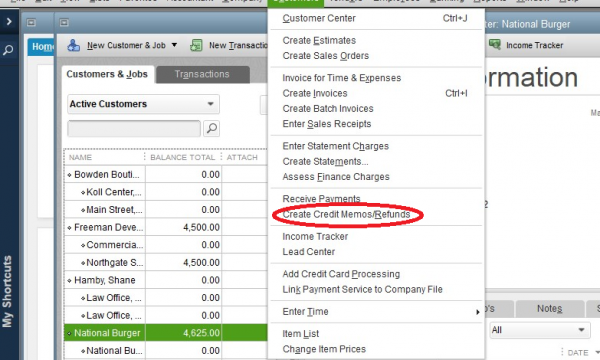

- Create a Credit Memo: This is the key step. Click the "+" icon at the top of the screen and select "Credit Memo." Choose the customer whose invoice you're writing off. Add the "Bad Debt Relief" item, and enter the amount of the debt you're writing off. In the "Account" area, choose the "Bad Debt Expense" account you created earlier. Add a note in the description field to explain why you're writing off the debt (e.g., "Invoice #1234 written off due to customer bankruptcy").

- Apply the Credit Memo to the Invoice: Now, you need to apply the credit memo to the unpaid invoice. Click "Save and close" on the credit memo. Then, go to the customer's account and find the unpaid invoice. Click "Receive Payment" for that invoice. You should see the credit memo listed as an available credit. Check the box next to the credit memo to apply it to the invoice. The amount due should now be zero. Click "Save and close."

Congratulations! You've just written off bad debt in QuickBooks Online! Now, take a deep breath and celebrate with a cup of coffee (or something stronger, I won't judge).

The Allowance Method (A More Sophisticated Approach)

The direct write-off method is simple, but it's not always the most accurate. The allowance method is a more sophisticated approach that involves estimating the amount of bad debt you expect to incur in the future and creating an allowance account to cover it.

This method is generally preferred by larger businesses that have a significant amount of accounts receivable. It's also required by Generally Accepted Accounting Principles (GAAP) in certain situations. The allowance method has two main advantages:

- Matching Principle: It aligns the expense of bad debt with the revenue it generated, providing a more accurate picture of your profitability.

- Accurate Balance Sheet: It presents a more realistic view of your accounts receivable by reducing them by the estimated amount of uncollectible debt.

I won't go into the details of the allowance method in this article (it's a bit more complex), but if you're interested in learning more, consult with an accountant or tax professional.

Important Considerations and Caveats

Before you start writing off bad debt left and right, here are a few important things to keep in mind:

- Consult with a Tax Professional: This is crucial! Tax laws regarding bad debt deductions can be complex and vary depending on your location and business structure. Always consult with a qualified tax professional to ensure you're following the rules and maximizing your tax benefits.

- Documentation is Key: I can't stress this enough. Keep meticulous records of all your collection efforts, customer communications, and any other relevant information. This documentation will be essential if you're ever audited.

- Don't Give Up Too Easily: Make sure you've truly exhausted all reasonable collection efforts before writing off a debt. Once you write it off, it's generally considered uncollectible, so you want to be sure you've done everything you can to recover the money.

- What if you actually get paid later? Okay, this is a rare but beautiful thing. If you wrote off a debt and the customer miraculously pays you later, you need to reverse the write-off. You'll basically do the opposite of what you did to write it off. (Consult with your accountant on the best way to handle this.)

In Conclusion: Take Control of Your Receivables!

Writing off bad debt isn't fun, but it's a necessary part of running a business. By understanding the process and following the steps outlined in this article, you can clean up your books, potentially reduce your tax liability, and move on from those frustrating unpaid invoices. Just remember to document everything, consult with a tax professional, and don't give up hope entirely... maybe Brenda will surprise you one day. (Okay, probably not, but it's nice to dream!)

So, go forth and conquer those accounts receivable! And remember, you're not alone. We've all been there, staring at those overdue invoices and wondering where all the money went. Just breathe, take action, and know that you've got this!

![Writing Off Bad Debt in Quickbooks Online Made Easy! [2024] - YouTube](https://i.ytimg.com/vi/TANIxJPa3n4/maxresdefault.jpg)