Which Of The Following Is Not An Asset

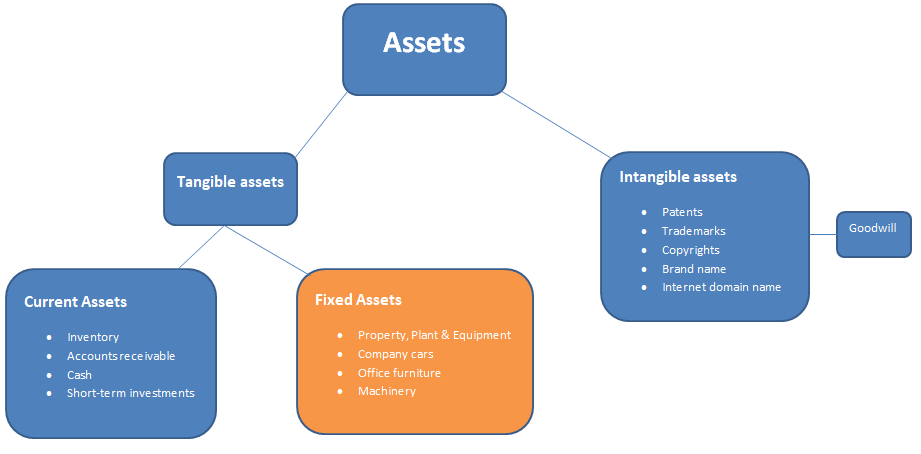

Identifying assets correctly is crucial for sound financial management, both for individuals and businesses. Assets represent resources of economic value that an entity owns or controls with the expectation that they will provide future benefit. Understanding what doesn't qualify as an asset is equally important.

Distinguishing Assets from Non-Assets

An asset possesses several key characteristics: it must be owned or controlled by the entity, it must have a probable future economic benefit, and that benefit must be reliably measurable. If an item fails to meet these criteria, it is generally not considered an asset.

Common Misconceptions About Assets

Several items are frequently mistaken for assets. These misunderstandings often stem from a superficial understanding of financial principles. Here's a breakdown of items that typically do not qualify as assets:

Must Read

“An asset is any item of value that a company owns.”

This statement, while partially correct, is incomplete and can be misleading. While an asset does indeed hold value, ownership alone is not sufficient. The item must also provide a future economic benefit that the entity can reliably measure.

Examples of Items That Are NOT Assets

Expenses

Definition: Expenses are costs incurred in the day-to-day operations of a business to generate revenue. They represent the consumption of assets or the incurrence of liabilities.

Why They Are Not Assets: While expenses are necessary for generating income, they lack future economic benefit beyond the period in which they are incurred. For instance, the salary paid to an employee is an expense because its benefit is consumed in that pay period. The employee's work contributes to revenue, but the salary itself is not an asset. Similarly, rent paid for office space is an expense; the benefit derived (use of the space) is consumed immediately.

Example: Advertising costs incurred to promote a product are an expense. Although the advertising may lead to increased sales, the cost itself is recorded as an expense in the period it is incurred. The benefit might extend into future periods, but generally accepted accounting principles (GAAP) require that such costs be expensed unless they meet strict criteria for capitalization (being recorded as an asset). Branding costs that directly and demonstrably increase future revenue may, in some instances, be capitalized, but the bar for doing so is high.

Liabilities

Definition: Liabilities represent obligations of an entity to transfer assets or provide services to other entities in the future as a result of past transactions or events.

Why They Are Not Assets: Liabilities are the opposite of assets. They represent what an entity owes to others, not what it owns. Common liabilities include accounts payable (money owed to suppliers), salaries payable (money owed to employees), and loans payable (money owed to lenders).

Example: A company takes out a loan from a bank. The loan amount is a liability, representing the company's obligation to repay the loan with interest. While the company may use the loan proceeds to acquire assets (like equipment), the loan itself is not an asset. The company owns the equipment (an asset), but owes the bank the loan amount (a liability).

Losses

Definition: Losses result from decreases in equity (net worth) from peripheral or incidental transactions of an entity. They often arise from unexpected events or activities not related to the company's core operations.

Why They Are Not Assets: Losses represent a decrease in an entity's wealth and do not provide any future economic benefit. Examples include losses from the sale of obsolete inventory, losses from lawsuits, or losses from natural disasters.

Example: A company suffers a fire that destroys a portion of its inventory. The value of the destroyed inventory represents a loss. This loss reduces the company's net worth but does not create any future benefit. Insurance proceeds received to cover the loss would be considered an asset.

Bad Debt Expense

Definition: Bad debt expense is the portion of accounts receivable that a company estimates will not be collected. It's an expense that reflects the risk of customers defaulting on their payments.

Why They Are Not Assets: Accounts receivable represent amounts owed to a company by its customers for goods or services provided on credit. They are assets. However, bad debt expense acknowledges that a portion of these receivables may be uncollectible. The bad debt expense itself is not an asset; it's a contra-asset account (specifically, an allowance for doubtful accounts) that reduces the net realizable value of accounts receivable. Essentially, it reflects the reduced value of the accounts receivable asset.

Example: A company has $100,000 in accounts receivable. Based on historical experience, the company estimates that $2,000 will be uncollectible. The company records a bad debt expense of $2,000 and creates an allowance for doubtful accounts of $2,000. The net realizable value of the accounts receivable (the amount the company expects to collect) is $98,000 ($100,000 - $2,000). The $2,000 bad debt expense is not an asset.

Depreciation Expense

Definition: Depreciation expense is the systematic allocation of the cost of a tangible asset (like equipment or a building) over its useful life. It reflects the gradual decline in the asset's value due to wear and tear, obsolescence, or other factors.

Why They Are Not Assets: The underlying asset (the equipment or building) is an asset. However, depreciation expense is the allocation of the cost of that asset to the periods in which it is used. It reduces the carrying value (book value) of the asset on the balance sheet. The depreciation expense itself is recorded on the income statement and represents the portion of the asset's cost that has been consumed during the accounting period. Like other expenses, it does not provide any future economic benefit beyond the period in which it is incurred.

Example: A company purchases a machine for $50,000 with an estimated useful life of 5 years. Using straight-line depreciation, the company will record depreciation expense of $10,000 per year ($50,000 / 5 years). The machine is an asset, but the $10,000 annual depreciation expense is not.

Intangible Considerations

The distinction between assets and non-assets can sometimes be blurred with intangible items. While some intangible items qualify as assets (e.g., patents, trademarks, copyrights, goodwill acquired in a business acquisition), others do not.

For instance, internally generated goodwill (e.g., a strong brand reputation developed through marketing efforts) is generally not recognized as an asset under GAAP. This is because its value is difficult to reliably measure and is not separable from the company itself. Similarly, a talented workforce is undoubtedly valuable, but the value of the human capital is not typically recorded as an asset on the balance sheet due to measurement challenges and the lack of control over employees (they can leave the company).

Key Takeaways

- Assets possess definable future economic benefits.

- Expenses, liabilities, and losses are fundamentally not assets.

- Depreciation expense and bad debt expense are related to assets but are not assets themselves; they reflect the consumption or reduced value of assets.

- Intangible items require careful evaluation to determine if they meet the criteria for asset recognition. Not all valuable intangible items are recorded as assets on the balance sheet.

A thorough understanding of these distinctions is essential for accurate financial reporting and effective decision-making.