Paying off your car loan is a significant financial milestone. Once you've made that final payment, several important processes are set in motion. Understanding these steps will ensure a smooth transition and allow you to fully realize the benefits of car ownership without debt.

Verification and Confirmation of Final Payment

Contacting Your Lender

Before celebrating, it’s prudent to contact your lender (bank, credit union, or finance company) a few weeks before your anticipated final payment date. Confirm the exact payoff amount, including any outstanding interest or fees. Request a written payoff quote, which is typically valid for a specific period (e.g., 10-15 days). This protects you from unexpected charges or discrepancies.

Methods of Payment

Ensure you understand the lender's accepted payment methods for the final amount. Wire transfers or certified checks are often preferred for larger, final payments due to their security and immediate availability of funds. Some lenders might allow online payments, but it's vital to confirm any limits and processing times associated with these methods.

After making the final payment, meticulously review your account statement online or in the mail to confirm that the loan is marked as “paid in full” or “closed.” If there are any discrepancies, contact your lender immediately to rectify the issue. Keep a copy of the final payment confirmation and the loan statement for your records.

Receiving Your Car Title

Lien Release Process

The most crucial aspect of paying off your car loan is receiving the car title. When you finance a vehicle, the lender places a lien on the title, signifying their ownership interest in the vehicle until the loan is repaid. Once the loan is satisfied, the lender is legally obligated to release the lien.

Title Delivery Methods

The method of title delivery varies depending on the state and the lender. Some states are "title-holding" states, where the lender physically holds the title during the loan term and mails it to you directly after the final payment. Other states are "non-title-holding" states, where the title is sent to the vehicle owner (you) with the lender's lien recorded on it. In these cases, the lender will send you a lien release document.

Title Delivery Timeframe

The time it takes to receive your title or lien release varies, but it typically ranges from 10 to 30 days after the final payment. Contact your lender if you haven't received it within this timeframe. Delays can occur due to processing times or administrative errors.

Is it good to pay off car loan early? Leia aqui: What happens when you

What to Do if You Don't Receive the Title

If you don't receive the title within a reasonable timeframe (e.g., 30 days), contact your lender immediately. Document all communication with the lender, including dates, names of representatives, and summaries of conversations. If the lender is unresponsive, you may need to contact your state's Department of Motor Vehicles (DMV) or equivalent agency for assistance. They can guide you through the process of obtaining a duplicate title or resolving the lien release issue. In some cases, legal advice might be necessary to compel the lender to release the lien.

Removing the Lien from Your Vehicle Record

Submitting the Lien Release

Once you receive the title (in title-holding states) or the lien release document (in non-title-holding states), you'll need to submit it to your state's DMV or equivalent agency to have the lien removed from your vehicle record. This officially confirms your full ownership of the vehicle.

DMV Requirements

The specific requirements for removing a lien vary by state. Typically, you'll need to bring the original title or lien release document, your driver's license, and a completed application form to the DMV. Some states may also require a small processing fee.

Obtaining a Clean Title

After the DMV processes your application, they will issue a new, clean title in your name, indicating that there are no outstanding liens on the vehicle. Keep this title in a safe place, as it is an important document for future transactions, such as selling or transferring the vehicle.

What happens if you pay off Self loan early? Leia aqui: What happens

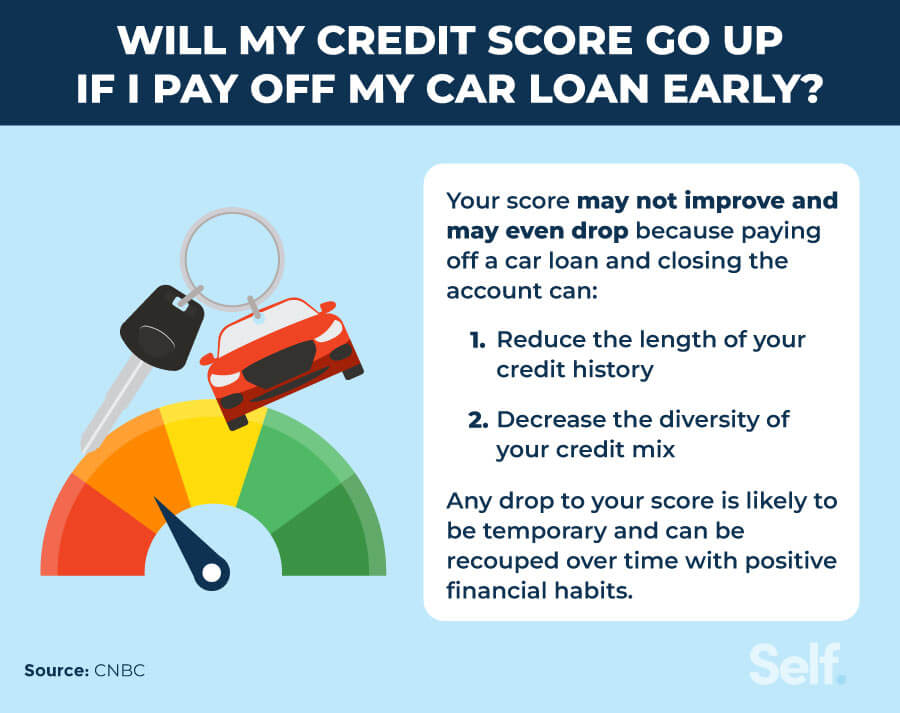

Impact on Credit Score

Loan Closure

Paying off your car loan is generally a positive event that will be reflected in your credit report. The closed account will be reported to the credit bureaus (Experian, Equifax, and TransUnion). This demonstrates responsible credit management.

Potential Credit Score Changes

The impact on your credit score is complex and depends on your overall credit profile. In some cases, your score might increase slightly due to the positive payment history and the reduction in your overall debt. However, if the car loan was your only installment loan, your score might temporarily decrease slightly due to the reduced credit mix. The effect is usually minimal and temporary.

Credit Report Monitoring

Regularly monitor your credit reports from all three major credit bureaus to ensure that the car loan is accurately reported as paid off and closed. You can obtain free copies of your credit reports annually from AnnualCreditReport.com. If you find any errors, dispute them with the credit bureau and the lender.

Insurance Considerations

Maintaining Insurance Coverage

Even after paying off your car loan, it's essential to maintain adequate car insurance coverage. While you're no longer required by the lender to carry specific coverage levels (such as collision or comprehensive), having insurance protects you financially in case of accidents, theft, or damage to your vehicle.

Reviewing Your Coverage Options

Consider reviewing your insurance coverage options with your insurance provider. Now that you own the car outright, you might choose to adjust your coverage levels based on your risk tolerance and financial situation. For example, if you have an older car with lower value, you might decide to reduce or eliminate collision and comprehensive coverage to save on premiums.

How to Pay Off a Car Loan Faster: 15 Steps (with Pictures)

Financial Planning After Loan Payoff

Reallocating Funds

Paying off your car loan frees up a significant amount of money each month. Consider how you want to reallocate these funds to achieve other financial goals. Some options include:

Saving for retirement: Increase your contributions to your 401(k), IRA, or other retirement accounts.

Building an emergency fund: Ensure you have sufficient funds to cover unexpected expenses.

Paying down other debt: Focus on paying off high-interest debt, such as credit card balances.

Should I pay off my car loan early? - CreditRepair.com

Investing: Invest in stocks, bonds, or other assets to grow your wealth.

Saving for a down payment on a home: If you plan to buy a home, allocate the funds towards your down payment.

Budgeting Adjustments

Adjust your budget to reflect the elimination of the car loan payment and the reallocation of funds towards your chosen financial goals. Regularly review your budget to ensure you're on track to achieve your objectives.

Key Takeaways

Paying off your car loan is a positive step toward financial freedom. Remember these key points:

Confirm the final payoff amount with your lender before making the last payment.

Verify that the loan is marked as "paid in full" after the final payment.

Obtain your car title or lien release document from the lender.

Submit the necessary documents to your DMV to remove the lien from your vehicle record.

Monitor your credit report to ensure accurate reporting of the loan closure.

Maintain adequate car insurance coverage.

Reallocate the freed-up funds to achieve other financial goals.

By following these steps, you can ensure a smooth transition to full car ownership and maximize the financial benefits of being debt-free.