What Is Ordinary Loss Debt Instrument

Okay, so picture this: Last year, I was feeling all high and mighty, ready to conquer the stock market. I convinced myself I was some kind of investing guru (spoiler alert: I'm not). I poured some cash into a startup that, on paper, looked like the next big thing. Fast forward six months, and… well, let's just say that startup is now serving as a cautionary tale in business school lectures. I took a bath. A big, soapy, financial bath. And while licking my wounds, I stumbled upon something called an "ordinary loss debt instrument." It sounded…intriguing. Like maybe, just maybe, there was a silver lining in this whole financial fiasco. That got me thinking - what exactly is an ordinary loss debt instrument, and could it have saved my bacon?

Understanding the Basics: Debt vs. Equity

Before we dive headfirst into the world of ordinary loss debt instruments, let's quickly recap the difference between debt and equity. This is Investing 101, people, but a little refresher never hurt anyone. Think of it this way:

- Equity: You're buying a piece of the company. You're a shareholder, an owner (albeit a tiny one, probably). You profit if the company does well, but you also suffer if it tanks. This is usually where the REALLY big gains (and losses) happen. Think stocks, shares, and the like.

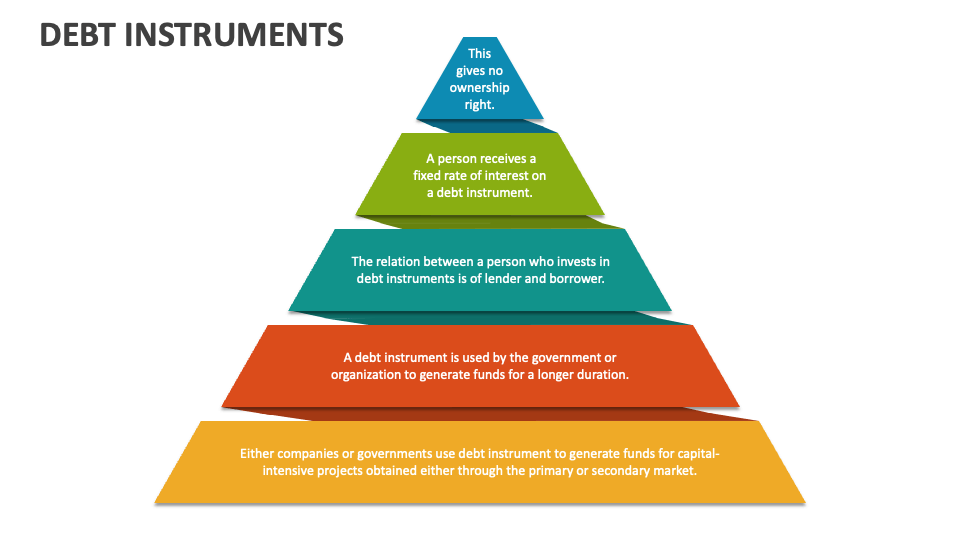

- Debt: You're lending money to the company. They promise to pay you back with interest. You're a creditor, not an owner. You're more concerned with getting your money back than hitting the jackpot. This is usually safer, but also has lower potential returns. Think bonds, loans, and… well, ordinary loss debt instruments!

See? Not so scary. Now, why does this distinction matter? Because the tax treatment of losses from debt and equity investments can be vastly different. And THAT'S where the "ordinary" part comes into play.

Must Read

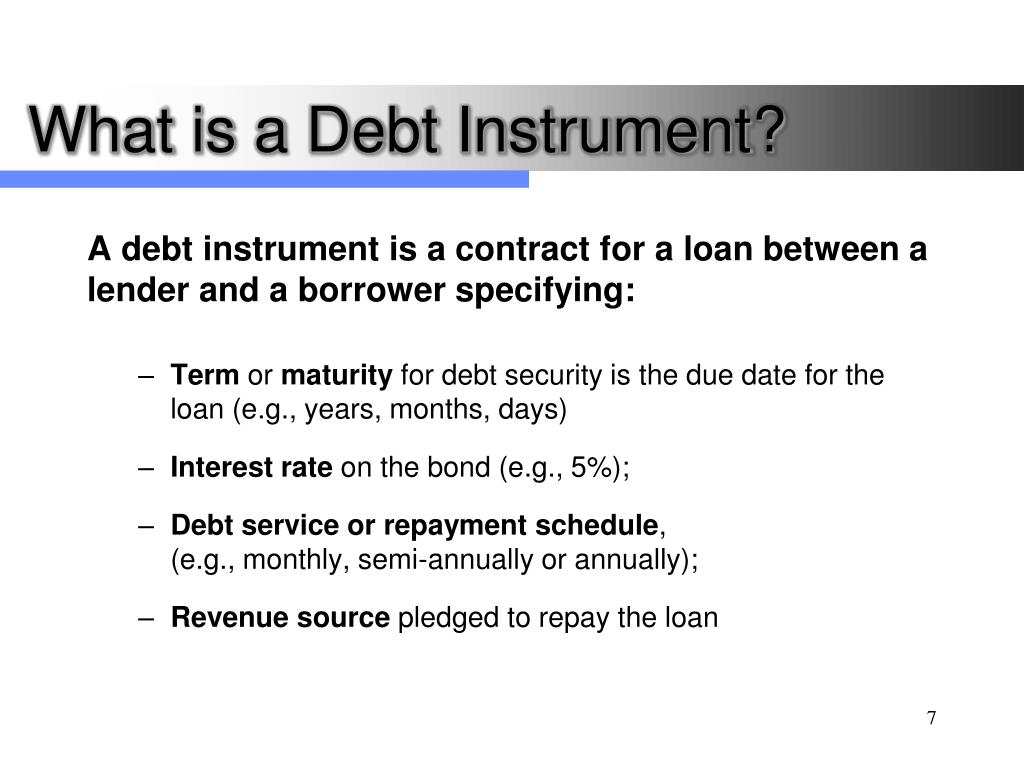

What IS an Ordinary Loss Debt Instrument?

Alright, drumroll please… An ordinary loss debt instrument is a type of debt security that, if it becomes worthless, allows you to deduct the loss against your ordinary income rather than being limited to the capital loss rules. This is HUGE. Let me explain further.

Normally, when you lose money on an investment – say, selling a stock for less than you bought it for – that's considered a capital loss. Capital losses are limited in how much you can deduct each year against your income. The IRS usually allows you to deduct up to $3,000 of capital losses per year against your ordinary income. Any losses beyond that? They get carried forward to future years. Which, let's be honest, feels like kicking someone when they're already down.

Ordinary loss debt instruments offer a potential workaround. If the debt instrument becomes completely worthless (think the company goes bankrupt and you get absolutely nothing), you can deduct the full loss against your ordinary income in the year the debt became worthless. Yes, you read that right. The full loss.

Imagine, just imagine, if my ill-fated startup investment had been structured as an ordinary loss debt instrument... Sigh. I could have written off the whole thing!

The Catch (There's Always a Catch, Isn't There?)

Of course, nothing's ever quite that simple, is it? There are some important caveats to keep in mind:

- It Must Be Bona Fide Debt: The instrument really needs to be debt. The IRS is smart. They're going to scrutinize anything that looks like disguised equity masquerading as debt. There needs to be a reasonable expectation of repayment, a fixed interest rate, and a maturity date. If it looks, smells, and quacks like equity, the IRS will treat it as equity.

- Worthlessness is Key: The debt has to be totally worthless. Not just "oh, it's not doing so well," but genuinely, certifiably, completely worthless. The company has to be belly up, with no assets left to pay creditors. Proving worthlessness can sometimes be tricky and might require some documentation.

- Small Business Stock (Section 1244 Stock): This is similar but relates to stock, not debt. Section 1244 stock allows individual investors and certain partnerships to deduct an ordinary loss (instead of a capital loss) on the sale or worthlessness of stock in a qualifying small business. This is another way to potentially mitigate investment losses, but it applies to equity, not debt. We're focusing on debt instruments here, though!

Examples of Ordinary Loss Debt Instruments

Okay, so what kind of debt instruments are we talking about here? Here are a few examples:

- Small Business Loans: If you make a loan to a small business, and that business goes bust, the loan may qualify as an ordinary loss debt instrument. This is especially relevant if you're lending money to a friend or family member who's starting a business. (Just remember the "bona fide" debt requirements!).

- Debt Issued by Financially Distressed Companies: Sometimes, companies on the brink of bankruptcy will issue debt to try and stay afloat. This debt is often considered high-risk, but it could potentially qualify as an ordinary loss debt instrument if the company ultimately fails. This, of course, is high-risk, high-reward…or high-risk, high-loss, more likely.

Important Note: Not all small business loans or debt issued by financially distressed companies automatically qualify. It's crucial to do your research and consult with a tax advisor to determine if a particular debt instrument meets the requirements for ordinary loss treatment.

Why Ordinary Loss Treatment Matters

Let's be blunt: losing money sucks. But if you have to lose money (and let's face it, everyone does at some point), wouldn't you rather minimize the tax hit? That's where ordinary loss treatment comes in.

The advantage of deducting a loss against ordinary income is that it can significantly reduce your tax liability in the year the loss occurs. This is particularly beneficial if you have a high income in that year. Think of it as a tax shield against some of your earnings.

Let's illustrate with an example: Imagine you have a $50,000 ordinary loss from a debt instrument that went belly up. You also have $100,000 of ordinary income (salary, wages, etc.). If you can deduct the $50,000 loss against your $100,000 income, your taxable income is reduced to $50,000. That's a huge tax savings! Compared to if the $50,000 was a capital loss, you could only deduct $3,000 a year, leaving $47,000 to be carried forward, and slowly deducted over several years.

How to Determine if a Debt Instrument Qualifies

So, you're intrigued. You're thinking, "Maybe I should look into these ordinary loss debt instrument things." Smart move! But how do you determine if a particular debt instrument qualifies for ordinary loss treatment?

- Review the Terms of the Debt Instrument: Carefully examine the loan agreement or bond indenture. Look for clauses that address what happens in the event of default or bankruptcy. Does the instrument clearly define the borrower's obligation to repay the debt?

- Assess the Financial Health of the Borrower: Do your due diligence on the borrower's financial situation. Are they financially stable? Do they have a good track record of repaying debt? The riskier the borrower, the higher the chance the debt will become worthless. And the riskier the investment, the more you need to be sure the loss can be claimed as an ordinary loss.

- Consult with a Tax Advisor: This is the most important step! Tax laws are complex and can change frequently. A qualified tax advisor can review the specific facts and circumstances of your situation and provide personalized advice. Don't rely solely on information you find online (even from this amazing article!).

Potential Risks and Considerations

Investing in debt instruments that might qualify for ordinary loss treatment is not without risk. Here are a few things to consider:

- Higher Risk of Default: Debt instruments that offer the potential for ordinary loss treatment are often issued by companies that are already financially distressed. This means there's a higher risk that the company will default on the debt, and you'll lose your entire investment.

- Difficulty Proving Worthlessness: As mentioned earlier, proving that a debt instrument is completely worthless can be challenging. The IRS may require documentation such as bankruptcy filings, liquidation reports, or appraisals to support your claim.

- Complexity of Tax Laws: The rules surrounding ordinary loss treatment can be complex and subject to interpretation. Make sure you understand the rules and consult with a tax advisor to ensure you're complying with the law.

Is It Right for You?

So, after all of this, the big question: Are ordinary loss debt instruments right for you? The answer, as always, is "it depends." These investments can be a useful tool for mitigating losses and reducing your tax liability, but they're not suitable for everyone. They might be a good fit if:

- You're comfortable with a higher level of risk.

- You have a high income and could benefit from the tax deduction.

- You have a good understanding of the tax laws.

- You're working with a qualified tax advisor.

Ultimately, the decision of whether or not to invest in ordinary loss debt instruments is a personal one. Weigh the potential benefits against the risks, do your due diligence, and consult with a tax advisor to make an informed decision.

As for me? I'm definitely going to be more careful with my investments in the future. And I'm going to seriously consider whether structuring some of them as ordinary loss debt instruments makes sense. Maybe, just maybe, I can turn my investing misfortunes into a slightly less painful tax situation. Fingers crossed!

:max_bytes(150000):strip_icc()/DebtInstrument-bac00eababe34debb46875d94bf71ff4.jpg)