What Is A Mortgage Acquisition Date

The mortgage acquisition date, while seemingly simple, is a crucial piece of information linked to your home loan. It’s the day you officially took ownership of the mortgage, marking the starting point for many important calculations and processes. Understanding what it is and where to find it can be surprisingly useful in various everyday scenarios.

Understanding the Mortgage Acquisition Date

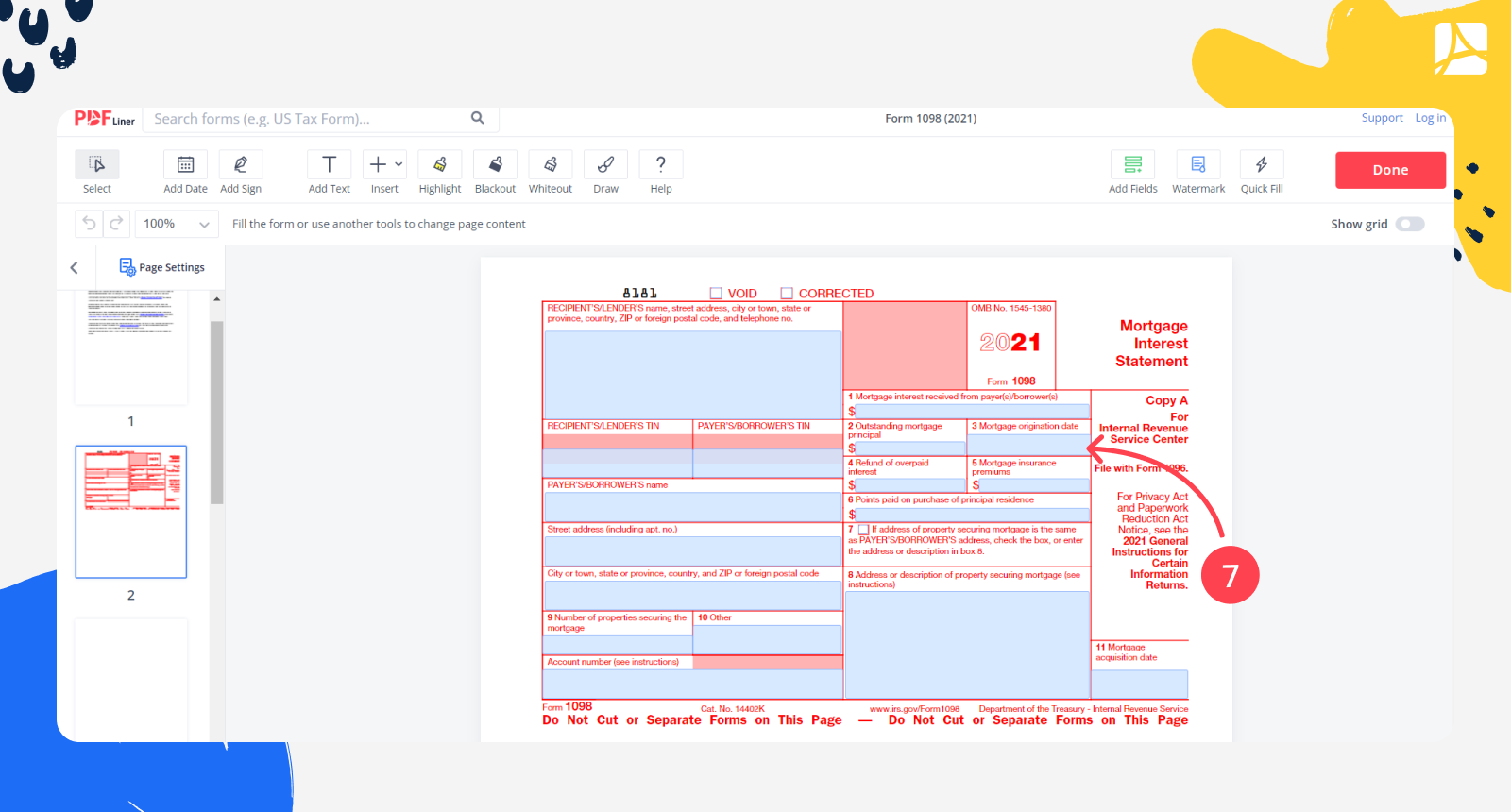

Essentially, the mortgage acquisition date is the date your mortgage loan was finalized and the funds were disbursed. It's not necessarily the same as the closing date on your home purchase, although they are usually very close. The acquisition date represents the formal inception of your mortgage obligation.

Where to Find It:

Must Read

You can typically find your mortgage acquisition date in several places:

- Your mortgage statement: Look for it near the loan origination date or similar label.

- Your closing documents: Specifically, the loan agreement or promissory note.

- Your online mortgage account: Most lenders provide online portals where you can access your loan details.

Practical Applications in Daily Life

Knowing your mortgage acquisition date isn’t just about having a piece of information; it's about understanding how it affects various financial aspects related to your home.

1. Calculating Interest Paid:

This date is pivotal when calculating how much interest you've paid on your mortgage over a specific period. This information is essential for several reasons:

- Tax Deductions: In many jurisdictions, mortgage interest is tax-deductible. You’ll need to know the total interest paid each year to claim this deduction. Having the correct acquisition date ensures accurate calculations. You can use online mortgage calculators, inputting the acquisition date and other loan details, to determine the interest portion of your payments.

- Financial Planning: Knowing how much you're paying in interest versus principal helps you understand the true cost of your home loan and allows for better financial planning. This insight can influence decisions like refinancing or making extra principal payments.

Example: Let's say you acquired your mortgage on July 15, 2020. To calculate your interest paid for the 2023 tax year, you'd need to sum the interest portions of all payments made from January 2023 to December 2023. The acquisition date anchors this calculation.

2. Refinancing Analysis:

When considering refinancing, the acquisition date plays a role in assessing the potential benefits. Specifically, it helps you understand:

- Break-Even Point: Refinancing involves costs (e.g., appraisal fees, origination fees). Knowing your acquisition date, original interest rate, and remaining principal allows you to calculate how long it will take to recoup these costs with the lower interest rate offered by the new loan. This "break-even point" is critical for deciding if refinancing is worthwhile.

- Loan Age: The acquisition date helps determine how much of your loan you've already paid off. This can influence the types of refinance options available to you (e.g., cash-out refinance).

3. Home Equity Calculation:

Your home equity is the difference between your home's current market value and your outstanding mortgage balance. The acquisition date is indirectly important here because it helps track how your mortgage balance has changed over time. Combined with property value appraisals, you can more accurately track your equity growth.

4. Mortgage Insurance (PMI) Removal:

If you paid less than 20% down when you bought your home, you likely have private mortgage insurance (PMI). PMI can often be removed once you reach 20% equity. The acquisition date helps track the amortization of your loan (the gradual reduction of the principal balance) and, combined with increases in your home's value, determine when you reach that 20% equity threshold. You can proactively contact your lender to initiate the PMI removal process once you believe you meet the criteria.

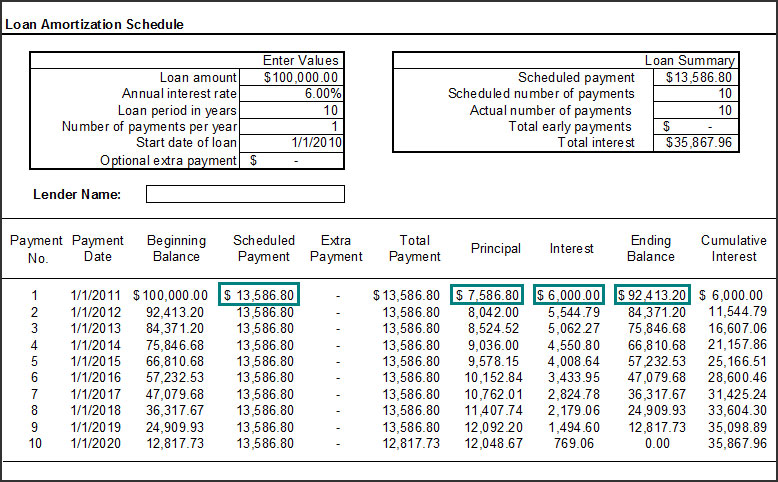

5. Understanding Loan Amortization:

The acquisition date is the starting point for your loan's amortization schedule. This schedule details how each payment is allocated between principal and interest over the life of the loan. Reviewing your amortization schedule (often available online or upon request from your lender) helps you understand how your loan balance decreases over time. It can also guide decisions about making extra principal payments to accelerate the payoff process.

6. Potential Legal Issues:

In rare cases, the accuracy of the acquisition date might become relevant in legal disputes related to the mortgage. For example, discrepancies in loan documentation or issues with foreclosure proceedings can sometimes hinge on the validity of this date. While less common, it's still a good reason to keep accurate records of your mortgage documents.

Practical Tips

- Keep your closing documents organized: These documents contain vital information, including the acquisition date. Store them securely in a safe place.

- Monitor your mortgage statements: Review your statements regularly to ensure the information is accurate. Contact your lender immediately if you notice any discrepancies.

- Utilize online resources: Many websites and financial tools can help you calculate interest paid, estimate your break-even point for refinancing, and track your home equity.

A Quick Checklist/Guideline

- Locate your mortgage acquisition date: Find it on your mortgage statement, closing documents, or online account.

- Record the date in a safe place: Keep it with your other important financial documents.

- Use the date for calculations: Employ it when calculating interest paid, analyzing refinancing options, or tracking home equity.

- Verify accuracy: Double-check the acquisition date against multiple sources to ensure accuracy.

- Consult professionals: If you have any questions or need assistance with calculations, consult a financial advisor or mortgage professional.

By understanding the significance of your mortgage acquisition date and how to use it, you can make more informed financial decisions related to your home loan and overall financial well-being.