What Happens After Pay Off Car Loan

The final payment on a car loan is a significant milestone for many individuals. It signifies the end of a recurring financial obligation and opens up new possibilities for budgeting and financial planning. However, the experience doesn't conclude the moment the last check clears. A series of steps and potential consequences follow, each with its own set of implications. Understanding these post-payment realities is crucial for navigating the transition smoothly and maximizing the benefits of becoming debt-free.

Causes: The Path to Loan Completion

The journey to paying off a car loan is driven by several key factors. Primarily, it's the result of consistent adherence to the loan repayment schedule, a commitment that reflects financial discipline and responsible borrowing. The amortization schedule, a detailed breakdown of each payment showing the allocation towards principal and interest, plays a crucial role. As payments are made over time, a greater portion is directed towards the principal, gradually reducing the outstanding balance.

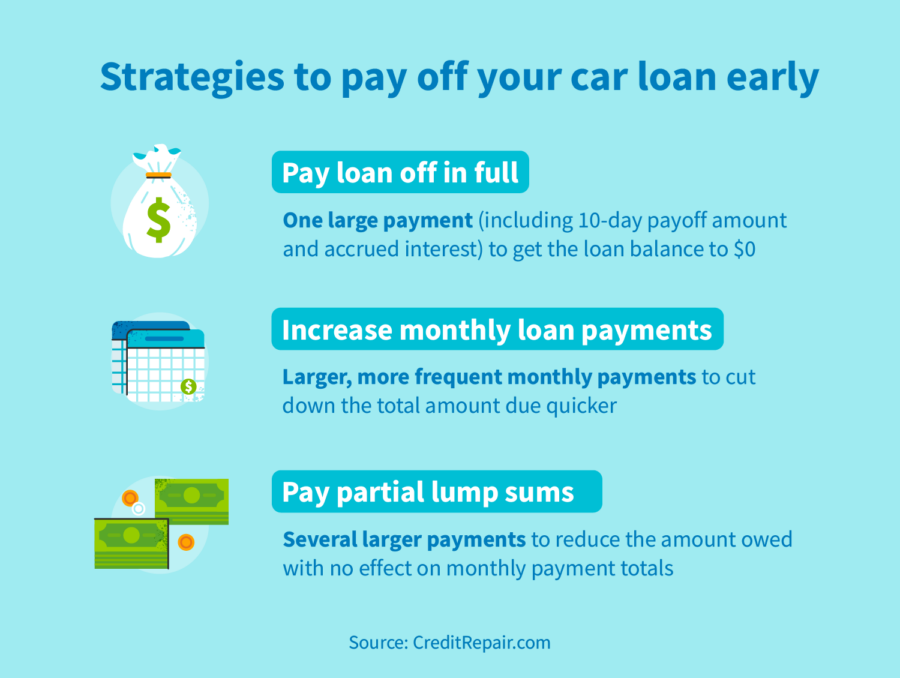

Another contributing factor is the borrower's financial circumstances. An increase in income, coupled with consistent budgeting, can accelerate the repayment process. Some borrowers may choose to make extra payments, either regularly or sporadically, further shortening the loan term and reducing the total interest paid. This proactive approach requires careful financial planning and the ability to allocate additional funds towards debt reduction.

Must Read

Refinancing can also indirectly lead to loan completion. While it doesn't directly pay off the original loan, refinancing into a loan with a shorter term or a lower interest rate can expedite the overall repayment process. This strategy, however, is dependent on market conditions and the borrower's creditworthiness. The Federal Reserve's interest rate policies significantly impact auto loan rates, influencing the feasibility and attractiveness of refinancing options. For example, during periods of low interest rates, refinancing activity tends to increase as borrowers seek to lower their monthly payments or shorten the loan term.

Conversely, certain circumstances can hinder or delay loan completion. Unexpected expenses, job loss, or financial emergencies can strain a borrower's ability to make timely payments. This can lead to missed payments, late fees, and potentially even repossession. According to a 2023 report by the Consumer Financial Protection Bureau (CFPB), a significant percentage of auto loan borrowers experience difficulty in making payments, highlighting the vulnerability of some individuals to economic shocks.

Effects: Immediate and Long-Term Consequences

The immediate effects of paying off a car loan are primarily financial. The most obvious consequence is the elimination of the monthly loan payment, freeing up a significant portion of the borrower's budget. This newfound financial flexibility can be used for various purposes, such as investing, saving for retirement, paying down other debts, or simply improving one's quality of life.

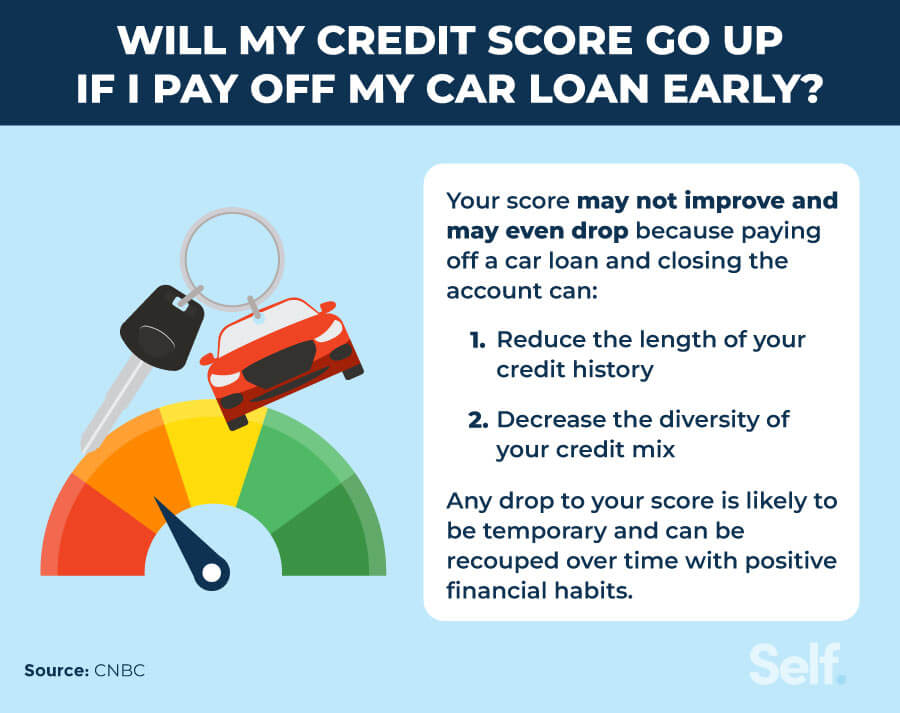

Furthermore, paying off a car loan positively impacts one's credit score. As the loan is reported as paid in full to the credit bureaus, it demonstrates responsible credit management and contributes to a stronger credit history. This can lead to more favorable terms on future loans or credit applications. The specific impact on one's credit score will depend on individual credit history and other factors.

"Paying off a loan is always a good thing for your credit report," says credit expert John Ulzheimer. "It shows lenders that you are capable of repaying your debts."

Another effect is the release of the lien on the vehicle. The lender's security interest in the car is lifted, and the borrower receives the title, officially signifying ownership. This process may involve some paperwork and administrative steps, depending on the state and the lender. In some cases, the lender will automatically send the title to the borrower, while in others, the borrower may need to request it.

The long-term effects extend beyond the immediate financial benefits. Owning a car outright provides a sense of security and independence. It removes the risk of repossession and allows the borrower to make decisions about the vehicle without needing the lender's approval. This freedom can be particularly valuable during times of financial uncertainty.

However, it's also important to consider the potential for increased maintenance costs as the vehicle ages. As cars get older, they tend to require more repairs and maintenance. The money saved from the loan payment may need to be allocated towards these expenses. Therefore, it's crucial to factor in these potential costs when planning one's budget after paying off the car loan.

Implications: Broader Financial and Societal Impacts

The implications of paying off a car loan extend beyond the individual borrower and have broader financial and societal impacts. On a macroeconomic level, decreased consumer debt can contribute to greater economic stability. When individuals have less debt, they are less vulnerable to economic downturns and are more likely to spend and invest, stimulating economic growth.

For the financial industry, the completion of auto loan payments represents a shift in the lender-borrower relationship. The lender receives its principal and interest, closing the transaction. This allows lenders to allocate capital to new loans and investments, contributing to the overall flow of credit in the economy. The profitability of auto lending is heavily influenced by interest rate spreads and loan default rates, which in turn are affected by economic conditions and consumer behavior.

From a societal perspective, car ownership plays a significant role in mobility and access to opportunities. For many individuals, owning a car is essential for commuting to work, accessing healthcare, and participating in social activities. Paying off a car loan provides a sense of financial empowerment and increases access to these opportunities, particularly for those in areas with limited public transportation. Reliable transportation can be a critical factor in upward mobility, allowing individuals to access better jobs and educational opportunities.

However, the reliance on personal vehicles also has negative implications, such as increased traffic congestion, air pollution, and dependence on fossil fuels. Encouraging the use of public transportation, cycling, and walking can help to mitigate these negative impacts. Furthermore, the increasing prevalence of ride-sharing services and electric vehicles is transforming the transportation landscape and potentially reducing the need for individual car ownership in the long run.

Finally, the psychological impact of paying off a car loan should not be underestimated. It can provide a sense of accomplishment and reduce stress, leading to improved mental and emotional well-being. This positive reinforcement can motivate individuals to pursue other financial goals and adopt more responsible financial habits. Achieving financial milestones, such as paying off a car loan, can contribute to a greater sense of control over one's life and future.

The history of auto loans in the United States reflects the evolution of consumer credit and the automobile industry. In the early 20th century, car ownership was primarily limited to the wealthy. The introduction of installment loans made cars more accessible to the middle class, fueling the growth of the auto industry and transforming American society. Today, auto loans are a ubiquitous part of the financial landscape, with trillions of dollars in outstanding debt. The terms and conditions of these loans have evolved over time, reflecting changes in interest rates, credit risk, and regulatory oversight.

Navigating the Aftermath: Practical Steps

Upon paying off a car loan, several practical steps should be taken. First, confirm with the lender that the loan is indeed paid in full and request a written confirmation. Second, obtain the title to the vehicle and ensure that it is properly registered in your name. Third, review your budget and reallocate the funds previously used for the car payment towards other financial goals. Finally, consider increasing your insurance coverage to protect your investment in the vehicle.

These actions, though seemingly simple, ensure a clean break from the loan obligation and position you for sound financial management in the future. Ignoring these steps can lead to unnecessary complications and potential financial setbacks.

Conclusion

Paying off a car loan is a multifaceted event with far-reaching consequences. While the immediate benefits are clear – the elimination of monthly payments and the improvement of one's credit score – the long-term implications extend to broader financial stability, societal impacts, and even psychological well-being. Understanding these nuances is crucial for maximizing the positive effects and mitigating any potential drawbacks. By carefully planning and managing one's finances, individuals can leverage the newfound financial freedom to achieve their goals and build a more secure future. The experience serves as a valuable lesson in financial responsibility and the power of sustained effort in achieving long-term goals. The broader significance lies in its contribution to individual empowerment and overall economic health, highlighting the interconnectedness of personal finance and societal well-being.

![How to Pay Off a Car Loan Faster [5 Tested Methods for 2024]](https://review42.com/wp-content/uploads/2022/02/feature-image-49-how-to-pay-off-car-loan-faster.jpg)