What Are The Five 5 Types Of Collateral

Hey there, friend! Ever wondered how you can get a loan, even when you don't have a sparkling credit score or a ton of cash upfront? The secret often lies in something called collateral. Think of it like this: it's your "pinky promise" to the lender that you'll pay them back. But instead of just words, it's something of value that they can grab onto if things go south.

Now, I know what you're thinking: "Collateral? Sounds complicated!" But trust me, it's not rocket science. In fact, you've probably encountered collateral in your everyday life without even realizing it. So, let's break down the five main types of collateral and why you should even care. Ready? Let's dive in!

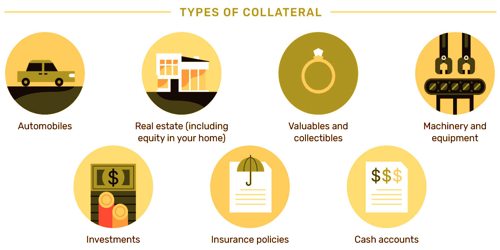

1. Real Estate: Your Humble (or Not-So-Humble) Abode

Okay, this is probably the most well-known type of collateral. Real estate includes your house, your apartment, your vacation cabin in the woods – any land and permanent structures on it. When you get a mortgage, your house is the collateral. If you stop making those mortgage payments, the bank has the right to foreclose and sell your house to recoup their money.

Must Read

Think of it like this: imagine you’re borrowing a friend’s super-rare vinyl record collection (valued at a small fortune, naturally!). You promise to return it in pristine condition, but to give them extra assurance, you leave your vintage guitar with them as collateral. If you scratch their records beyond repair, they get to keep your guitar. Pretty straightforward, right? Mortgages work on the same principle – only with a house and a whole lot more paperwork!

Why should you care? Well, understanding real estate as collateral can help you make informed decisions about homeownership and refinancing. It’s a huge responsibility, but also a powerful tool for building wealth. Knowing the risks associated with defaulting on your mortgage can save you a lot of heartache (and your house!).

2. Personal Property: Your Treasures and Trinkets (of Value)

This category covers a broad range of items, from your car and boat to your jewelry, electronics, and even your prized stamp collection (if it's worth something!). Personal property as collateral is all about tangible assets that hold monetary value.

Let's say you want to buy a shiny new motorcycle but don't have the cash. You can get an auto loan, where the motorcycle itself acts as collateral. Miss too many payments, and the lender can repossess the bike. It’s like promising your friend your awesome gaming console if you don't pay them back the $20 they lent you. Maybe a bit extreme for $20, but you get the idea!

Another example could be pawning jewelry. You need some quick cash, so you take your gold necklace to a pawn shop. They'll give you a loan, using the necklace as collateral. If you don't repay the loan within the agreed timeframe, they get to keep and sell the necklace.

Why should you care? Knowing what qualifies as personal property collateral can help you access loans you might not otherwise qualify for. Just be sure you're comfortable with the risk of losing those cherished possessions if you can't repay the loan. It's a trade-off between accessing funds and potentially parting ways with your valuables. Always weigh the options carefully!

3. Savings and Investments: Your Nest Egg on the Line

Believe it or not, your savings and investments can also be used as collateral! This includes savings accounts, certificates of deposit (CDs), stocks, and bonds. The lender essentially places a hold on these assets, preventing you from withdrawing or selling them until the loan is repaid.

Imagine you have a significant amount of money in a CD. You want to start a small business, but you don't want to withdraw the money from the CD and lose the interest it's earning. You could potentially use the CD as collateral for a loan to fund your business venture. If your business fails and you can't repay the loan, the lender can seize the funds in your CD.

Why should you care? Using savings and investments as collateral can be a strategic move if you want to access loans without liquidating your assets. However, it’s crucial to understand the risks involved. If you're not confident in your ability to repay the loan, you could lose your hard-earned savings. It’s about balancing the potential rewards with the potential for significant loss.

4. Inventory: The Lifeblood of Businesses

This one is mostly relevant to business owners. Inventory refers to the goods a business has on hand for sale. It can include raw materials, work-in-progress, and finished products. Lenders often accept inventory as collateral for business loans, particularly for businesses involved in manufacturing, retail, or wholesale.

Think of a small bakery that needs a loan to buy more ovens and ingredients. They can use their existing stock of flour, sugar, and baked goods as collateral. If the bakery defaults on the loan, the lender can seize the inventory and sell it to recoup their money.

Why should you care? If you’re a business owner, understanding inventory as collateral can unlock financing options to help you grow your business. It allows you to leverage your existing assets to secure the funds you need for expansion, purchasing equipment, or managing cash flow. However, you need to carefully manage your inventory and ensure it retains its value to avoid complications if the lender needs to seize it.

5. Accounts Receivable: Money Owed to You

Another one primarily for businesses, accounts receivable represent the money that customers owe to your business for goods or services already delivered. Lenders may accept these outstanding invoices as collateral for a loan.

Let’s say you run a freelance web design business. You’ve completed several projects, but your clients haven’t paid you yet. You can use these unpaid invoices as collateral to secure a short-term loan to cover your expenses until the payments come in. The lender essentially gets the right to collect those payments if you default on the loan.

Why should you care? Accounts receivable financing can be a lifesaver for businesses that experience cash flow challenges due to delayed customer payments. It allows you to access immediate funds based on the value of your outstanding invoices, helping you bridge the gap between providing services and getting paid. Just be aware that the lender will typically scrutinize the creditworthiness of your customers to assess the risk associated with collecting those payments.

Final Thoughts: Collateral is Your Friend (When Used Wisely!)

So, there you have it! The five main types of collateral, demystified and explained in a way that (hopefully!) makes sense. Remember, collateral is all about reducing risk for the lender and increasing your chances of getting approved for a loan. But it's a two-way street. It's crucial to fully understand the implications of pledging your assets as collateral and to only borrow what you can confidently repay.

Think of collateral like a safety net. It's there to protect the lender (and ultimately, the financial system!), but you also need to be aware of where it is and how it works before you jump! With a little knowledge and careful planning, you can use collateral to your advantage and achieve your financial goals without putting your valuable assets at undue risk. Happy borrowing (responsibly, of course)!

:max_bytes(150000):strip_icc()/collateral-loans-315195-v3-5bc4cbf746e0fb002693d842.png)