What Are Current And Noncurrent Assets

Understanding Asset Classification: Current and Noncurrent Assets

Assets are a fundamental component of any business's financial health, representing the resources a company owns or controls that are expected to provide future economic benefits. These assets are broadly categorized into two main types: current assets and noncurrent assets. Understanding the distinction between these categories is crucial for accurate financial reporting, analysis, and decision-making.

Current Assets: Short-Term Resources

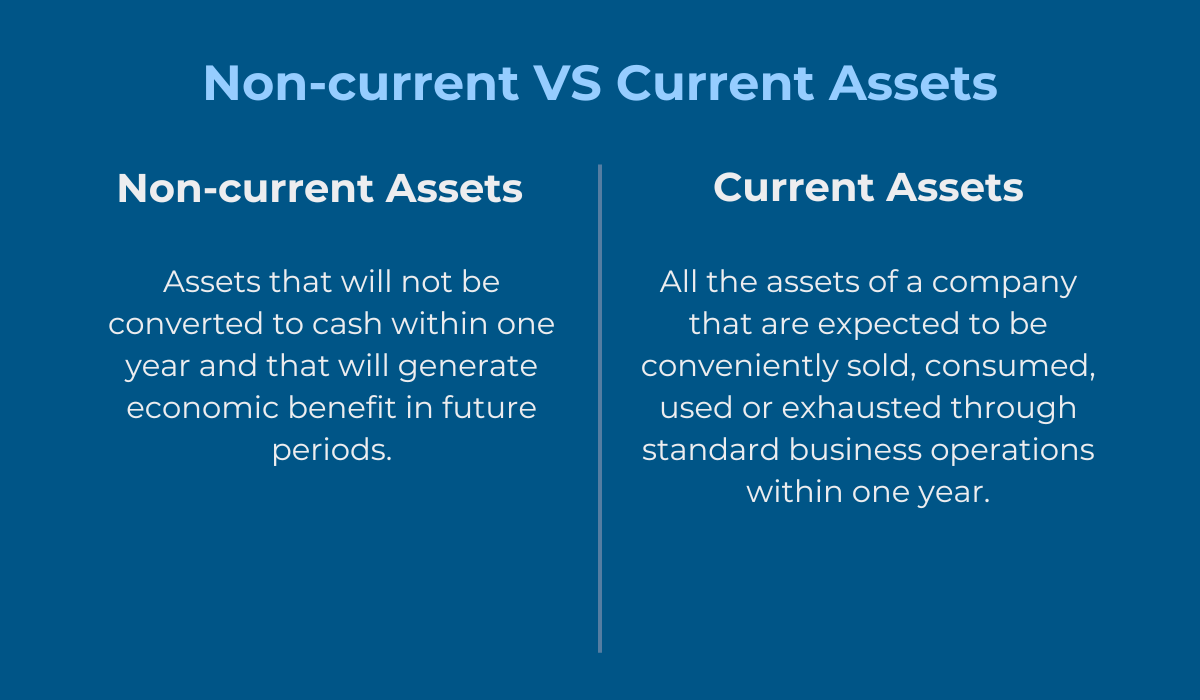

Current assets are defined as assets that are expected to be converted into cash, sold, or consumed within one year or the company's operating cycle, whichever is longer. This short-term nature makes them readily available to meet a company's immediate obligations and operational needs.

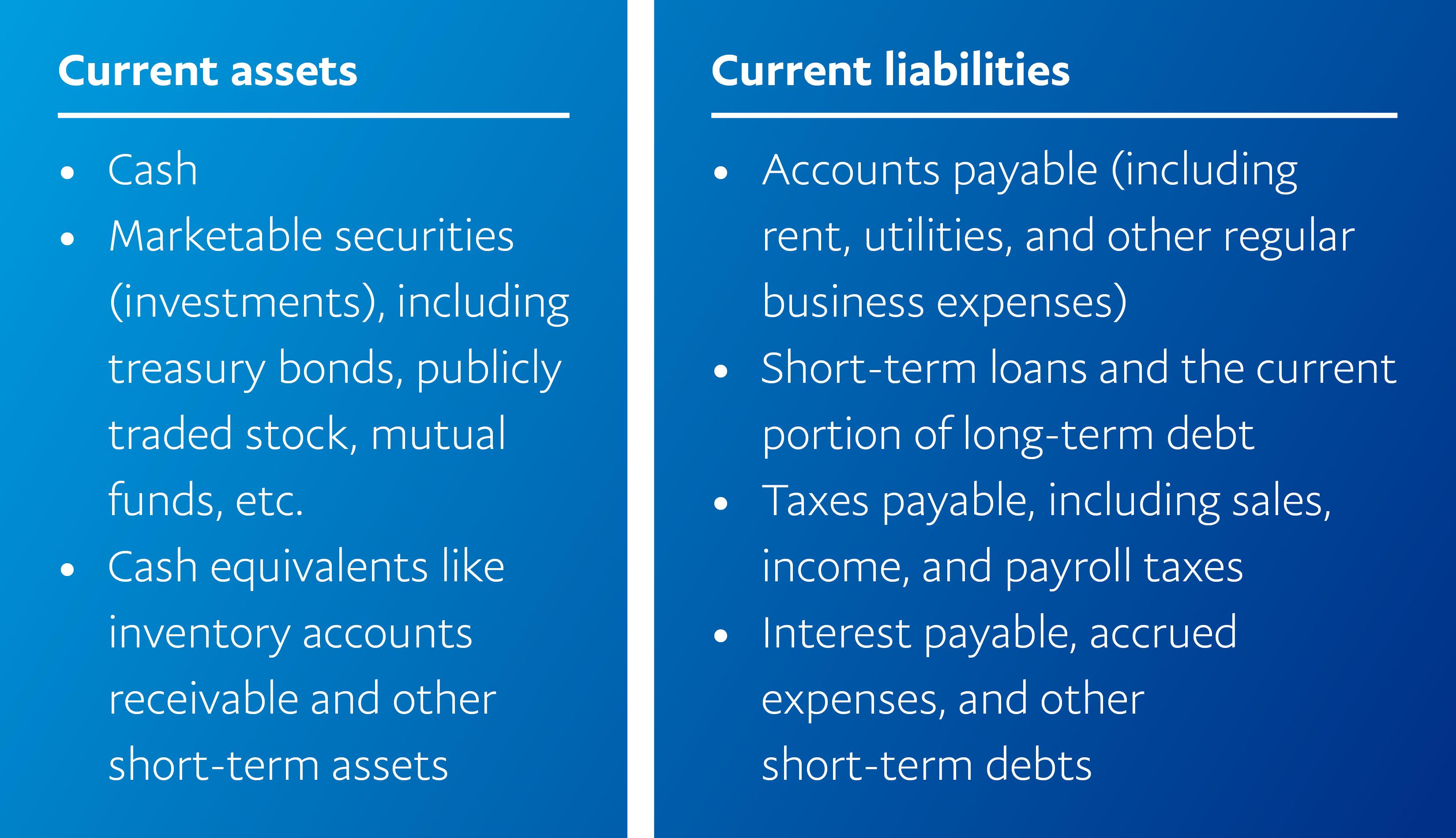

Common examples of current assets include:

Must Read

- Cash and Cash Equivalents: This is the most liquid asset, including readily available cash on hand, checking accounts, and short-term, highly liquid investments like treasury bills and commercial paper. These investments typically have maturities of three months or less.

- Marketable Securities: These are short-term investments that can be easily converted into cash, such as stocks and bonds held for short-term trading purposes. The intention is to generate profits from short-term price fluctuations.

- Accounts Receivable: This represents money owed to the company by its customers for goods or services delivered on credit. The collection period is typically within 30 to 90 days. A crucial aspect of accounts receivable management is the allowance for doubtful accounts, which is an estimate of the amount of accounts receivable that may not be collected.

- Inventory: This includes raw materials, work-in-progress, and finished goods held for sale to customers. Inventory management is a critical process, balancing the need to meet customer demand with the costs of storage and potential obsolescence.

- Prepaid Expenses: These are expenses that have been paid in advance but not yet consumed, such as insurance premiums or rent. As the benefit is received over time, the prepaid expense is recognized as an actual expense on the income statement.

The liquidity of current assets makes them essential for a company's working capital management. Efficient management of these assets is crucial for maintaining smooth operations and meeting short-term obligations.

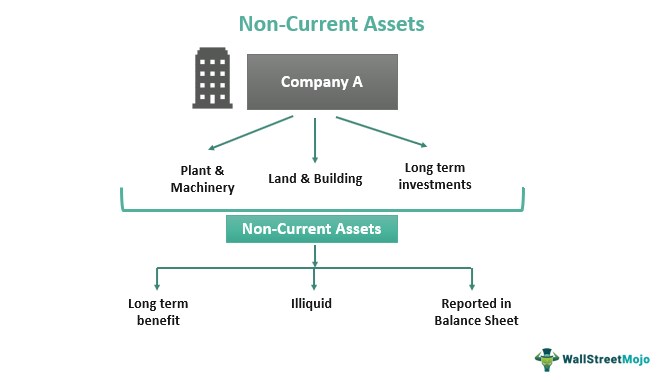

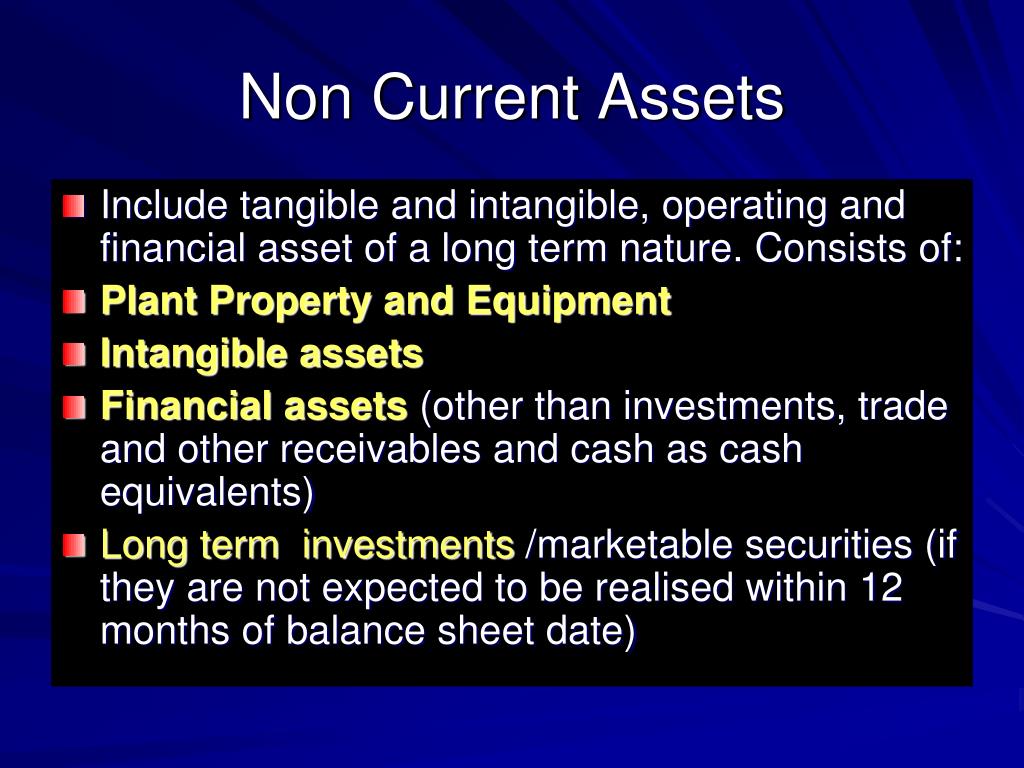

Noncurrent Assets: Long-Term Investments

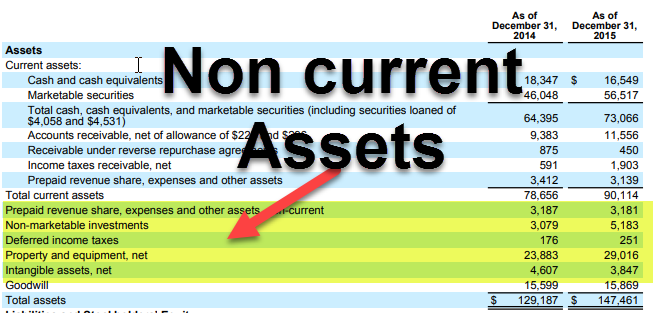

Noncurrent assets, also known as long-term assets, are assets that are not expected to be converted into cash, sold, or consumed within one year or the company's operating cycle. These assets are typically used to generate revenue over a longer period and are vital for a company's long-term growth and profitability.

Noncurrent assets can be further categorized into:

- Property, Plant, and Equipment (PP&E): These are tangible assets used in the production or supply of goods and services, for rental to others, or for administrative purposes. Examples include land, buildings, machinery, equipment, vehicles, and furniture. PP&E is typically depreciated over its useful life, reflecting the gradual decline in its value due to wear and tear, obsolescence, or usage.

- Long-Term Investments: These are investments held for more than one year, such as stocks and bonds of other companies, investments in subsidiaries or affiliates, and real estate held for investment purposes. The purpose of these investments can vary, from generating long-term returns to exerting influence over another company.

- Intangible Assets: These are assets that lack physical substance but provide future economic benefits. Examples include patents, trademarks, copyrights, goodwill, and brand names. Intangible assets can be either amortized (systematically expensed over their useful life) or tested for impairment (a reduction in their carrying value if their fair value falls below their book value). Goodwill, arising from the acquisition of another company, is not amortized but is subject to impairment testing.

- Deferred Tax Assets: These arise when taxable income is higher than accounting income, resulting in a future tax benefit. They represent the amount of income taxes recoverable in future periods as a result of temporary differences between the book value of an asset or liability and its tax basis.

Noncurrent assets represent a significant investment in a company's future. They are crucial for generating long-term revenue and supporting the company's overall business strategy.

The Significance of the Current Ratio

The current ratio is a key financial metric that provides insight into a company's ability to meet its short-term obligations. It is calculated by dividing current assets by current liabilities. A higher current ratio generally indicates a stronger ability to pay off short-term debts. A current ratio of 2:1 or higher is generally considered healthy, but the ideal ratio can vary depending on the industry.

For example, a retailer with high inventory turnover might be comfortable with a lower current ratio, while a company in a more capital-intensive industry with longer production cycles might require a higher ratio.

Depreciation and Amortization

A key difference in accounting treatment between tangible and intangible noncurrent assets lies in depreciation and amortization. Depreciation is the process of allocating the cost of a tangible asset (like PP&E) over its useful life. This reflects the consumption or decline in value of the asset over time. Various depreciation methods exist, such as straight-line, declining balance, and units of production. Amortization is the equivalent process for intangible assets with a definite useful life, such as patents or copyrights. Goodwill, however, is not amortized but is tested annually for impairment.

Impairment of Assets

Both current and noncurrent assets can be subject to impairment. Impairment occurs when the fair value of an asset falls below its carrying value on the balance sheet. For example, if a piece of equipment becomes obsolete or damaged, its carrying value may need to be reduced to reflect its lower fair value. Similarly, if the value of goodwill declines due to poor performance of the acquired company, an impairment loss may need to be recognized.

Presentation on the Balance Sheet

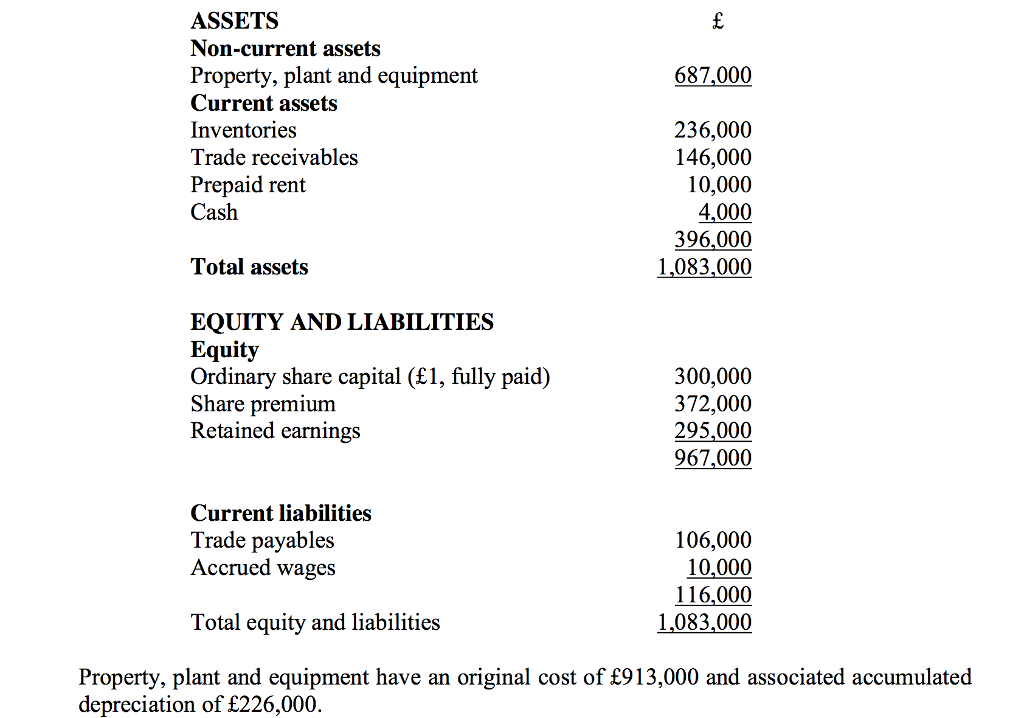

The balance sheet is a snapshot of a company's assets, liabilities, and equity at a specific point in time. Current and noncurrent assets are presented separately on the balance sheet, typically in order of liquidity. Current assets are listed first, followed by noncurrent assets. This presentation allows users of financial statements to quickly assess a company's financial position and its ability to meet its obligations.

Key Takeaways

Here's a summary of the key differences between current and noncurrent assets:

- Time Horizon: Current assets are expected to be converted into cash or used within one year or the operating cycle, while noncurrent assets are expected to provide benefits for more than one year.

- Liquidity: Current assets are generally more liquid than noncurrent assets, meaning they can be easily converted into cash.

- Purpose: Current assets are used to meet short-term obligations and support day-to-day operations, while noncurrent assets are used to generate long-term revenue and support the company's overall business strategy.

- Examples: Common current assets include cash, accounts receivable, and inventory. Common noncurrent assets include PP&E, long-term investments, and intangible assets.

- Depreciation/Amortization: Tangible noncurrent assets (PP&E) are depreciated, while intangible assets with a definite life are amortized. Goodwill is not amortized but is tested for impairment.

Understanding the distinction between current and noncurrent assets is essential for financial analysis, investment decisions, and overall business management. By carefully classifying and managing these assets, companies can optimize their financial performance and achieve their strategic goals.

:max_bytes(150000):strip_icc()/dotdash_Final_How_Current_and_Noncurrent_Assets_Differ_Oct_2020-01-e74218e547134e3db0ac9e9a7446d577.jpg)

:max_bytes(150000):strip_icc()/Exxon-265fb0cef5f04c359ca78ad24048d312.jpg)

:max_bytes(150000):strip_icc()/noncurrent-assets-resized-583d5c0e1a224b66b1909594c0376714.jpg)