Unused Line Of Credit On Balance Sheet

Okay, let's talk about something that sounds super intimidating: an unused line of credit on a balance sheet. I know, I know. Sounds like accounting jargon only accountants understand, right? But trust me, it's not as scary as it seems. Think of it like that gym membership you bought in January with the best of intentions, that's just sitting there, unused, month after month.

See? We’re already connecting this to real life. We've all been there.

What is a Line of Credit, Anyway?

First, let's break down what a line of credit actually is. Imagine you have a really, really good friend named "Banky." (Okay, maybe not, but go with it). Banky says, "Hey, I trust you. Here's access to, let's say, $10,000. You don't have to take it right now. It's just there, if you need it. But if you do use it, you'll have to pay me back with a little extra on top (interest, the price for renting the money)."

Must Read

That's essentially a line of credit! It's pre-approved access to a certain amount of money. You only pay interest on what you actually borrow, not the total amount available.

Personal vs. Business: Same Concept, Different Scale

You can get a line of credit personally (often called a personal line of credit or a home equity line of credit – HELOC) or for your business. The concept is the same. For a business, it’s typically used for short-term needs like covering payroll, purchasing inventory, or smoothing out cash flow dips.

Think of the small bakery down the street. Maybe they take out a line of credit to buy extra flour and sugar before the holiday rush. They might not need it every month, but it's there as a safety net. That’s smart business.

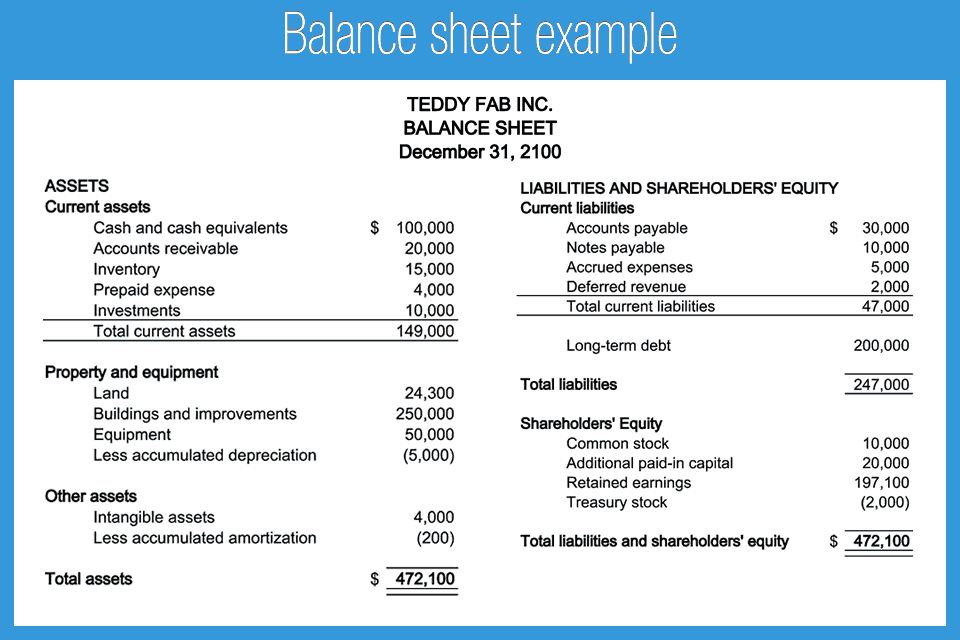

The Balance Sheet: Where the Magic (or the Murk) Happens

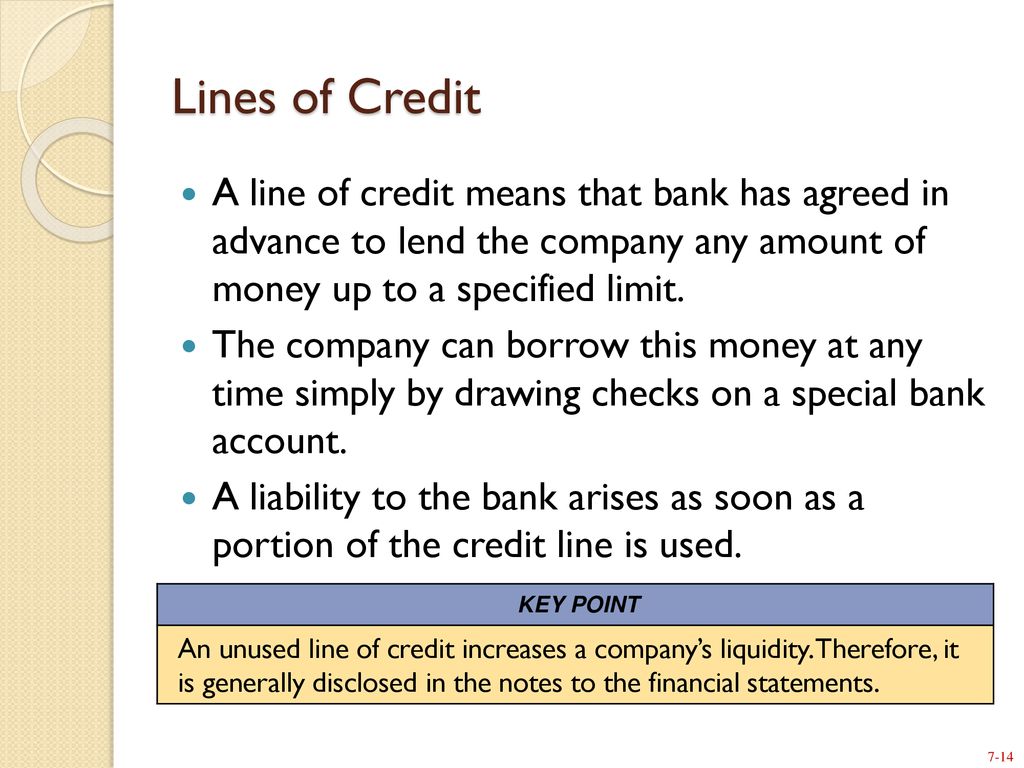

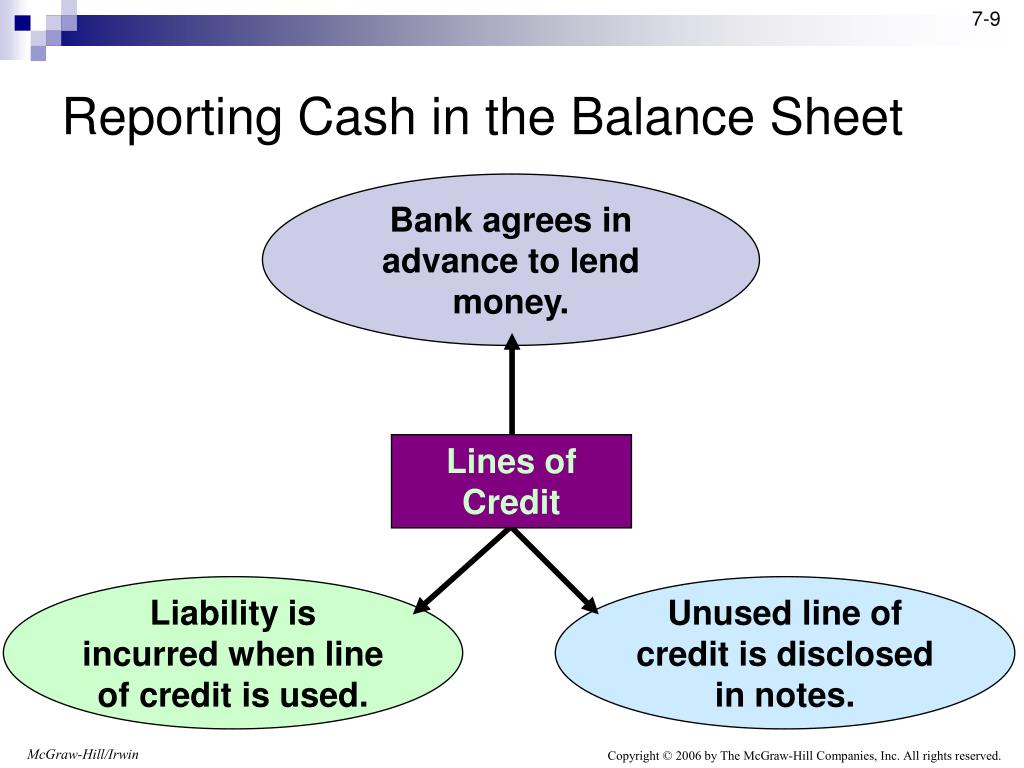

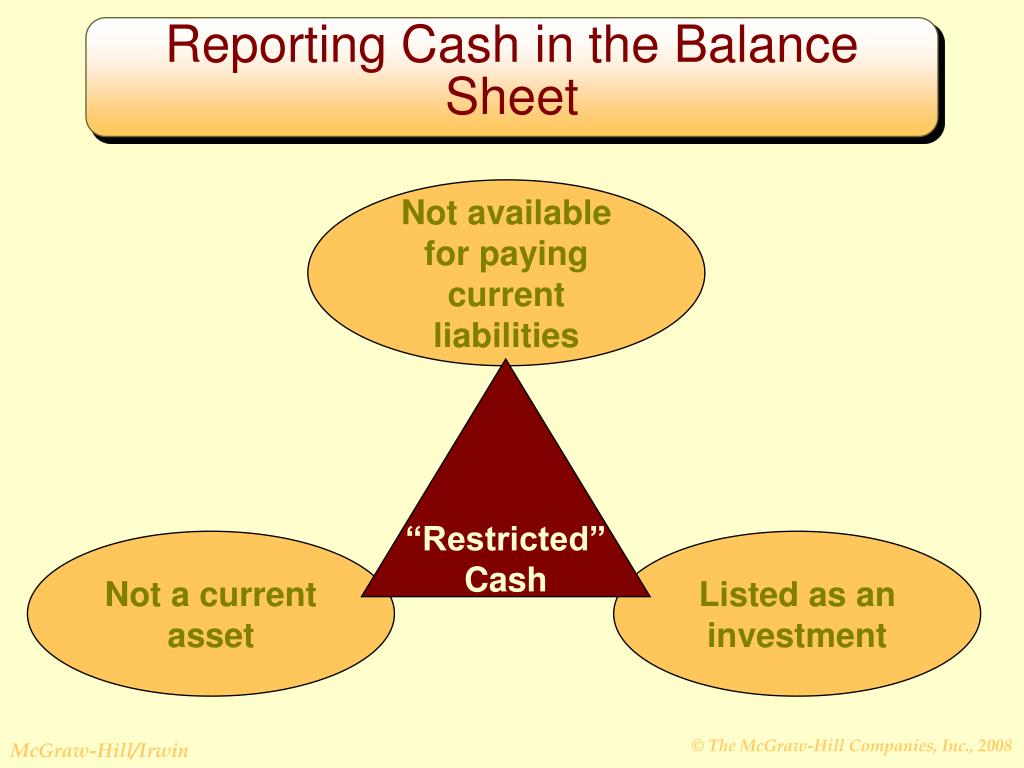

Alright, now let's bring in the balance sheet. A balance sheet is like a snapshot of a company's financial health at a specific point in time. It shows what the company owns (assets), what it owes (liabilities), and the owner's equity (the difference between assets and liabilities). It's like a financial selfie! And our unused line of credit makes an appearance here, specifically in the liabilities section.

Now, why is it there if it’s unused? Good question! Even though you haven't borrowed the money, the availability of that credit is a financial obligation. You could borrow it at any time, and the bank is committed to lending it to you (within the terms of the agreement, of course). Therefore, it's disclosed in the footnotes of the balance sheet as a contingent liability.

Think of it like this: You have a credit card with a $5,000 limit, and you haven't used it. It doesn't show up as debt on your credit report (yet!), but the fact that you could potentially rack up $5,000 in debt is still…well, a fact. The unused line of credit is similar. It's a potential liability waiting in the wings.

Why is an Unused Line of Credit a Good Thing? (Mostly)

Believe it or not, having an unused line of credit can actually be a good thing. Here's why:

- Financial Flexibility: It's a safety net! Unexpected expenses happen. Maybe a crucial piece of equipment breaks down, or a major client is late on a payment. The line of credit provides a financial cushion to weather the storm. It's like having a spare tire in your car – you hope you don't need it, but you're grateful it's there when you do.

- Improved Creditworthiness: Having a line of credit and managing it responsibly (i.e., not maxing it out) can actually improve your company's credit score. It shows lenders that you're capable of handling debt and that you're a reliable borrower. It’s kind of like having a good relationship with your landlord.

- Opportunity to Seize Opportunities: Sometimes, opportunities arise unexpectedly. Maybe a competitor is having a fire sale on inventory, or a prime piece of real estate becomes available. A line of credit can give you the financial firepower to jump on these opportunities quickly. It enables you to be agile in response to market changes.

However, there are some potential downsides:

- Fees: Some lines of credit come with annual fees, even if you don't use them. It's like paying for that gym membership even when you only go twice a year. Make sure you understand the fee structure before agreeing to the line of credit.

- Temptation: Having access to extra cash can be tempting to overspend, even on things you don't really need. It's important to be disciplined and only use the line of credit for legitimate business needs. Don't buy that giant inflatable flamingo for the office just because you can.

- Impact on Debt Ratios: While the unused portion isn't technically debt, it can impact your debt-to-equity ratio, even if you don't take from it. If you are looking to take out additional loans, lenders will take the total amount available to you into consideration, not just the amount you are currently borrowing.

Decoding the Footnotes: Finding the Unused Line of Credit

Okay, so where exactly on the balance sheet is this thing? As mentioned earlier, it's usually disclosed in the footnotes. Footnotes are the unsung heroes of financial statements. They provide additional information and explanations about the numbers you see on the main balance sheet, income statement, and cash flow statement.

Look for a section on "Contingencies" or "Commitments." You should find a description of the line of credit, including the total amount available, the interest rate, and any other key terms. It might say something like, "The company has a $500,000 line of credit with Banky at an interest rate of prime + 2%. As of December 31, 2023, $0 has been drawn on the line of credit."

Reading financial statements can be intimidating. It can feel like trying to read another language. But the more you expose yourself to these documents, the better you will understand what they mean. Reading the footnotes can provide you additional information about the company that you're assessing.

Unused Line of Credit: A Business's Trusty Sidekick

In conclusion, an unused line of credit on a balance sheet isn't some mysterious accounting monster. It's simply a readily available source of funds that can provide financial flexibility and opportunity for a business. It's like having a secret weapon in your financial arsenal. However, it's important to understand the terms and conditions of the line of credit and to use it responsibly.

So, next time you hear someone talking about an unused line of credit, don't glaze over with boredom. Remember your unused gym membership, and remember that it can be a valuable asset (especially if you ever decide to actually use that gym membership).

And remember, understanding your company's financials is key to making informed decisions and steering your business towards success. Now, go forth and conquer the world (or at least your balance sheet)!

By the way, are you using that gym membership or nah?

:max_bytes(150000):strip_icc()/dotdash_Final_Line_of_Credit_LOC_May_2020-01-b6dd7853664d4c03bde6b16adc22f806.jpg)

:max_bytes(150000):strip_icc()/how-a-line-of-credit-works-315642-UPDATED-50c98a253c7f42dabfc4111f574dc016.png)