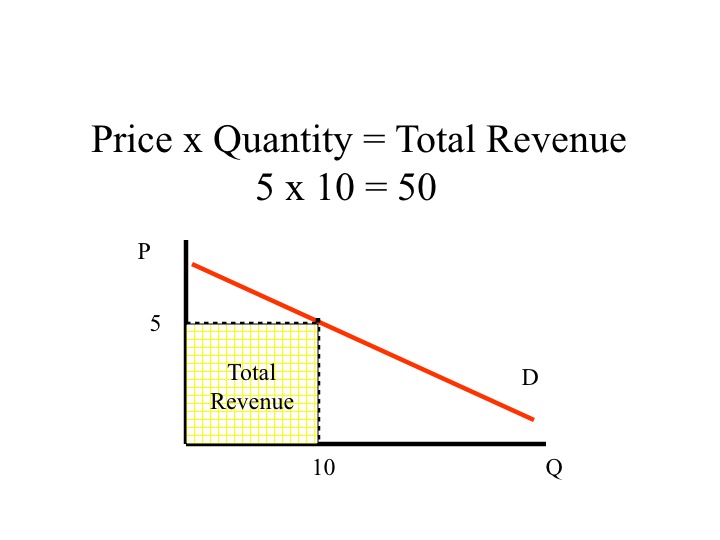

Unit Price X Quantity Sold Total Cost

The fundamental equation of “Unit Price x Quantity Sold = Total Cost” underpins countless commercial transactions. This seemingly simple formula belies a complex interplay of factors that determine the financial viability of businesses and the overall health of economies. Understanding the causes, effects, and implications of each element within this equation is crucial for effective decision-making in various contexts, from individual consumers to multinational corporations.

Causes Affecting Unit Price

The unit price, the cost of a single item or service, is rarely an arbitrary figure. It's the result of a confluence of market forces, production costs, and strategic decisions. Several factors can contribute to its fluctuation.

Supply and Demand

Perhaps the most fundamental driver of unit price is the relationship between supply and demand. If demand for a product exceeds its supply, prices tend to rise. Conversely, if supply outstrips demand, prices are likely to fall. This principle is illustrated in various industries. For example, during the COVID-19 pandemic, the demand for personal protective equipment (PPE) such as masks and hand sanitizer skyrocketed. Due to limited supply chains and manufacturing capacity, unit prices for these items experienced dramatic increases, sometimes exceeding tenfold their pre-pandemic levels. Similarly, agricultural commodities are highly susceptible to supply and demand dynamics. A drought, for example, can significantly reduce crop yields, leading to higher prices for agricultural products.

Must Read

Production Costs

The costs associated with producing a good or service directly influence its unit price. These costs encompass raw materials, labor, manufacturing overhead, and research and development. An increase in any of these components will likely translate into a higher unit price. For instance, the price of gasoline is directly linked to the price of crude oil. Geopolitical events that disrupt oil production or increase the cost of extraction often lead to higher prices at the pump. Similarly, technological advancements can sometimes lower production costs, enabling businesses to offer products at a lower unit price. The development of more efficient manufacturing processes in the electronics industry, for example, has contributed to the declining prices of smartphones and other electronic devices over time.

Competition

The level of competition within a market significantly impacts pricing strategies. In highly competitive markets, businesses may be forced to lower their unit prices to attract customers and maintain market share. This often leads to price wars, where competitors engage in successive price cuts to gain an edge. Conversely, in markets with limited competition, businesses have more pricing power and can charge higher unit prices. Consider the pharmaceutical industry. Companies holding patents for life-saving drugs often face little competition, allowing them to set relatively high prices. However, once patents expire and generic versions become available, competition intensifies, and unit prices typically decline significantly.

Government Regulations and Taxes

Government interventions, such as taxes, subsidies, and regulations, can also affect unit prices. Taxes, like sales taxes or excise taxes, directly increase the price consumers pay for goods and services. Subsidies, on the other hand, can lower the cost of production, enabling businesses to offer products at lower prices. Regulations, such as environmental regulations or safety standards, can increase production costs, potentially leading to higher unit prices. For example, carbon taxes implemented to mitigate climate change can increase the price of energy and goods produced using fossil fuels.

Causes Affecting Quantity Sold

The quantity sold, representing the number of units purchased by consumers, is equally subject to various influences. Understanding these influences is critical for sales forecasting and inventory management.

Price Elasticity of Demand

The price elasticity of demand measures the responsiveness of quantity demanded to changes in price. Goods and services with high price elasticity experience significant changes in quantity sold when prices fluctuate. For example, luxury goods often exhibit high price elasticity, as consumers may be more willing to forgo these items if prices increase. In contrast, essential goods like food or medicine tend to have low price elasticity, meaning that demand remains relatively stable even with price changes. Understanding price elasticity is crucial for businesses when considering price adjustments.

Consumer Income and Preferences

Consumer income and preferences play a significant role in determining the quantity sold. As income levels rise, consumers tend to purchase more goods and services, particularly those considered non-essential. Changes in consumer preferences, driven by trends, advertising, or evolving tastes, can also significantly impact demand. The rise of veganism, for example, has led to a substantial increase in the quantity sold of plant-based food products.

Marketing and Promotion

Effective marketing and promotional activities can significantly boost the quantity sold. Advertising campaigns, discounts, coupons, and other promotional strategies can attract new customers and incentivize existing customers to purchase more. A well-executed marketing campaign can create brand awareness, build customer loyalty, and ultimately drive sales volume. The success of Apple's marketing campaigns, for instance, has consistently contributed to high sales volumes for its products.

Availability and Distribution

The availability and distribution of a product directly affect the quantity sold. If a product is readily available in convenient locations, consumers are more likely to purchase it. Effective distribution networks and strong retail partnerships are essential for maximizing sales. The expansion of e-commerce platforms has significantly increased the accessibility of a wide range of products, leading to higher sales volumes for many businesses.

Effects and Implications on Total Cost

The total cost, the product of unit price and quantity sold, represents the total revenue generated from the sale of a product or service. It is a key metric for assessing profitability and financial performance.

Profitability and Revenue

Total cost directly impacts a company's profitability and revenue. Higher total cost, assuming costs are managed effectively, translates to greater revenue and potentially higher profits. Businesses strive to optimize their pricing and sales strategies to maximize total cost and achieve their financial goals. However, increasing total cost at the expense of profitability is unsustainable. Businesses must carefully balance unit price and quantity sold to achieve optimal financial performance.

Market Share

Total cost can also be an indicator of market share. A company with a higher total cost compared to its competitors may have a larger market share, indicating greater brand recognition and customer loyalty. However, a higher total cost can also be a result of higher unit prices, potentially making a company vulnerable to competition from lower-priced alternatives. Balancing competitive pricing with profitability is a constant challenge for businesses.

Investment Decisions

Total cost is a crucial factor in investment decisions. Investors analyze a company's total cost and its underlying components to assess its financial health and growth potential. Companies with consistently increasing total cost are often viewed as attractive investment opportunities, signaling strong sales growth and market expansion. However, investors also scrutinize the drivers of total cost growth, ensuring that it is sustainable and not driven by unsustainable pricing practices or excessive promotional spending.

Economic Indicators

Aggregated total cost data can serve as valuable economic indicators. Tracking total cost across various industries and sectors can provide insights into consumer spending patterns, inflation trends, and overall economic growth. For example, a significant increase in total cost for consumer goods may indicate rising consumer demand or inflationary pressures. Government agencies and economists often use total cost data to monitor economic performance and make informed policy decisions.

Broader Significance

The equation "Unit Price x Quantity Sold = Total Cost" transcends mere financial calculation. It mirrors fundamental principles of resource allocation, economic activity, and consumer behavior. A society's collective decisions around production, consumption, and pricing influence everything from resource sustainability to wealth distribution. Understanding these interconnections helps individuals make informed choices as consumers, businesses develop sustainable strategies, and policymakers create effective economic policies. Ignoring the nuanced interplay within this equation can lead to unsustainable economic practices, market distortions, and ultimately, reduced overall well-being.