The Term Fractional Reserves Refers To

The concept of fractional reserves is fundamental to understanding modern banking systems and how money is created and managed within an economy. It's a system where banks are required to hold only a fraction of their deposits in reserve, lending out the remaining portion. This allows banks to effectively create new money, playing a crucial role in economic growth and stability.

What are Fractional Reserves?

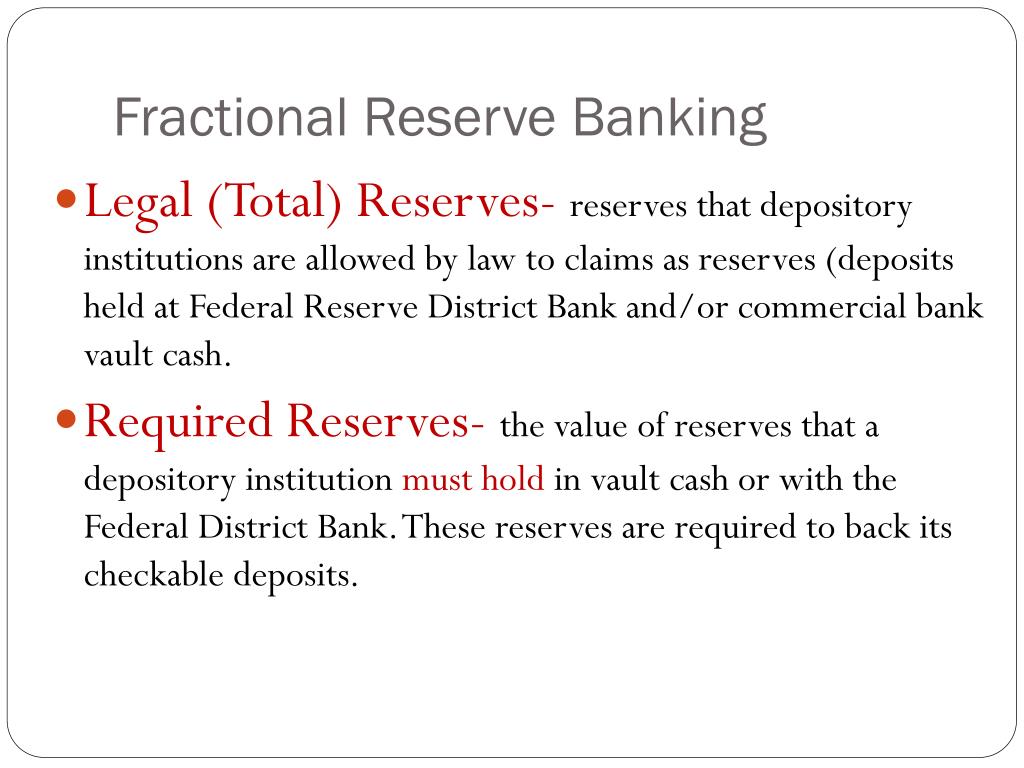

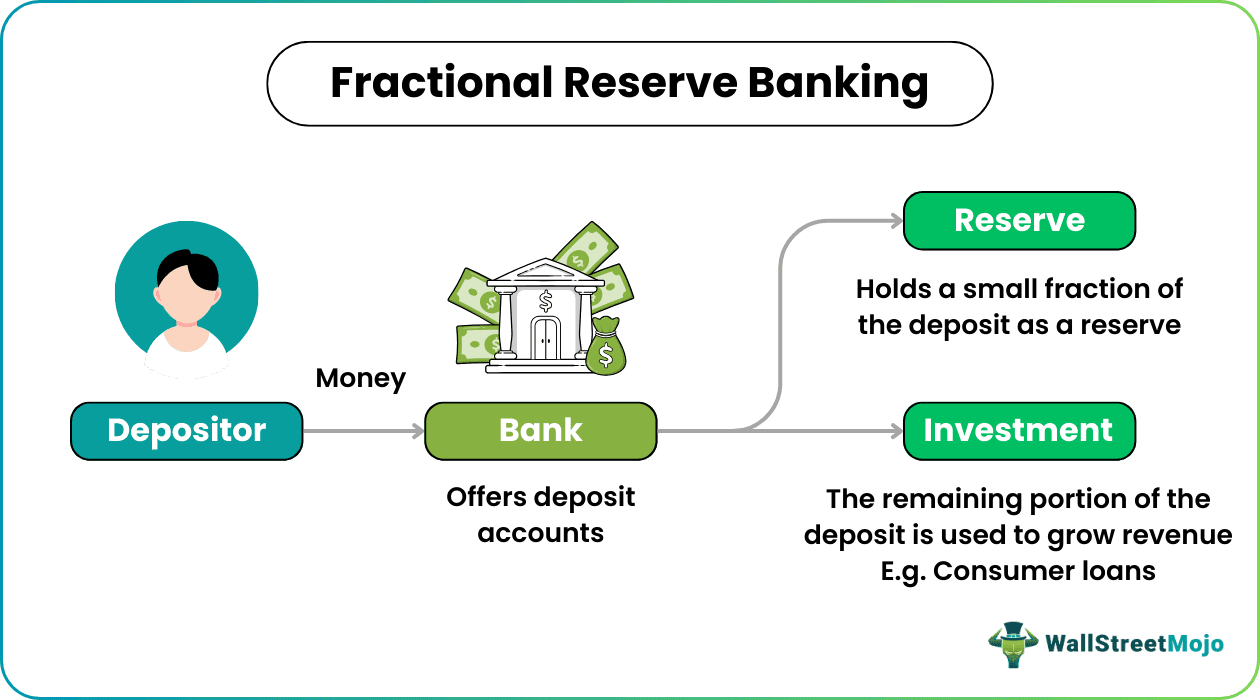

At its core, the term "fractional reserves" refers to the practice where banks retain only a percentage of their customers’ deposits as readily available cash. This percentage is known as the reserve requirement. The rest of the money deposited can then be used by the bank for lending, investments, and other profit-generating activities.

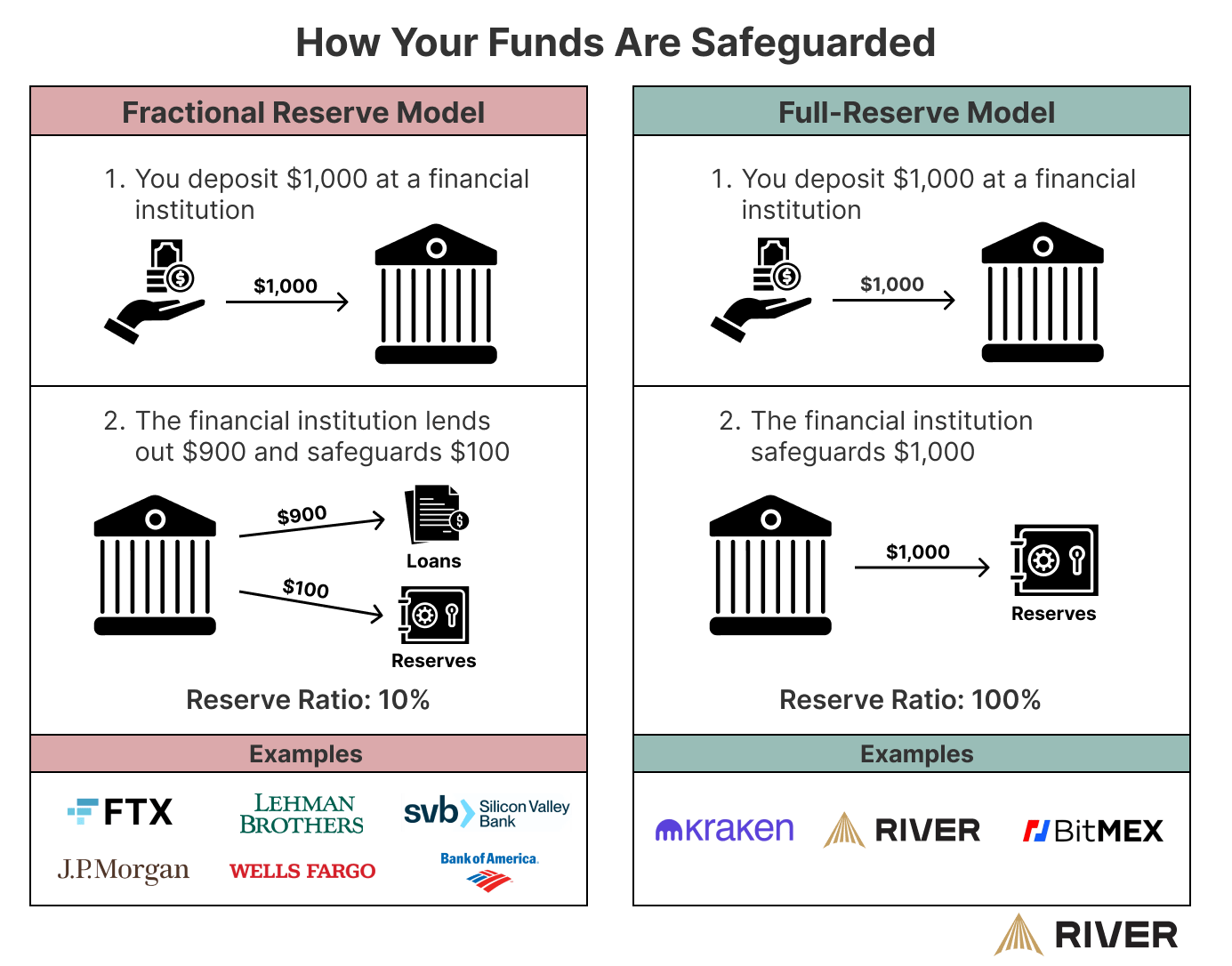

Imagine a scenario where you deposit $1,000 into your bank account. If the reserve requirement is 10%, the bank is legally obligated to keep $100 on hand. The remaining $900 can be lent out to another customer, such as someone seeking a loan to buy a car or a house. This process forms the basis of fractional reserve banking.

Must Read

It's important to understand that the bank doesn't physically take your $1,000 and divide it. Instead, it uses the deposit as a basis for making new loans, essentially creating new credit in the economy. Your account balance still reflects the full $1,000, and you can withdraw it as needed (assuming sufficient liquidity). However, the bank is simultaneously using a portion of that deposit to support loans and other financial activities.

The Reserve Requirement

The reserve requirement is a percentage set by the central bank (e.g., the Federal Reserve in the United States) that dictates the minimum amount of deposits commercial banks must hold in reserve. This requirement can be met by keeping physical cash in the bank's vault or by holding funds in an account at the central bank.

The reserve requirement is a crucial tool used by central banks to influence the money supply and credit conditions in an economy. By adjusting the reserve requirement, the central bank can encourage banks to lend more or less money. A lower reserve requirement allows banks to lend out a larger portion of their deposits, increasing the money supply and potentially stimulating economic growth. Conversely, a higher reserve requirement forces banks to hold more reserves, reducing the amount of money available for lending and potentially slowing down economic activity.

Factors Influencing the Reserve Requirement

Several factors influence the level at which a central bank sets the reserve requirement:

- Economic Conditions: During periods of economic recession or slowdown, central banks may lower reserve requirements to encourage lending and stimulate economic activity. In contrast, during periods of rapid economic growth or inflation, central banks may raise reserve requirements to curb lending and cool down the economy.

- Inflation: High inflation often prompts central banks to increase reserve requirements to reduce the money supply and slow down price increases.

- Financial Stability: Central banks may adjust reserve requirements to promote financial stability by influencing the amount of credit available in the economy.

- Monetary Policy Goals: Reserve requirements are just one tool in a central bank’s toolkit for achieving its overall monetary policy goals, which typically include price stability, full employment, and sustainable economic growth.

The Money Multiplier Effect

Fractional reserve banking creates a phenomenon known as the money multiplier effect. This describes how an initial deposit can lead to a larger increase in the overall money supply. It works as follows:

- You deposit $1,000.

- The bank keeps 10% ($100) as a reserve and lends out $900.

- The borrower spends the $900, which ends up deposited into another bank.

- This second bank keeps 10% ($90) and lends out $810.

- The process continues, with each subsequent loan creating new deposits.

The money multiplier (k) is calculated as: k = 1 / Reserve Requirement.

In our example, with a 10% reserve requirement, the money multiplier is 1 / 0.10 = 10. This means that the initial $1,000 deposit could potentially lead to a $10,000 increase in the money supply through the fractional reserve banking system.

It's important to note that the actual money multiplier effect is often less than the theoretical maximum. Factors such as individuals holding cash instead of depositing it, and banks choosing to hold reserves above the required level, can reduce the overall impact.

Risks and Benefits of Fractional Reserve Banking

Fractional reserve banking offers significant benefits to the economy but also carries certain risks:

Benefits:

- Economic Growth: By allowing banks to lend out a significant portion of their deposits, fractional reserve banking fuels economic growth by providing capital for businesses to expand, individuals to purchase homes, and governments to invest in infrastructure.

- Increased Liquidity: Fractional reserve banking allows for a more efficient use of capital, increasing the liquidity of the financial system and facilitating transactions.

- Profitability for Banks: Lending out deposits allows banks to generate profits through interest income, which is essential for their financial stability and ability to provide banking services.

Risks:

- Bank Runs: If a large number of depositors simultaneously attempt to withdraw their funds (a bank run), the bank may not have enough reserves to meet the demand, leading to its collapse. This is because the bank has lent out a significant portion of its deposits.

- Financial Instability: Overly aggressive lending practices, fueled by low reserve requirements, can lead to asset bubbles and financial instability.

- Inflation: Excessive money creation through fractional reserve banking can lead to inflation if the money supply grows faster than the economy's ability to produce goods and services.

To mitigate these risks, central banks and regulatory agencies implement various safeguards, including deposit insurance, bank supervision, and stress testing, to ensure the stability of the financial system.

The Debate Surrounding Fractional Reserve Banking

Fractional reserve banking is a subject of ongoing debate among economists and policymakers. Some argue that it is an essential component of a modern economy, enabling economic growth and facilitating transactions. Others criticize it for its potential to create financial instability and contribute to boom-and-bust cycles.

Critics often point to the fact that fractional reserve banking essentially creates money out of thin air, which they argue can lead to inflation and distort economic incentives. They suggest that alternative banking systems, such as full-reserve banking, would be more stable and less prone to crises.

Proponents of fractional reserve banking, on the other hand, argue that it is a necessary condition for a dynamic and growing economy. They contend that the risks associated with fractional reserve banking can be effectively managed through appropriate regulation and supervision.

Conclusion

In summary, the term "fractional reserves" describes a system where banks are required to hold only a fraction of their deposits in reserve, allowing them to lend out the remaining portion and create new money. This system plays a crucial role in modern economies by facilitating economic growth and increasing liquidity. However, it also carries risks, such as bank runs and financial instability, which must be carefully managed through regulation and supervision. Understanding fractional reserve banking is essential for grasping how money is created and managed, and its impact on the overall economy.

:max_bytes(150000):strip_icc()/fractionalreservebanking.asp-final-a5faeb741c464711ba434ee652c40ebf.png)