The Risk Of Loss May Be Classified As

Hey friend! Ever bought something online and then felt that tiny, nagging worry in the back of your head? You know, the "what if it gets lost?" anxiety? That, my friend, is the risk of loss, and it's surprisingly complex. Let's dive in, shall we? (Grab your coffee – this might take a minute!)

So, what exactly is this "risk of loss" we're talking about? Simply put, it's the risk that goods will be damaged, destroyed, or lost before they reach the lucky person who's supposed to receive them. It's basically the universe saying, "Ha! You thought you were getting that awesome new gadget? Think again!" Okay, maybe not that dramatic, but you get the idea.

Classifying the Beast: How Risk of Loss Gets Sorted

Now, here's where things get interesting. The risk of loss isn't just some vague, amorphous blob of bad luck. Oh no. It's actually classified and categorized. We love categories, don't we? It's like organizing your sock drawer – satisfying and strangely important! So how do we sort out the potential loss? It's all about who's responsible when things go south.

Must Read

By Contract: The "Read the Fine Print" Scenario

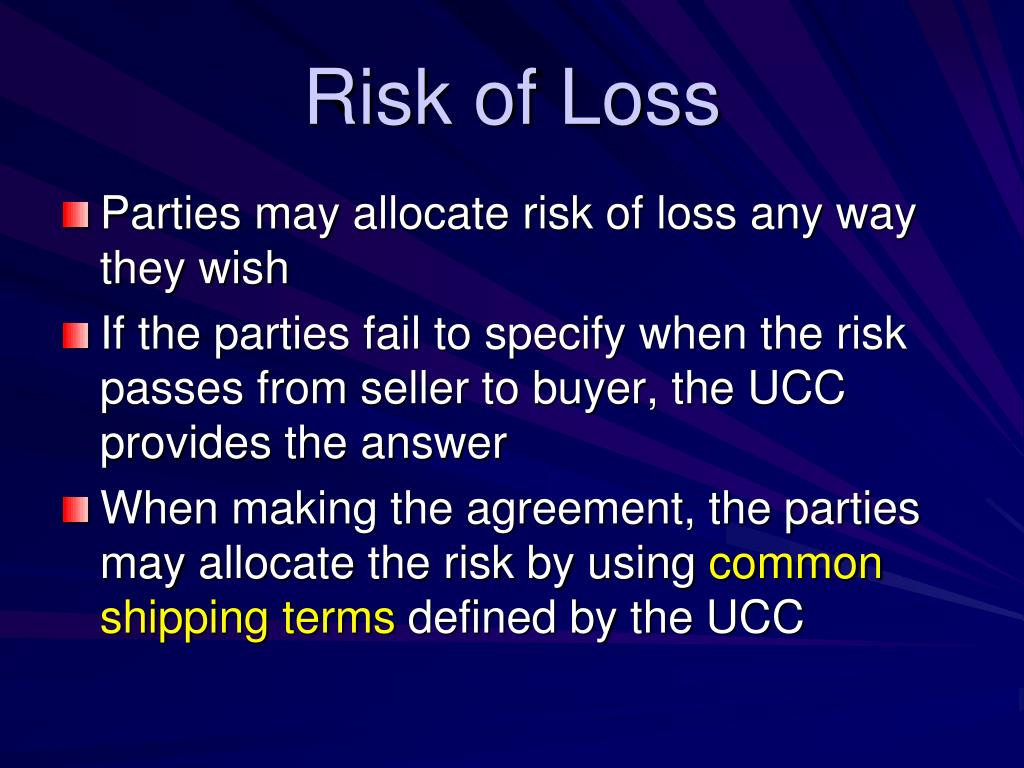

This is where the terms of the sale come into play. Did you actually read that ridiculously long agreement you clicked "I agree" to? Probably not. (Don't worry, nobody does!) But buried in there somewhere might be a clause about who's responsible if your package ends up at the bottom of the ocean. Sales contracts often explicitly state who bears the risk of loss. It can be the seller until the item is delivered, the buyer the moment it leaves the seller's hands, or some other creative arrangement. It all depends on the agreement!

For instance, you might see something like "FOB Shipping Point." That means the buyer takes on the risk of loss as soon as the seller ships the goods. "FOB Destination," on the other hand, means the seller is responsible until the goods reach the buyer's specified destination. See? Tricky stuff! Like a legal escape room!

And what if there's no specific agreement? Ah, that's where the law steps in to play referee.

By Negligence: Who Messed Up?

Okay, imagine this: a delivery driver is texting while driving (never a good idea!) and crashes the truck, destroying your precious package of artisanal cheese. (Tragedy!) In this case, the risk of loss might fall on the negligent party – in this case, the delivery company – because their actions directly caused the loss. Negligence, in legal terms, basically means someone didn't exercise reasonable care, and their carelessness resulted in damage or loss.

It's not always as straightforward as a truck crash, though. What if a warehouse employee leaves a pallet of delicate glassware out in the rain? Negligence! What if a shipping company fails to properly secure a load of expensive electronics? Negligence again! It's all about proving that someone's carelessness contributed to the loss.

By Type of Goods: Are They Fungible?

Fungible? Sounds like a fungus, right? Well, not exactly. In legal terms, fungible goods are things that are interchangeable. Think grain, oil, or even money. If you're buying 100 bushels of wheat, it doesn't really matter which 100 bushels you get, as long as they're of the agreed-upon quality. Because each unit is essentially the same as the next.

When dealing with fungible goods, the risk of loss can sometimes be determined by identification. This means figuring out which specific goods were intended for the buyer. If those specific goods are damaged or lost, then the risk of loss falls on whoever owned them at the time. If they're all mixed together and impossible to identify, then it gets a little more complicated. (Legal complications are lawyers' bread and butter, you know.)

By Insurable Interest: Who Has Skin in the Game?

This one is all about insurance. If you have an insurable interest in goods, you can insure them against loss or damage. This means you would suffer a financial loss if something happened to those goods. The person with the insurable interest usually bears the risk of loss, at least up to the amount of the insurance coverage. Banks often have insurable interest in items if they have helped pay for them on behalf of someone else. They might require a borrower to get insurance, to minimize their own risk exposure.

Think of it like this: if you're buying a car, you probably want to get insurance on it, right? That's because you have an insurable interest – you'd lose a lot of money if the car got totaled. Similarly, businesses often insure their inventory to protect themselves against losses due to fire, theft, or other disasters.

By Bailment: Handing Over the Keys (Literally!)

Okay, "bailment" sounds super fancy, right? But it's actually pretty simple. A bailment is basically when you temporarily hand over possession of your goods to someone else. Like if you take your watch to a jeweler for repair, or if you store your furniture in a storage unit. You, as the owner, are the bailor. The person who takes possession of your goods is the bailee.

In a bailment situation, the bailee usually has a duty of care to protect your goods from loss or damage. If they're negligent and your goods are harmed, they could be held liable for the loss. But the exact responsibilities depend on the type of bailment. For example, a "gratuitous bailment" (where the bailee is doing you a favor) might have a lower standard of care than a "bailment for hire" (where you're paying the bailee for their services).

Who Cares About All This? (Besides Lawyers, of Course!)

Okay, so you might be thinking, "Why should I care about all these classifications? I just want my package to arrive in one piece!" Fair enough. But understanding the risk of loss can be crucial in a few situations:

- Negotiating Contracts: Knowing who bears the risk of loss can give you leverage when negotiating sales agreements. You might be able to negotiate for more favorable terms, like having the seller bear the risk until the goods reach your doorstep.

- Protecting Your Business: If you're a business owner, understanding the risk of loss is essential for managing your inventory and ensuring you're adequately insured.

- Resolving Disputes: If goods are lost or damaged, knowing the rules about risk of loss can help you determine who's responsible and whether you have a valid claim.

- Simply Being Informed: It's always good to know your rights and responsibilities! Plus, you can impress your friends at parties with your newfound knowledge of bailments and fungible goods. (Okay, maybe not. But you could try!)

Ultimately, the risk of loss is a complex area of law that depends on a variety of factors. But by understanding the basic principles, you can better protect yourself and your valuable possessions. So, the next time you buy something online, take a moment to think about the risk of loss. And maybe, just maybe, read the fine print. (Okay, probably not. But you could consider it!)

It may sound complicated, but understanding the basic principles can save you a headache (and potentially a lot of money) down the line. Think of it as adulting 101 – a slightly boring, but ultimately useful skill to have in your back pocket. Now, go forth and conquer the world of commerce, armed with your knowledge of risk of loss!

+Contract+is+Breached..jpg)