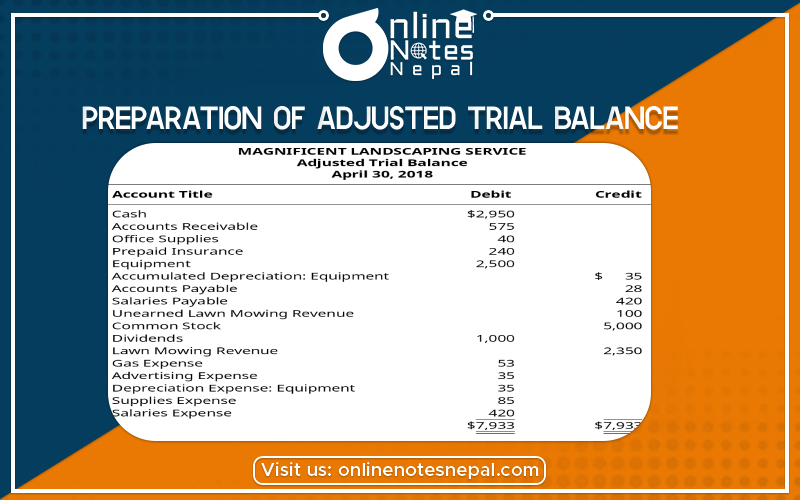

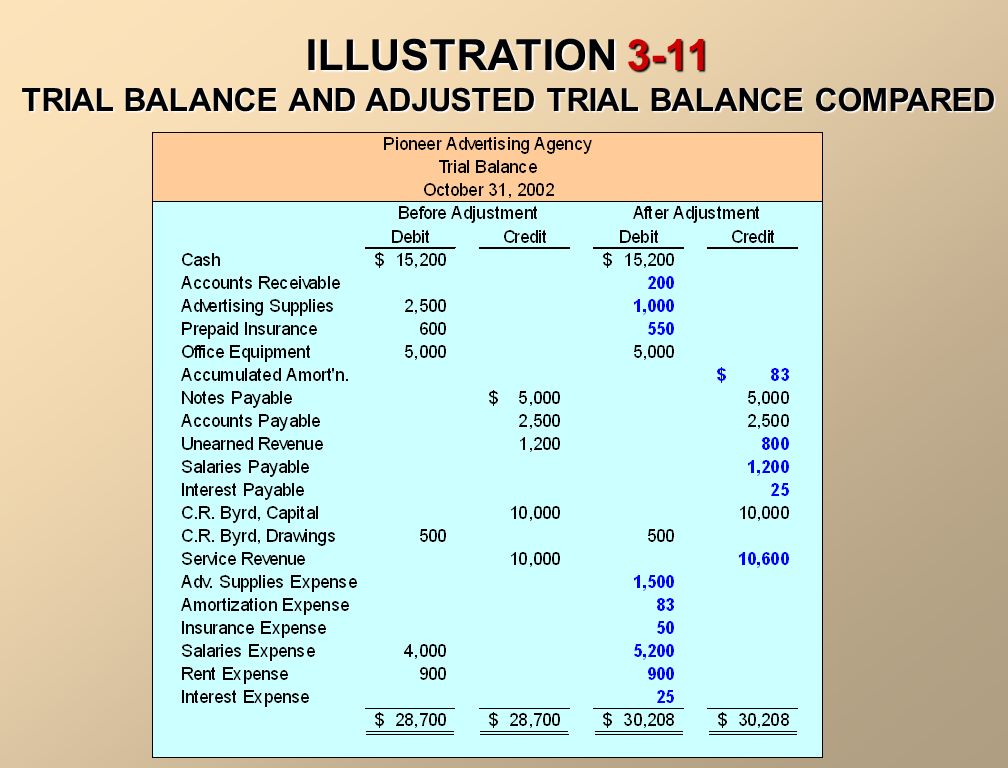

The Adjusted Trial Balance Is Prepared

The adjusted trial balance is a crucial step in the accounting cycle. It follows the initial preparation of a trial balance and the subsequent recording of adjusting entries. This process ensures the accuracy and reliability of financial statements.

Purpose of the Adjusted Trial Balance

The primary goal of preparing an adjusted trial balance is to verify the equality of debit and credit balances in the general ledger after adjusting entries have been posted. Adjusting entries are necessary to update account balances for items that were not previously recorded correctly or to reflect the proper revenue and expense recognition under the accrual accounting method. These entries are vital for presenting a fair and accurate representation of a company's financial position and performance.

When It's Prepared

The adjusted trial balance is typically prepared at the end of an accounting period, which can be monthly, quarterly, or annually. It is created after all adjusting entries have been journalized and posted to the ledger accounts but before the preparation of the financial statements (income statement, balance sheet, and statement of cash flows).

Must Read

The Process of Preparing the Adjusted Trial Balance

The creation of an adjusted trial balance follows a systematic approach:

- Prepare the Initial Trial Balance: This is the first step. The initial trial balance lists all general ledger accounts and their debit or credit balances at a specific point in time. Its purpose is to prove the mathematical equality of debits and credits. If debits do not equal credits, an error exists and must be located and corrected before proceeding.

- Identify the Need for Adjusting Entries: Analyze the accounts in the initial trial balance to identify areas that require adjustments. Common examples include:

- Accrued revenues (revenues earned but not yet received).

- Accrued expenses (expenses incurred but not yet paid).

- Deferred revenues (cash received but not yet earned).

- Deferred expenses (cash paid but not yet used).

- Depreciation expense (allocation of the cost of a long-term asset over its useful life).

- Bad debt expense (estimation of uncollectible accounts receivable).

- Journalize and Post Adjusting Entries: Prepare the necessary adjusting entries in the general journal and post them to the respective ledger accounts. Each adjusting entry impacts at least one income statement account (revenue or expense) and one balance sheet account (asset or liability).

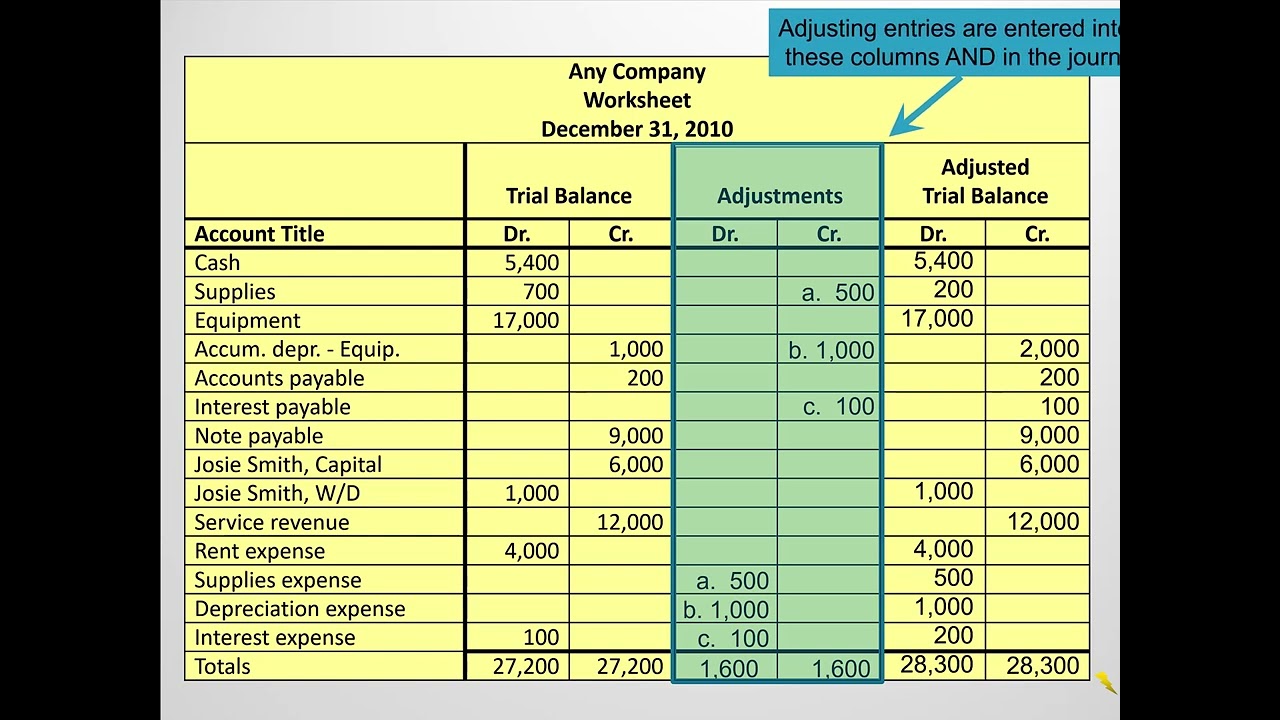

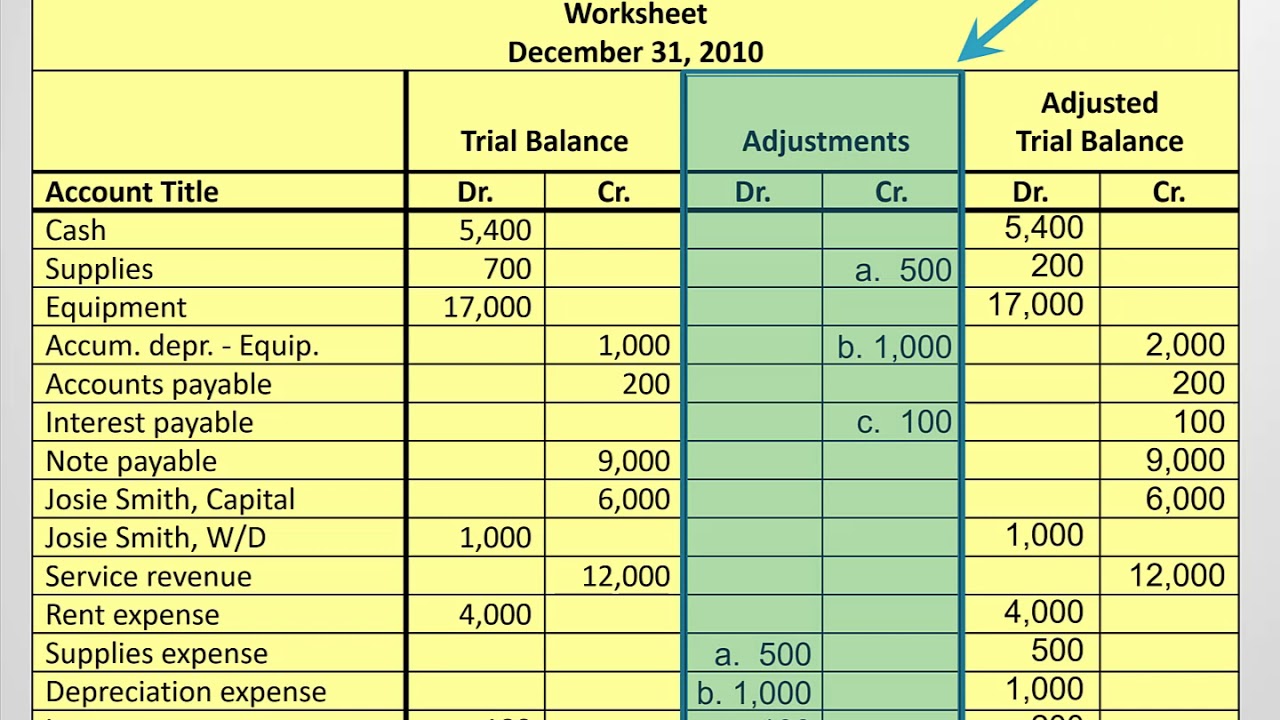

- Prepare the Adjusted Trial Balance Worksheet: This is a working paper, not a formal financial statement. It typically has multiple columns:

- Account Name

- Unadjusted Trial Balance (Debit & Credit) - This section mirrors the initial trial balance.

- Adjustments (Debit & Credit) - This section reflects the adjusting entries made.

- Adjusted Trial Balance (Debit & Credit) - This is the sum of the Unadjusted Trial Balance and Adjustments columns for each account.

- Income Statement (Debit & Credit) - This section pulls adjusted revenues and expenses to determine net income or net loss.

- Balance Sheet (Debit & Credit) - This section pulls adjusted assets, liabilities, and equity accounts.

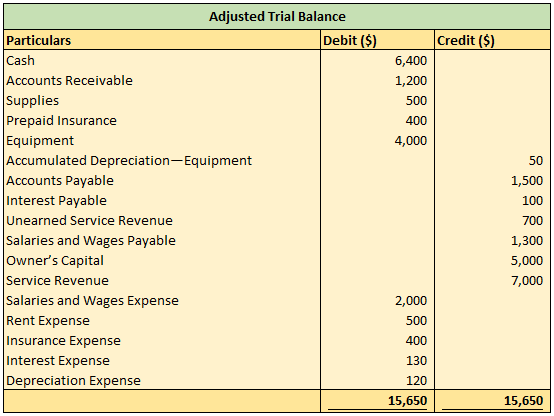

- List Account Names and Balances: List all the general ledger account names in the 'Account Name' column. Then, transfer the adjusted debit or credit balance of each account from the general ledger to the appropriate 'Adjusted Trial Balance' debit or credit column on the worksheet.

- Total the Debit and Credit Columns: Add up all the debit balances and all the credit balances in the Adjusted Trial Balance columns.

- Verify Equality: The total debits must equal the total credits in the Adjusted Trial Balance columns. If they do not match, there is an error that must be located and corrected before proceeding to the financial statement preparation. Double-check the posting of adjusting entries and the transfer of balances to the worksheet.

Example of Adjusting Entries and Their Impact

Consider a company that has earned $5,000 in services revenue but has not yet billed the client. The adjusting entry would be:

Debit: Accounts Receivable $5,000

Credit: Service Revenue $5,000

This entry recognizes the revenue earned even though cash has not been received. The Accounts Receivable balance on the balance sheet is increased, and the Service Revenue on the income statement is also increased.

Another common example is depreciation. Suppose a company has equipment that cost $10,000 and has an estimated useful life of 5 years. Using the straight-line method, the annual depreciation expense is $2,000. The adjusting entry would be:

Debit: Depreciation Expense $2,000

Credit: Accumulated Depreciation $2,000

This entry recognizes the depreciation expense for the year and increases the accumulated depreciation account, which is a contra-asset account that reduces the book value of the equipment.

Importance of Accuracy

The accuracy of the adjusted trial balance is paramount because it serves as the foundation for preparing reliable financial statements. Any errors in the adjusted trial balance will propagate through the financial statements, leading to misstatements of assets, liabilities, equity, revenues, and expenses. This, in turn, can negatively impact decision-making by management, investors, and other stakeholders.

Potential Errors and How to Prevent Them

Common errors that can occur during the preparation of the adjusted trial balance include:

- Mathematical Errors: Incorrect addition or subtraction when calculating adjusted balances. Double-check all calculations.

- Posting Errors: Incorrectly posting adjusting entries to the ledger accounts or omitting them entirely. Review the postings carefully.

- Transposition Errors: Reversing the digits when transferring balances (e.g., writing $123 as $132). Pay close attention to detail.

- Omission Errors: Failing to include an account or an adjusting entry on the trial balance. Ensure all relevant information is included.

To minimize these errors, it is essential to implement internal controls, such as:

- Regular Account Reconciliations: Reconcile bank accounts, accounts receivable, and other key accounts on a regular basis.

- Independent Review: Have another accountant or qualified professional review the adjusted trial balance and supporting documentation.

- Use of Accounting Software: Utilize accounting software that automates many of the calculations and posting processes, reducing the risk of human error.

Benefits of Preparing an Adjusted Trial Balance

Besides ensuring the accuracy of financial statements, preparing an adjusted trial balance offers several other benefits:

- Improved Financial Reporting: It leads to more accurate and reliable financial statements that comply with generally accepted accounting principles (GAAP).

- Enhanced Decision-Making: It provides management with better information for making informed business decisions.

- Facilitates Audits: It simplifies the audit process by providing auditors with a well-organized and accurate summary of account balances.

- Internal Control: The process helps to identify weaknesses in internal controls and provides an opportunity to improve them.

Conclusion

The adjusted trial balance is a fundamental step in the accounting cycle, bridging the gap between the initial trial balance and the creation of financial statements. Its preparation ensures the accuracy and reliability of financial data by incorporating necessary adjustments, ultimately leading to sound financial reporting and informed decision-making. It is a critical component of the accounting process that cannot be overlooked.

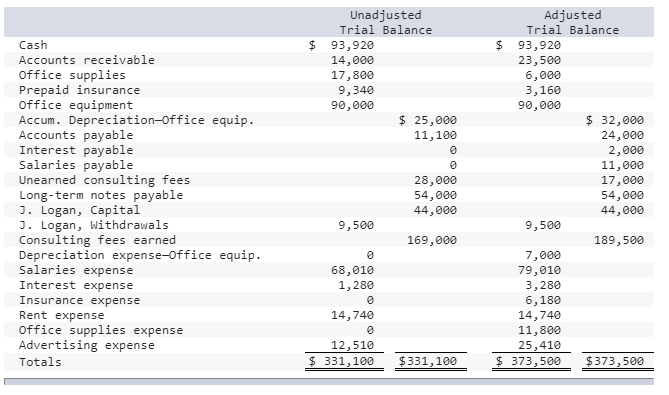

![[SOLVED] The adjusted trial balance for Frinzi Company | Course Eagle](http://courseeagle.com/images/the-adjusted-trial-balance-for-frinzi-company-is-given-in-e3-81119-1.jpg)