Secured Title Loans For Bad Credit

Hey there, friend! Ever heard of a secured title loan? It sounds kinda… intense, right? Like something straight out of a heist movie. But trust me, it's way more mundane (and legal!). Especially when we throw "bad credit" into the mix. Let's dive into this quirky corner of the financial world, shall we?

Bad Credit? No Problem (Maybe?)

Okay, so you've got less-than-stellar credit. We've all been there. Maybe you missed a bill, or three. Perhaps you accidentally bought a llama farm on a credit card (hey, no judgment!). Whatever the reason, your credit score is singing the blues. That doesn't mean you're doomed to a life of ramen and regret! This is where title loans can, potentially, come into play.

What's the Deal with Title Loans?

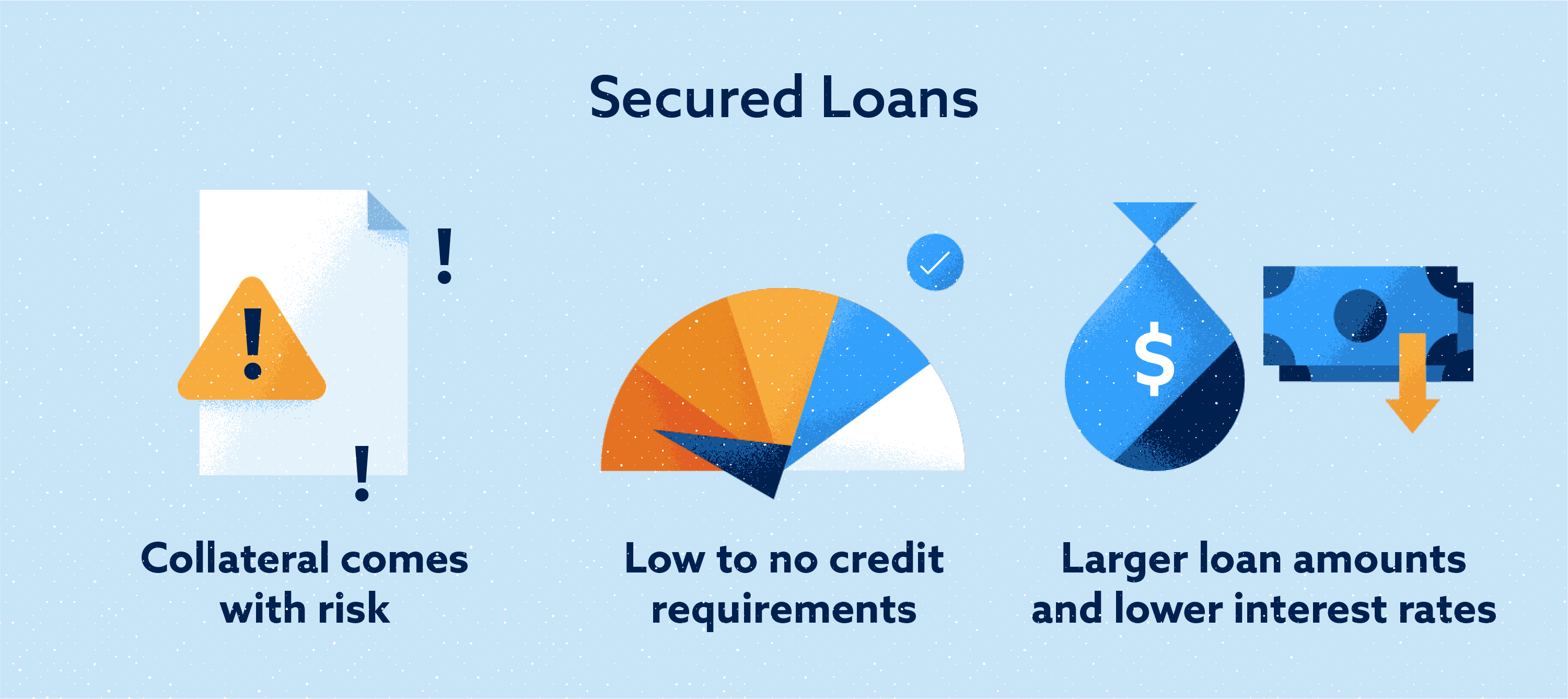

Think of it like this: you're offering up your car as a temporary hostage. Okay, not really a hostage. It's called collateral. You're borrowing money, and your car title is the guarantee that you'll pay it back. If you don't, the lender gets to repossess your sweet ride. Ouch!

Must Read

Here's the fun part: Because you're offering something of value (your car), lenders are often more willing to overlook a shaky credit history. They figure, "Hey, if they don't pay, at least we get a car!" Ruthless? Maybe. Effective? Sometimes.

Now, don't get me wrong. This isn't a magic wand that makes bad credit disappear. It's more like a financial Hail Mary. But it can be an option when other doors are slammed shut.

The Good, the Bad, and the Slightly Ridiculous

Let's break down the pros and cons of secured title loans for bad credit. Think of it as a reality check with a side of financial humor.

The Perks (Yes, There Are Some!)

- Faster Approval: Unlike traditional loans that require mountains of paperwork and weeks of waiting, title loans can often be approved in a matter of hours. Need cash in a hurry? This could be a lifesaver.

- Bad Credit? Who Cares (Kind Of): As we discussed, your credit score isn't the be-all and end-all. Lenders are more focused on the value of your car.

- Keep Driving: You usually get to keep driving your car while you're paying off the loan. It's not like they're going to stick it in a garage somewhere. Unless… (just kidding! Mostly).

The Downside (Brace Yourself)

- Insane Interest Rates: This is the big one. Title loans often come with eye-watering interest rates. We're talking percentages that could make your head spin. Seriously, do the math before you sign anything!

- Risk of Repossession: Miss a payment, and your car could be towed away. Imagine explaining that to your boss. "Yeah, sorry I'm late. My car got kidnapped by a loan company."

- Cycle of Debt: High interest rates can make it difficult to repay the loan, leading to a cycle of debt. You might end up borrowing more money to pay off the original loan. It's a financial black hole!

The Ridiculous (Because Why Not?)

Did you know that some people have tried to use boats, RVs, and even airplanes as collateral for title loans? I'm not sure how you'd repossess an airplane, but I'd pay to see it. Also, imagine explaining to your spouse that you just took out a loan using the family yacht as collateral. That's a conversation I wouldn't want to be a part of!

Before You Take the Plunge

Okay, so you're still considering a secured title loan for bad credit? Here's some friendly advice (because that's what friends do!).

Do Your Homework

Shop around: Don't just go with the first lender you find. Compare interest rates, fees, and repayment terms. Look for the least terrible option (because let's be honest, none of them are exactly amazing). Look up reviews and complaints about different lenders. Knowledge is power!

Read the fine print: This is crucial! Understand every single detail of the loan agreement. What are the penalties for late payments? What happens if you can't repay the loan? Don't be afraid to ask questions. If something seems fishy, walk away.

Explore Alternatives

Before you commit to a title loan, consider other options. Can you borrow money from friends or family? Can you sell some unwanted stuff? Can you get a personal loan from a credit union? Are there any government assistance programs that could help? Explore every avenue before you risk losing your car.

Budget, Budget, Budget!

If you do decide to take out a title loan, create a realistic budget. Figure out exactly how you're going to repay the loan, including interest and fees. Stick to your budget like glue! Don't let those high interest rates suck you dry.

The Bottom Line

Secured title loans for bad credit can be a temporary solution for urgent financial needs. But they're also incredibly risky. High interest rates and the threat of repossession make them a last resort, not a first choice. Think carefully, do your research, and explore all other options before you take the plunge.

And hey, maybe start saving up for that llama farm before you put it on your credit card next time. Just a thought!

Remember, I'm not a financial advisor. This is just a friendly chat about a quirky topic. Always consult with a qualified professional before making any major financial decisions. Stay safe, and keep your car keys handy!