Revolving Line Of Credit For Bad Credit

Hey there, friend! Ever felt like your credit score is holding you back? Like it's this grumpy gatekeeper saying, "Nope, not today!" to all your financial aspirations? We've all been there. But what if I told you there's a potential lifeline out there, a financial tool that could offer a helping hand even with a less-than-stellar credit history? We're talking about revolving lines of credit for bad credit, and trust me, they're way more interesting than they sound.

What's the Deal with Revolving Lines of Credit?

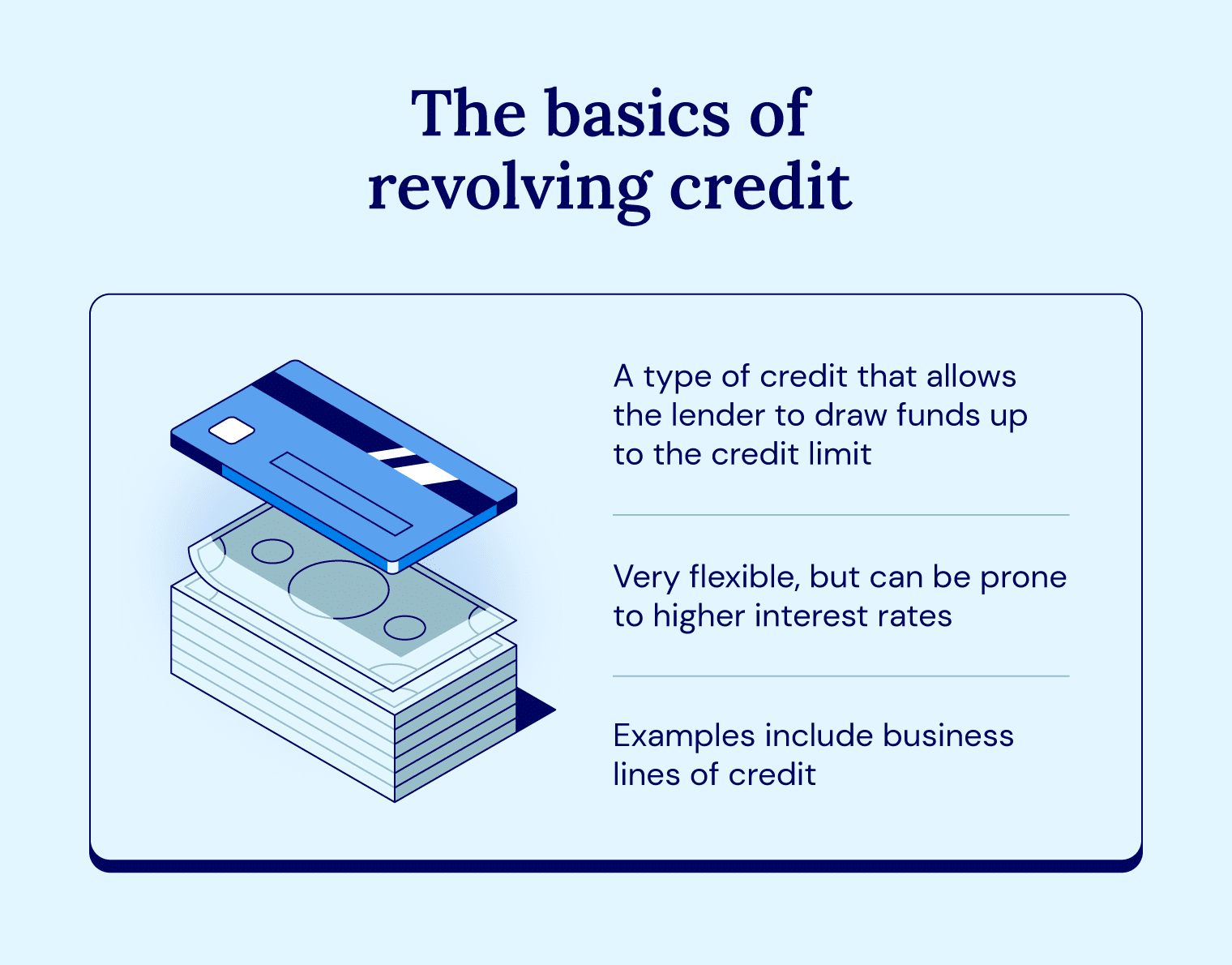

Okay, let's break it down. Imagine a credit card, but with a slightly different twist. Instead of a one-time loan, a revolving line of credit gives you access to a pool of money that you can borrow from, repay, and borrow from again – like a never-ending piggy bank! Sounds pretty cool, right?

Think of it like this: Your budget is a garden. Sometimes it needs watering (unexpected expenses!), sometimes it flourishes (extra income!). A revolving line of credit is like having a little sprinkler system you can turn on when things get dry. You use what you need, and when the rains come (you get paid!), you refill the reservoir. Simple as that!

Must Read

But here's the catch: because we're talking about options for people with bad credit, the terms might be a little different than what you'd get with a perfect credit score. Think potentially higher interest rates and lower credit limits. But don't let that scare you away just yet! Let's dive deeper.

Why Bother When My Credit's Not Great?

So, you might be thinking, "If my credit's already bad, why would I even consider this?" Good question! Here's the thing: a revolving line of credit, even with potentially higher rates, can be a valuable tool for a few key reasons:

- Emergency Fund Alternative: Unexpected car repair? Medical bill surprise? A revolving line of credit can act as a safety net when you don't have a fully stocked emergency fund. It's better than resorting to payday loans with sky-high interest rates.

- Credit Building Opportunity: Here's where it gets interesting. If you use the line of credit responsibly – meaning, you only borrow what you can afford to repay and you make on-time payments – you can actually start to rebuild your credit score! Each on-time payment is like a gold star on your credit report.

- Flexibility is Key: Unlike a traditional loan with fixed payments, a revolving line of credit offers more flexibility. You can borrow different amounts each month, as long as you stay within your credit limit. It’s like having a financial Swiss Army knife!

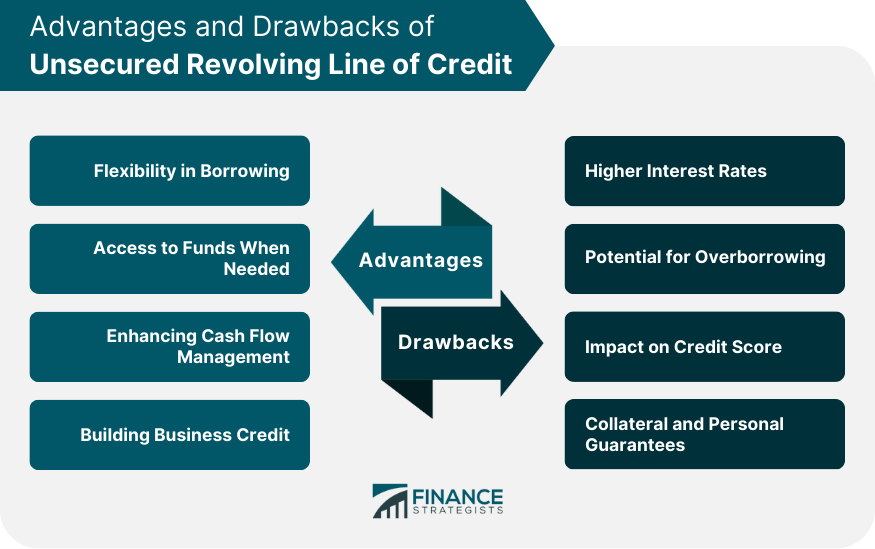

Things to Watch Out For (The Not-So-Fun Part)

Okay, let's be real. It's not all sunshine and rainbows. There are definitely things to keep in mind when considering a revolving line of credit for bad credit:

Interest Rates: The Elephant in the Room

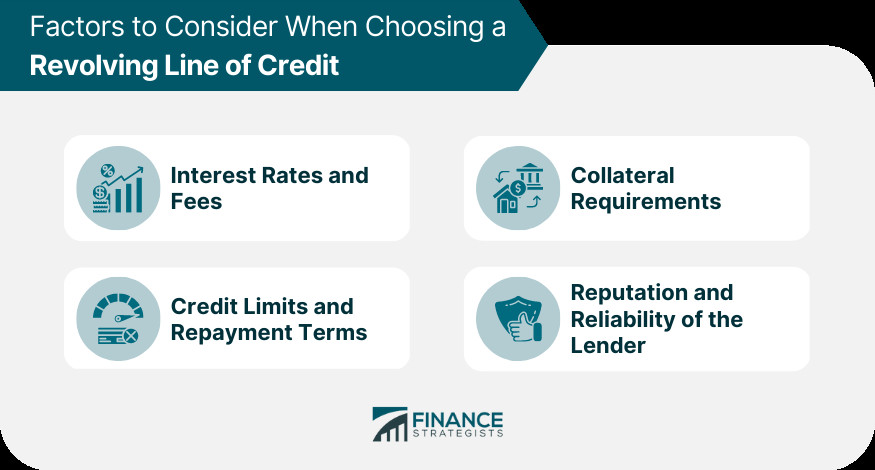

Let's face it: interest rates for bad credit options are usually higher. That's just the reality. So, before you jump in, make sure you understand the interest rate and how it's calculated. Compare offers from different lenders. Think of it like shopping for the best price on groceries - you wouldn't just grab the first item you see, right?

Fees, Fees, Everywhere!

Read the fine print! Some lenders charge annual fees, late payment fees, or even cash advance fees. These fees can add up quickly, so make sure you're aware of them and factor them into your decision. It's like knowing the hidden costs of that "amazing" all-inclusive vacation – are those "free" drinks really free?

The Temptation Trap

This is a big one. It's easy to get carried away and borrow more than you can afford to repay. Remember, a revolving line of credit is a tool, not a free pass to overspend. Discipline is key. Set a budget and stick to it!

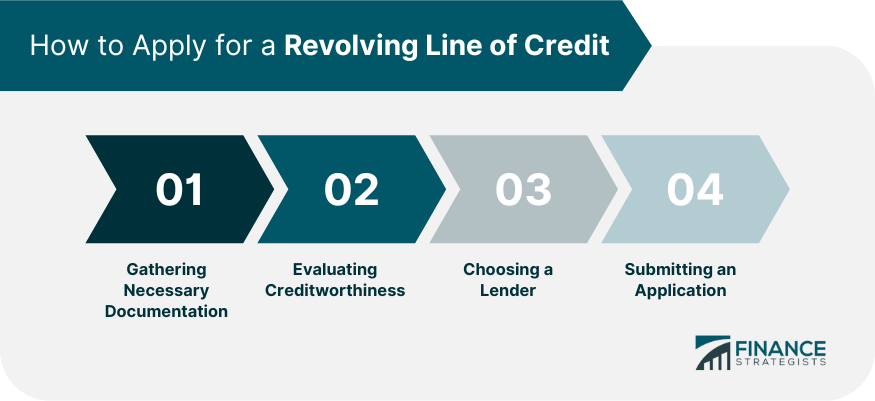

Finding the Right Revolving Line of Credit: Where Do I Start?

So, you're intrigued, but where do you even begin? Here are a few places to look:

:max_bytes(150000):strip_icc()/what-are-differences-between-revolving-credit-and-line-credit.asp-v1-3d86938b361d4a748bddb1f06ea74f3d.png)

- Credit Unions: Credit unions often offer more favorable terms than traditional banks, especially for people with less-than-perfect credit. They're like the friendly neighborhood bakery compared to the big chain store.

- Online Lenders: There are tons of online lenders specializing in bad credit loans. Do your research and compare offers carefully.

- Secured Lines of Credit: These require you to put up collateral, like a savings account. While it might seem risky, it can be a good option if you're having trouble getting approved for an unsecured line of credit. It's like putting down a deposit to show you're serious.

Always check the lender's reputation before applying. Read reviews and make sure they're legitimate. The Better Business Bureau (BBB) can be a helpful resource.

Is It Right for You? The Million-Dollar Question

Ultimately, whether a revolving line of credit for bad credit is right for you depends on your individual circumstances. Ask yourself these questions:

- Can I afford the monthly payments? (Be honest with yourself!)

- Will I use it responsibly? (No impulse shopping sprees!)

- Do I understand the terms and conditions? (Read the fine print!)

- Are there any other options available to me? (Explore all your possibilities!)

If you answered "yes" to these questions and you're confident you can manage the credit line responsibly, then it might be worth considering. But remember, it's not a magic bullet. It's a tool that, when used wisely, can help you manage your finances and even improve your credit score. But it needs careful management and understanding.

So, there you have it – a relaxed look at revolving lines of credit for bad credit. It's not a cure-all, but it can be a valuable tool for the right person. Just remember to do your research, understand the risks, and use it responsibly. Good luck!

Disclaimer: I am an AI chatbot and cannot provide financial advice. Please consult with a qualified financial advisor before making any financial decisions.