Obtaining a personal loan with a credit score around 500 presents significant challenges. A credit score in this range is generally considered "poor" and signifies a higher risk for lenders. This article outlines the options potentially available to borrowers with such a score, the associated conditions, and essential considerations for responsible borrowing.

Understanding the Landscape

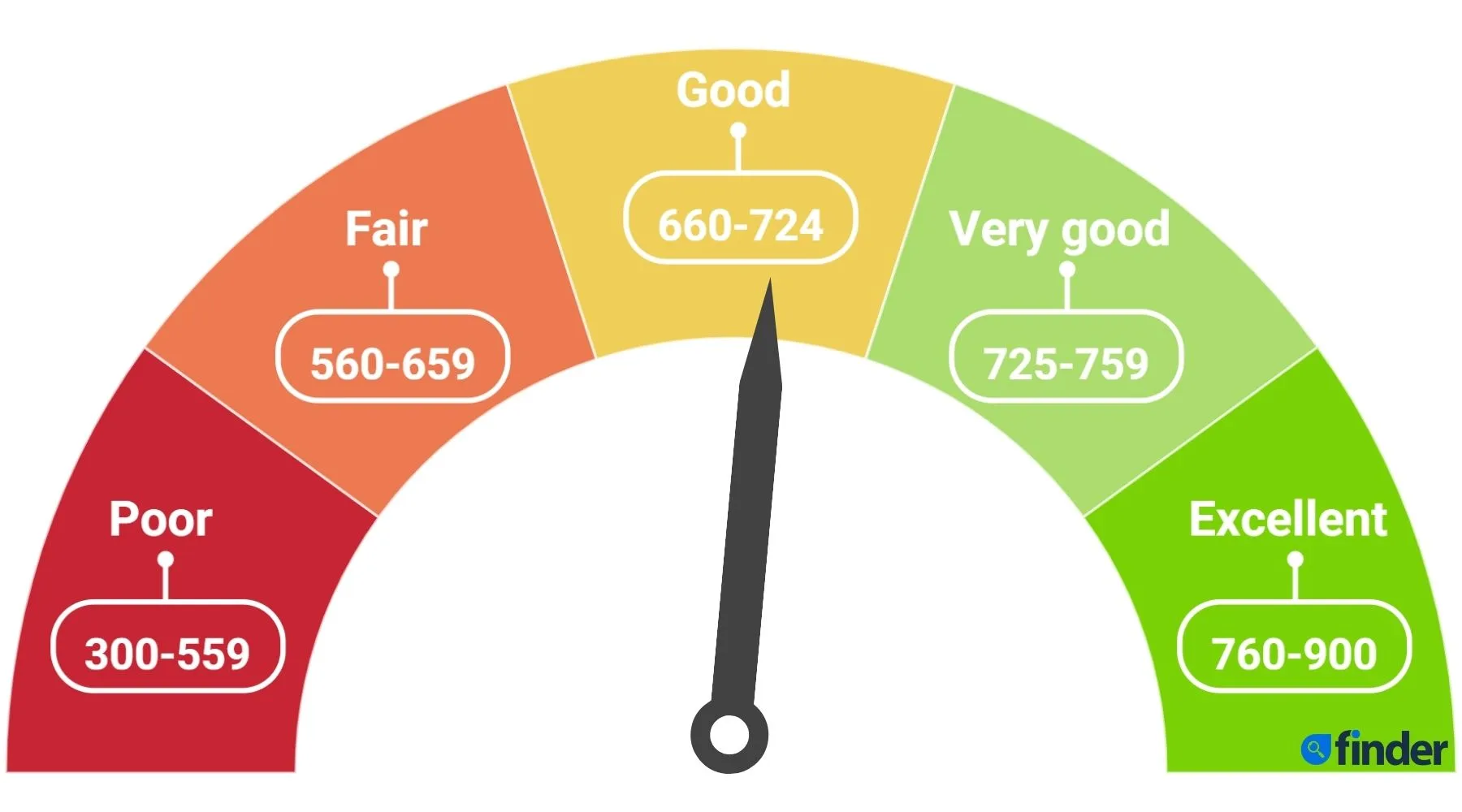

Credit scores are a numerical representation of an individual's creditworthiness, based on their credit history. FICO scores, the most widely used, range from 300 to 850. A score of 500 falls within the "poor" range, indicating a history of missed payments, high credit utilization, or other negative credit events. Lenders use these scores to assess the likelihood of repayment.

Borrowers with a 500 credit score will likely face:

Higher interest rates: Lenders compensate for the increased risk by charging significantly higher interest rates.

Stricter loan terms: Expect shorter repayment periods and potentially lower loan amounts.

Increased scrutiny: Lenders will thoroughly examine income, employment history, and other financial factors.

Limited options: Fewer lenders are willing to offer personal loans to borrowers with poor credit.

Potential Loan Options

While challenging, obtaining a personal loan with a 500 credit score is not impossible. Several options may be available, each with its own set of considerations:

Secured Personal Loans

Secured loans require the borrower to pledge an asset as collateral, such as a vehicle, savings account, or other valuable property. The collateral reduces the lender's risk, making them more willing to approve loans to borrowers with poor credit. If the borrower defaults on the loan, the lender can seize the collateral to recover their losses.

Considerations:

The value of the collateral must be sufficient to cover the loan amount. Failure to repay the loan can result in the loss of the pledged asset. Ensure the asset is properly insured and maintained.

How to Get a Personal Loan With a 500 Credit Score

Co-signed Loans

A co-signed loan involves another individual with good credit agreeing to be responsible for the loan if the borrower defaults. The co-signer's credit history provides the lender with added assurance, increasing the likelihood of approval. This option depends heavily on finding a willing and qualified co-signer.

Considerations:

The co-signer is legally obligated to repay the loan if the borrower fails to do so. This can negatively impact the co-signer's credit score and financial standing. Open communication and a clear understanding of the risks are essential.

Payday Loans and Title Loans

Payday loans are short-term, high-interest loans typically due on the borrower's next payday. Title loans are similar but use the borrower's vehicle as collateral. These loans are generally marketed to individuals with poor credit and are easily accessible.

Boost Your Credit Score with a Personal Loan

Considerations:

Payday and title loans carry extremely high interest rates and fees, often leading to a cycle of debt. They should be considered a last resort due to their predatory nature. Carefully evaluate the terms and ensure the loan can be repaid on time.

Credit Union Loans

Credit unions are member-owned financial institutions that may offer more favorable loan terms to their members than traditional banks. Some credit unions have programs specifically designed for borrowers with poor credit, focusing on financial education and credit building.

Considerations:

Membership in a credit union is usually required. Credit unions may have stricter eligibility requirements and may require a longer relationship with the institution before offering a loan. Research different credit unions and compare their offerings.

Debt Consolidation 500 Credit Score at Hillary Mccarty blog

Online Lenders

Several online lenders specialize in providing loans to borrowers with less-than-perfect credit. These lenders often have less stringent requirements than traditional banks and may be more willing to approve loans to individuals with a 500 credit score.

Considerations:

Online lenders may charge higher interest rates and fees. Carefully research the lender's reputation and read reviews before applying. Ensure the lender is legitimate and complies with all applicable regulations.

Factors Influencing Loan Approval

Beyond credit score, lenders consider several factors when evaluating loan applications, including:

Is It Possible To Get a Personal Loan With a 500 Credit Score

Income: A stable and verifiable income stream is crucial. Lenders want assurance that the borrower can afford to repay the loan.

Employment History: A consistent employment history demonstrates financial stability and reliability.

Debt-to-Income Ratio (DTI): Lenders assess the borrower's existing debt obligations relative to their income. A high DTI may indicate difficulty in managing additional debt.

Collateral (if applicable): The value and condition of any pledged collateral are important considerations for secured loans.

Strategies for Improving Approval Odds

Borrowers with a 500 credit score can take steps to improve their chances of loan approval:

Improve Credit Score: Even small improvements in credit score can increase approval odds. Focus on paying bills on time, reducing credit card balances, and disputing any errors on credit reports.

Increase Income: Explore opportunities to increase income, such as taking on a part-time job or freelancing.

Reduce Debt: Pay down existing debt to lower the DTI.

Provide a Down Payment: Offering a down payment on a secured loan can reduce the lender's risk.

Apply with a Co-signer: Enlisting a creditworthy co-signer can significantly improve approval chances.

The Importance of Responsible Borrowing

Obtaining a personal loan with a 500 credit score should be approached with caution. It's crucial to borrow only what is needed and to develop a realistic repayment plan. Failing to repay the loan can further damage credit and lead to significant financial hardship.

Before taking out a loan, carefully consider the following:

Interest Rates and Fees: Understand the total cost of the loan, including interest rates, origination fees, and other charges.

Repayment Terms: Ensure the repayment schedule is manageable and fits within your budget.

Alternatives: Explore alternative options, such as borrowing from family or friends, or seeking assistance from non-profit organizations.

Budgeting: Create a detailed budget to track income and expenses, and ensure you can comfortably afford the loan payments.

Key Takeaways

Securing a personal loan with a 500 credit score is a challenging but potentially achievable goal. Borrowers should focus on:

Exploring secured loans, co-signed loans, credit union loans, and online lenders.

Improving their credit score and overall financial situation.

Carefully evaluating the terms and conditions of any loan offer.

Practicing responsible borrowing habits to avoid further financial difficulties.

Ultimately, improving your credit score should be a primary focus, as this will open up more favorable loan options and reduce the overall cost of borrowing in the long run.