Personal Loans Similar To Bmg Money

Okay, so you're looking for personal loans similar to BMG Money, huh? Life throws curveballs, doesn't it? Unexpected bills, car repairs that seem to multiply like rabbits, maybe even a chance to finally take that dream vacation (you deserve it!). Whatever the reason, needing a loan is totally normal. Let's dive into some options, shall we? Think of me as your financial coffee buddy, here to help you navigate this loan landscape.

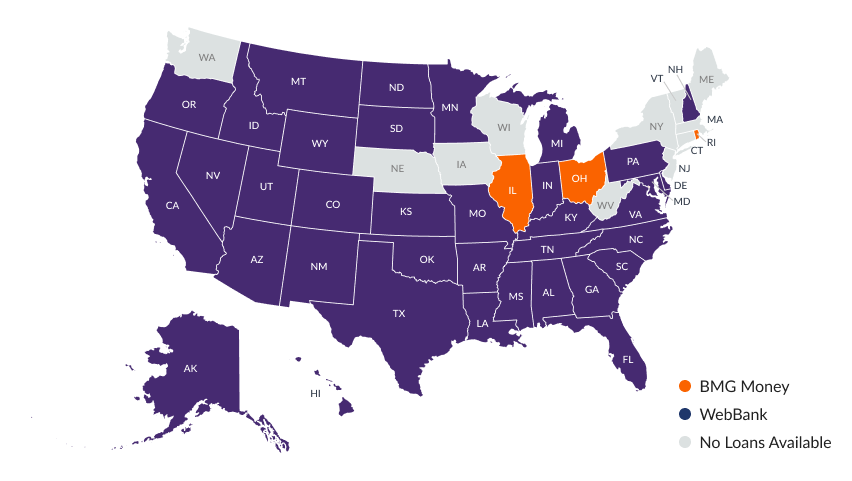

First things first, BMG Money specializes in loans for government employees. So, if you're in the public sector, awesome! If not, don't worry – there are plenty of fish in the sea...or, you know, lenders in the financial world. Let's explore some of those "fish," shall we?

Options to Explore: Beyond BMG Money

Online Lenders: The Speedy Gonzales of Loans

Online lenders are often the first place people look these days. Why? Because they're fast and often have less stringent requirements than traditional banks. Think of them as the online shopping of the loan world – convenient and available 24/7. But, always read the fine print! Seriously, it's like deciphering ancient hieroglyphs, but crucial. Do your homework, my friend.

Must Read

Companies like LightStream (known for great rates, especially if you have excellent credit) and Upstart (which considers factors beyond just your credit score – like education and employment history) are worth checking out. Upstart might be a good fit if your credit isn't perfect but you have a solid employment track record. Just remember to compare those interest rates! Even a small difference can add up to big bucks over the life of the loan. We don't want you paying more than you absolutely have to, right?

Then there's SoFi, which started with student loan refinancing but now offers personal loans too. They're known for member perks and career counseling, which is a nice bonus. Free advice? Yes, please!

Credit Unions: The Friendly Neighborhood Lender

Don't underestimate your local credit union! They're often more flexible than big banks and may offer better rates and more personalized service. Think of them as the mom-and-pop shops of the financial world. Because they're member-owned, they tend to prioritize their members' needs. They might even know your name! (Okay, maybe not, but they're generally more personable). Worth investigating? Definitely!

![9 Top Loans like BMG Money & Alternatives [2024] - ViralTalky](https://viraltalky.com/wp-content/uploads/2023/06/Loans-like-BMG-Money.jpg)

Plus, credit unions often have lower fees (hallelujah!). It's like finding a twenty-dollar bill in your old jeans – a welcome surprise! To join a credit union, you typically need to meet certain eligibility requirements, like living or working in a specific area, or being employed by a particular company. But it's usually pretty easy to qualify. Just do a quick search for credit unions in your area.

Banks: The Traditional Route (But Still Worth Considering!)

Okay, okay, banks might seem a little "old school," but they're still a viable option. Especially if you already have a good relationship with a bank (e.g., you've been a long-time customer), you might be able to snag a competitive rate on a personal loan. It never hurts to ask, right? The worst they can say is no. Plus, having an existing relationship might make the application process smoother.

Big banks like Chase, Wells Fargo, and Citibank all offer personal loans, but their rates and terms can vary widely. Don't just assume your current bank is offering you the best deal! Shop around and compare rates from other lenders too. It's like comparison shopping for a new TV – you want to get the best bang for your buck!

![9 Top Loans like BMG Money & Alternatives [2023] - ViralTalky](https://viraltalky.com/wp-content/uploads/2023/06/SoFi-Loan-1024x536.jpg.webp)

Peer-to-Peer Lending: Borrowing from the Crowd

Peer-to-peer (P2P) lending platforms connect borrowers with individual investors. Think of it as crowdfunding, but for loans. Companies like LendingClub and Prosper are popular players in this space. P2P lending can sometimes offer lower rates than traditional lenders, especially if you have good credit. But it can also be riskier for investors, so interest rates can be higher for borrowers with less-than-perfect credit.

It's definitely worth looking into, but make sure you understand the fees involved and the terms of the loan. And be aware that funding can sometimes take a little longer than with other types of lenders, as the platform needs to match you with investors. Patience is a virtue, as they say!

Factors to Consider Before Applying (aka: The Nitty-Gritty)

Credit Score: Your Financial Report Card

Your credit score is a major factor in determining whether you'll be approved for a personal loan and what interest rate you'll receive. A higher credit score generally means a lower interest rate. Makes sense, right? Lenders see you as less of a risk. If you have a low credit score, you might still be able to get a loan, but you'll likely pay a higher interest rate. It's like paying a premium for being a "risky driver" in the eyes of the insurance company.

Before you start applying for loans, check your credit score! You can get a free credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) once a year. Knowing your score will give you a better idea of what kind of rates you can expect. It's like checking the weather forecast before you plan a picnic – you want to be prepared!

Interest Rates: The Price You Pay to Borrow

Pay close attention to the interest rate! This is the cost of borrowing money. Interest rates can be fixed (meaning they stay the same throughout the life of the loan) or variable (meaning they can fluctuate). Fixed rates provide more predictability, while variable rates can be lower initially but could increase over time. It's like choosing between a steady paycheck and a commission-based job – each has its pros and cons.

Also, be aware of the difference between APR (annual percentage rate) and the interest rate. The APR includes the interest rate plus any fees associated with the loan, so it's a more accurate reflection of the true cost of borrowing. Think of it as the "sticker price" of the loan, including all the taxes and fees.

Loan Terms: How Long You Have to Repay

The loan term is the length of time you have to repay the loan. Shorter loan terms typically mean higher monthly payments but lower overall interest costs. Longer loan terms mean lower monthly payments but higher overall interest costs. It's a balancing act! You need to find a loan term that fits your budget and your financial goals.

![9 Top Loans like BMG Money & Alternatives [2024] - ViralTalky](https://viraltalky.com/wp-content/uploads/2023/06/Upstart-Personal-Loans-2.jpg)

Consider how much you can realistically afford to pay each month. Don't overextend yourself! It's better to choose a slightly longer loan term with lower monthly payments than to struggle to make payments on a shorter loan term. You don't want to be "house poor," or in this case, "loan poor!"

Fees: The Hidden Costs

Be aware of any fees associated with the loan. Some lenders charge origination fees (a percentage of the loan amount), prepayment penalties (a fee for paying off the loan early), or late payment fees. Read the fine print carefully to understand all the fees involved. You don't want any surprises! It's like finding out your cheap flight has a baggage fee that costs more than the ticket itself.

A Few Extra Tips (Because Why Not?)

- Shop around! Get quotes from multiple lenders before making a decision.

- Read the fine print! Seriously, every single word.

- Don't borrow more than you need! It's tempting, but resist!

- Make sure you can afford the monthly payments! Create a budget to see how the loan payments will fit into your finances.

- Consider a secured loan if you're having trouble getting approved! A secured loan is backed by collateral, such as a car or a house, which can make it easier to get approved, especially if you have bad credit. But be careful! If you can't repay the loan, you could lose your collateral.

The Bottom Line

Finding the right personal loan is like finding the perfect pair of jeans – it takes a little bit of effort, but it's worth it in the end! Don't be afraid to shop around, compare rates, and ask questions. And remember, you've got this! You're a financially savvy superhero in the making! Now go forth and conquer that loan landscape!

Disclaimer: I am an AI chatbot and cannot provide financial advice. Please consult with a qualified financial professional before making any financial decisions.

![9 Top Loans like BMG Money & Alternatives [2024] - ViralTalky](https://viraltalky.com/wp-content/uploads/2023/06/Lendly.jpg)

![9 Top Loans like BMG Money & Alternatives [2023] - ViralTalky](https://viraltalky.com/wp-content/uploads/2023/06/MoneyLion-Credit-Builder-2-1024x536.jpg)

![9 Top Loans like BMG Money & Alternatives [2023] - ViralTalky](https://viraltalky.com/wp-content/uploads/2023/06/JP-Morgan-Chase-1024x536.jpg)