Personal Loan With Car As Collateral

Remember that time your washing machine decided to stage its own personal apocalypse, spewing soapy water all over your laundry room? Yeah, good times. Mine did that last month. The repairman quoted me a price that made me question my life choices. Suddenly, that "responsible adult" thing felt very, very heavy. In moments like that, you start thinking, "Okay, universe, is this a test? And more importantly, how do I pass it without selling a kidney?"

Turns out, there are other options besides organ donation. Sometimes, you need a quick injection of cash. Maybe it's for an emergency repair, unexpected medical bills (because let's face it, life throws curveballs), or even to consolidate some high-interest debt that's been lurking in the shadows. That's where personal loans come in.

But what if your credit score is... less than stellar? Or maybe you just want a lower interest rate? That's where the idea of using your car as collateral comes into play. Let's dive into the world of personal loans with your car as collateral, shall we?

Must Read

What Exactly is a Personal Loan with Car as Collateral?

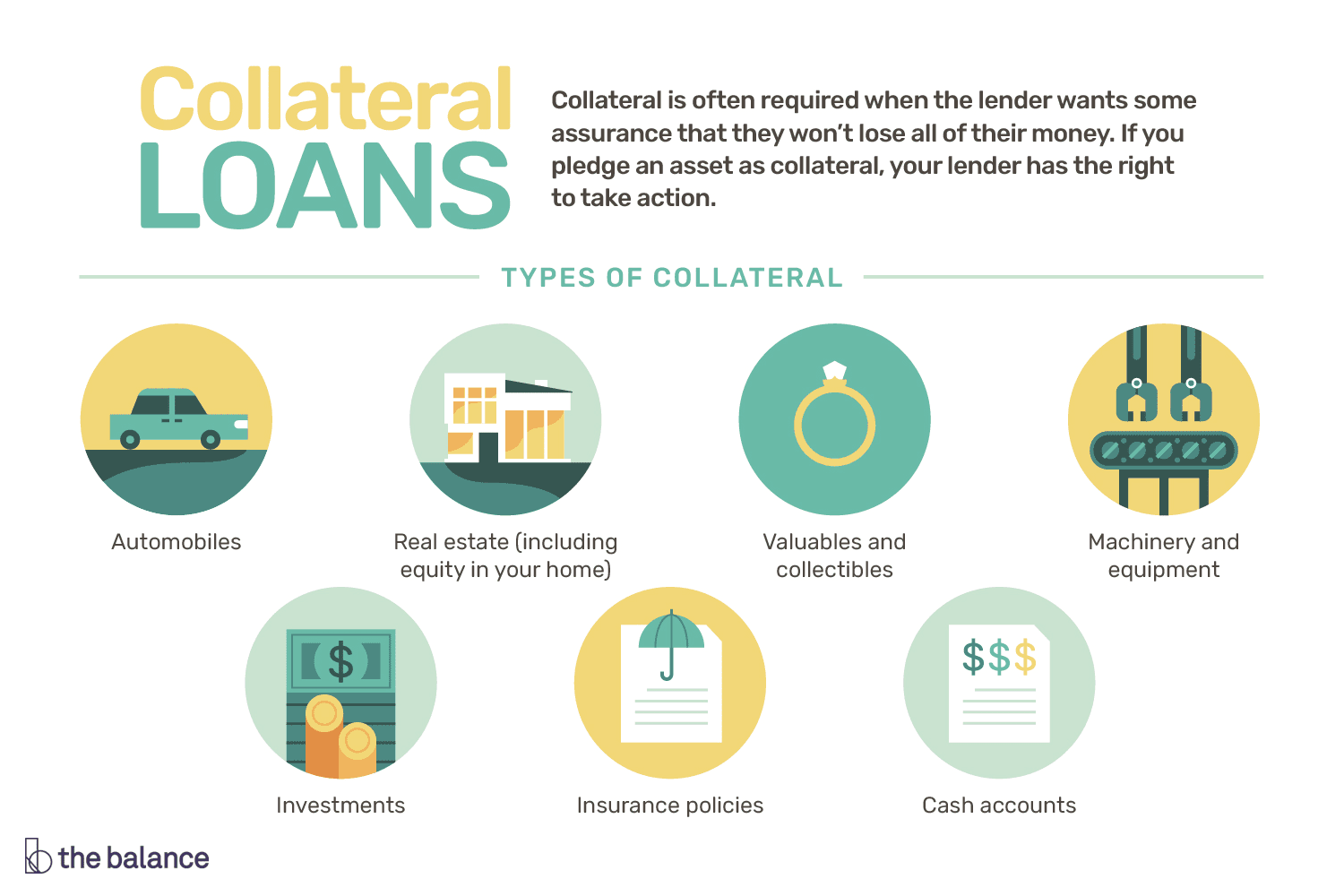

Okay, let's break this down. A personal loan is simply a loan you get from a bank, credit union, or online lender that you can use for pretty much anything. No one's breathing down your neck asking what you're spending it on (unless they're really nosy). A secured loan, on the other hand, requires you to put up something valuable as collateral. If you don't repay the loan, the lender can seize that asset to recoup their losses. Think of it as a safety net for the lender. They get some reassurance they'll get their money back.

A personal loan with your car as collateral is a secured loan where your car acts as that safety net. Basically, you're telling the lender, "Hey, I promise I'll pay you back. If I don't, you can have my ride." (Hopefully, it doesn't come to that!)

How Does it Work? A Step-by-Step Breakdown

The process usually goes something like this:

- Application: You fill out an application with the lender, providing information about your income, employment, and the vehicle you're using as collateral.

- Vehicle Appraisal: The lender will need to assess the value of your car. They'll likely have it appraised to determine its market value. Keep in mind, they want to make sure it's worth enough to cover the loan amount if you default.

- Loan Approval: If approved, the lender will offer you a loan with specific terms, including the interest rate, repayment schedule, and any fees.

- Loan Disbursement: Once you agree to the terms and sign the loan agreement, the lender will disburse the funds to you.

- Repayment: You make regular payments according to the loan agreement until the loan is paid off. And hopefully, you keep your car through the whole process!

The Pros and Cons: Weighing Your Options

Like everything in life, there are advantages and disadvantages to using your car as collateral. Let's take a look:

The Upsides: Why You Might Consider It

- Potentially Lower Interest Rates: Because the loan is secured, lenders often offer lower interest rates compared to unsecured personal loans. This can save you a significant amount of money over the life of the loan.

- Easier Approval with Bad Credit: If you have a less-than-perfect credit history, using your car as collateral can increase your chances of getting approved for a loan. The lender is taking on less risk because they have an asset to fall back on.

- Larger Loan Amounts: You might be able to borrow a larger sum of money compared to an unsecured loan. The value of your car can support a higher loan amount.

The Downsides: What You Need to Watch Out For

- Risk of Losing Your Car: This is the biggest and most obvious drawback. If you fail to make your loan payments, the lender can repossess your car. Think long and hard about whether you can realistically afford the repayments.

- Fees and Charges: Be aware of potential fees, such as application fees, appraisal fees, and late payment fees. These can add up quickly and increase the overall cost of the loan. Read the fine print! I can't stress this enough.

- Potential for High Interest Rates (Still): While the interest rate might be lower than an unsecured loan, it can still be relatively high, especially if you have bad credit. Shop around and compare offers from different lenders.

- Depreciation: Cars lose value over time. If you need to sell your car to repay the loan, you might not get as much as you originally anticipated. This could leave you owing more than the car is worth.

Who is This Type of Loan For?

A personal loan with your car as collateral might be a good option for you if:

- You have a less-than-perfect credit history and are struggling to get approved for an unsecured loan.

- You need a larger loan amount than you can qualify for with an unsecured loan.

- You're confident in your ability to repay the loan on time. Be honest with yourself about your financial situation.

- You're comfortable with the risk of losing your car if you default on the loan.

However, it's probably not a good idea if:

- You're already struggling with debt and are worried about making repayments.

- You need your car for essential transportation, like getting to work or taking your kids to school, and can't afford to be without it.

- You can qualify for an unsecured loan with a reasonable interest rate.

- You have a high-risk job or an unstable source of income.

Alternatives to Consider

Before you jump into a loan with your car as collateral, explore other options:

- Unsecured Personal Loans: Even if your credit isn't perfect, you might still be able to qualify for an unsecured personal loan. Shop around and compare offers from different lenders.

- Credit Cards: If you need a small amount of money, a credit card might be a good option. Just be sure to pay it off quickly to avoid accumulating interest charges.

- Debt Consolidation Loans: If you have multiple debts, a debt consolidation loan can help you simplify your finances and potentially lower your interest rate.

- Credit Counseling: A credit counselor can help you develop a budget and manage your debt. They can also negotiate with your creditors on your behalf.

- Ask for Help: Sometimes, the best solution is simply to talk to friends or family. They might be willing to lend you money or offer other forms of assistance.

Tips for Choosing a Lender

If you decide that a personal loan with your car as collateral is the right choice for you, here are some tips for choosing a lender:

- Shop Around: Don't just go with the first lender you find. Get quotes from multiple lenders and compare their interest rates, fees, and loan terms.

- Check the Lender's Reputation: Read online reviews and check with the Better Business Bureau to see if the lender has a good reputation.

- Read the Fine Print: Before you sign any loan agreement, read it carefully and make sure you understand all the terms and conditions. Don't be afraid to ask questions!

- Be Wary of Predatory Lenders: Avoid lenders who charge excessively high interest rates or fees, or who use aggressive or deceptive tactics.

- Consider Local Credit Unions: They are more likely to offer better conditions to their members.

Important Considerations Before Taking the Plunge

Before you sign on the dotted line, ask yourself these questions:

- Can I Afford the Repayments? Create a budget and make sure you can comfortably afford the monthly payments. Don't just assume you'll be able to make it work.

- What Will Happen if I Lose My Job? Do you have a backup plan in case you lose your job or experience a financial hardship?

- Is This Loan Really Necessary? Are there other ways to solve your financial problem without taking out a loan?

- Am I Willing to Risk Losing My Car? Be honest with yourself about the risks involved. If you're not comfortable with the possibility of losing your car, this type of loan might not be for you.

The Final Verdict: Is it Right for You?

A personal loan with your car as collateral can be a helpful tool in certain situations, but it's not a decision to be taken lightly. Weigh the pros and cons carefully, explore all your options, and make sure you understand the risks involved. Remember, your car is a valuable asset, and you don't want to lose it because of a bad loan decision.

Think of it this way: borrowing money is like playing a game of chess. You need to think several steps ahead, anticipate potential problems, and make sure you have a solid plan in place. Otherwise, you might end up in checkmate (and without a car!).

And hey, if you're still not sure, talk to a financial advisor. They can provide personalized advice and help you make the best decision for your individual circumstances. After all, it's always better to be safe than sorry, especially when your car is on the line.

Now, if you'll excuse me, I need to go find a new washing machine... and maybe a financial advisor. Just kidding (sort of!).

:max_bytes(150000):strip_icc()/dotdash-070915-personal-loans-vs-car-loans-how-they-differ-v2-f8faff14abb1488d869f4026c406a86c.jpg)