Payday Loans Based On Income Not Credit

Okay, let's talk about something that might have crossed your mind at some point – money. Specifically, when you're in a pinch and need a little help to bridge the gap between paychecks. Ever heard of payday loans based on income, not credit? Sounds intriguing, right? Let's dive in and see what the fuss is all about. Think of it like this: Your credit score is like your report card from high school – important at the time, but does it really define you now? These loans look beyond that.

What's the Big Deal?

So, why are we even talking about this? Well, traditional loans usually put a huge emphasis on your credit history. It's like showing up to a party and having the bouncer immediately ask to see your LinkedIn profile. If your score isn't sparkling, you might get turned away. But what if you've been working hard, earning consistently, but just haven't had the chance to build up a stellar credit score yet? That's where income-based payday loans come in. They're more interested in your current income stream than your past financial history.

It's About Right Now, Not Yesterday

Imagine you're trying to buy a pizza. A traditional lender is like a pizza place that only accepts orders from people who have bought pizzas there before and always left a five-star review. An income-based lender? They're more like the new place down the street that just wants to know if you have enough money to pay for the pizza right now. Big difference, right?

Must Read

How Do These Loans Actually Work?

Alright, let’s break it down. How do these loans based on your income actually work? What's the secret sauce?

- Proof of Income is Key: The lender will want to see proof that you have a regular income. This could be pay stubs, bank statements showing direct deposits, or even a letter from your employer. It’s all about showing them you can repay the loan. Think of it like this: you're showing them the recipe for your financial stability.

- Loan Amount: The amount you can borrow will typically depend on your income. They'll want to make sure the repayments are manageable for you. It's not about lending you as much as possible, but lending you what you can realistically afford to pay back.

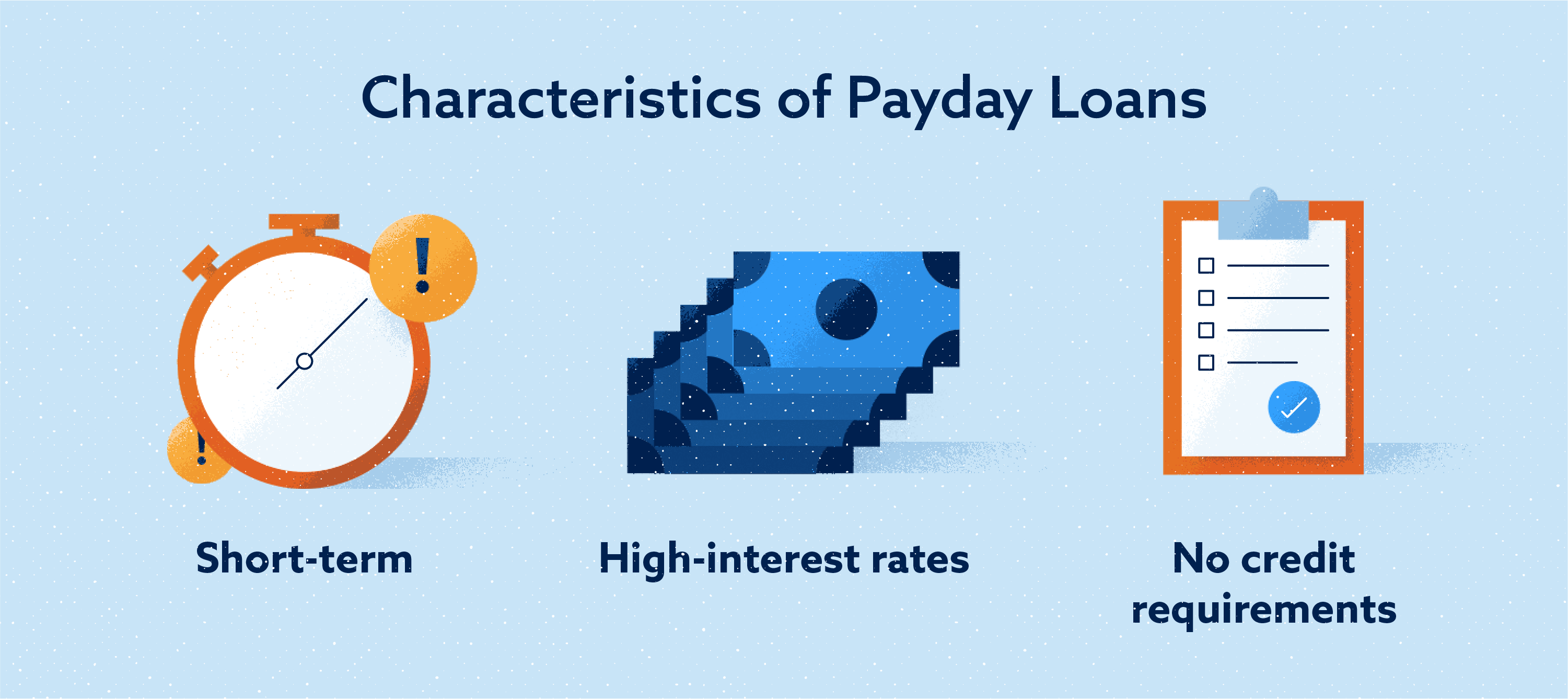

- Repayment Terms: These are usually short-term loans, meaning you'll need to pay them back relatively quickly – often by your next payday. Imagine borrowing sugar from a neighbor and promising to replace it as soon as you get to the grocery store.

- Fees and Interest: Payday loans often come with higher fees and interest rates than traditional loans. It's crucial to understand these costs before you sign anything. Think of it like this: convenience comes at a price, so make sure you're aware of the total cost before you commit.

Is it Too Good to be True?

Hold on, before you get too excited, let’s be real. These loans aren’t a magic solution. They're a tool, and like any tool, they need to be used carefully. It's important to understand the potential downsides. These loans often come with high interest rates and fees, which can quickly add up if you're not careful. They can also lead to a cycle of debt if you rely on them too frequently.

Why Might You Consider an Income-Based Payday Loan?

Okay, so when would this type of loan actually be a good idea? Let's brainstorm some scenarios:

- Emergency Expenses: Your car breaks down, and you need it to get to work. A sudden medical bill pops up. These unexpected expenses can throw anyone for a loop. Think of it like needing a quick patch to get you back on the road.

- Bridging the Gap: Maybe you had an unexpected expense this month and need a little help covering your bills until your next paycheck arrives. This loan can act as a temporary buffer.

- Limited Credit History: If you're just starting out and haven't had time to build up a good credit score, these loans can be an option when traditional loans are out of reach. It's like starting a game on easy mode.

But, Always Proceed with Caution!

It's essential to remember that these loans are best used as a last resort. They should be a short-term solution, not a long-term financial strategy. Always explore other options first, like borrowing from friends or family, negotiating with creditors, or looking into community resources that can provide assistance.

The Fine Print: What to Watch Out For

Before you jump in, let’s talk about the potential pitfalls. It’s like navigating a maze – you need to know where the dead ends are.

- High Interest Rates: As we've mentioned, payday loans often have very high interest rates. This can make them expensive to repay, especially if you need to roll over the loan. Think of it like buying a candy bar at the airport – it's convenient, but you're paying a premium.

- Short Repayment Terms: The short repayment terms can be challenging for some people. If you're not able to repay the loan on time, you could incur additional fees and penalties.

- Risk of Debt Cycle: Relying on payday loans too frequently can lead to a cycle of debt. You might find yourself constantly borrowing to cover expenses, making it difficult to get ahead financially.

- Predatory Lenders: Unfortunately, some lenders are not reputable and may try to take advantage of borrowers. Be sure to research the lender thoroughly before you apply for a loan. Look for reviews, check their licensing, and make sure they're transparent about their fees and terms.

Doing Your Homework: Choosing a Lender Wisely

So, you’ve decided that an income-based payday loan might be a good option for you. Now, how do you choose a lender you can trust? It's like choosing a mechanic – you want someone who's reliable and won't rip you off.

- Research and Compare: Don't just go with the first lender you find. Take the time to research different lenders and compare their fees, interest rates, and repayment terms. It's like comparison shopping for the best deal.

- Read Reviews: See what other borrowers have to say about their experience with the lender. Online reviews can provide valuable insights. Think of it like asking your friends for recommendations.

- Check Licensing: Make sure the lender is licensed to operate in your state. This can help ensure that they're following regulations and protecting borrowers.

- Transparency is Key: A reputable lender will be transparent about their fees and terms. They should be upfront about the total cost of the loan and any potential penalties. If a lender is evasive or unclear, that's a red flag.

- Customer Service: Evaluate the lender's customer service. Are they responsive and helpful? Do they answer your questions clearly and thoroughly? Good customer service is a sign that the lender cares about their borrowers.

The Takeaway: Informed Decisions Are the Best Decisions

Payday loans based on income, not credit, can be a useful tool in certain situations. But they're not a one-size-fits-all solution. It’s essential to understand the pros and cons, do your research, and make an informed decision. Think of it like this: you're the captain of your financial ship, and you need to steer it wisely.

Always remember to explore all your options, and prioritize your financial well-being. Don't let short-term needs overshadow long-term goals. And if you're struggling with debt or financial challenges, don't hesitate to seek help from a financial advisor or credit counselor.

So, there you have it! A friendly look at payday loans based on income, not credit. Hopefully, this has helped shed some light on the topic and empower you to make smart financial choices. Now go out there and conquer your financial goals!