Understanding the nuances of Form 1099-INT is crucial for both payers and recipients of interest income. While the primary purpose of this form is to report taxable interest earned, a less commonly understood aspect involves "Other Accrued Interest Paid." This article delves into the intricacies of this reporting requirement, clarifying what it encompasses and why it matters.

What is Accrued Interest?

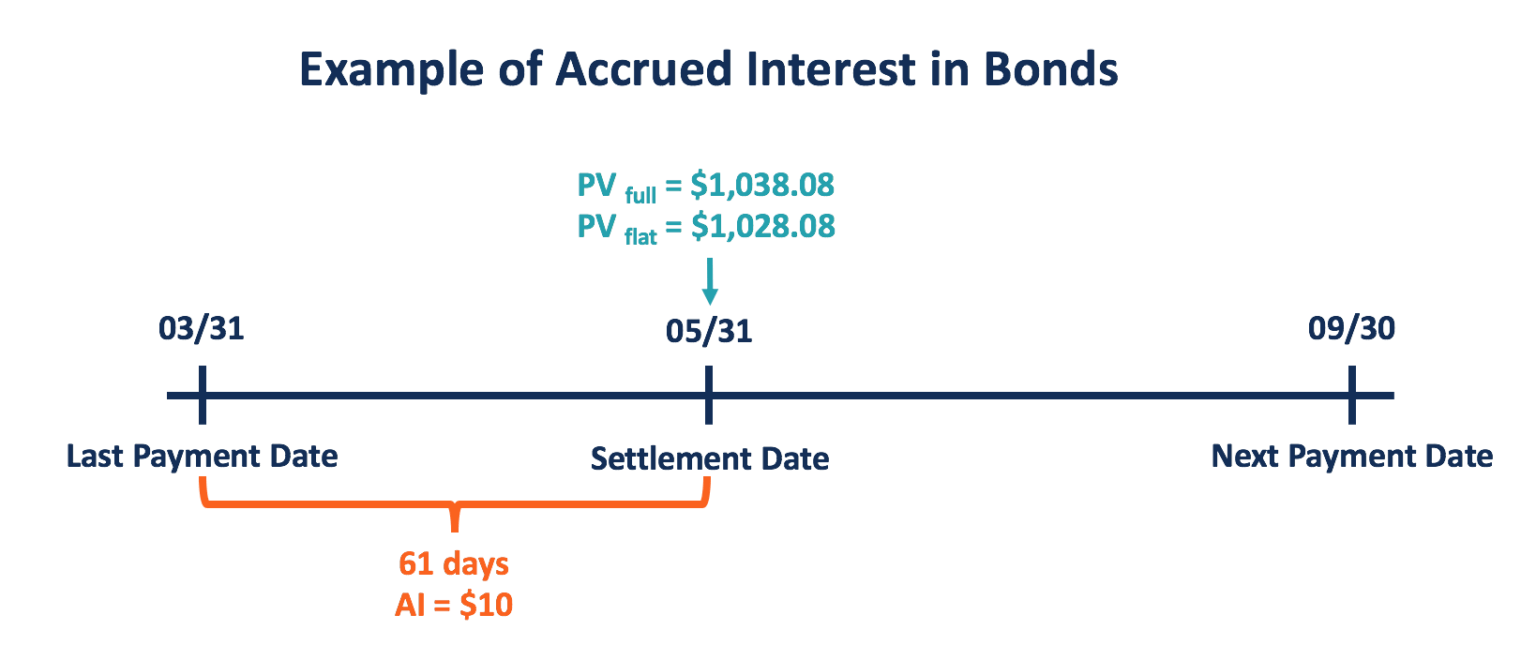

Before exploring the "Other Accrued Interest Paid" section, it's essential to grasp the concept of accrued interest. Accrued interest represents interest that has been earned but not yet paid out. It accumulates over time, typically daily, until the scheduled payment date. This is common in various financial instruments, including bonds, certificates of deposit (CDs), and other interest-bearing accounts.

Consider a bond that pays interest semi-annually. If the bond is sold between interest payment dates, the seller is entitled to the accrued interest up to the sale date. The buyer, in turn, will receive the full interest payment on the next scheduled date but will have effectively paid the seller for the portion of interest already earned.

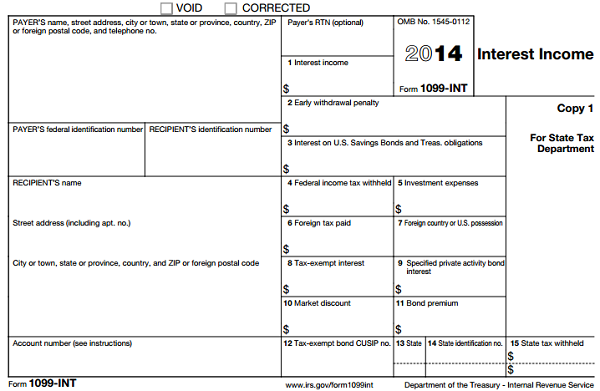

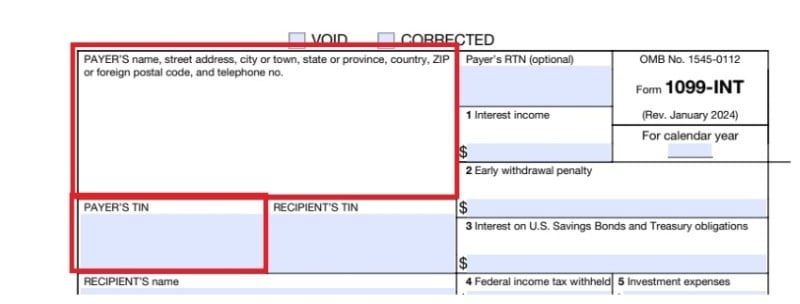

Box 4 of Form 1099-INT is specifically designated for "Federal income tax withheld." However, "Other Accrued Interest Paid" isn't explicitly reported in a dedicated box. Instead, it's generally understood to be included within Box 1, "Interest Income." This means the total interest reported in Box 1 might include both the actual interest earned and any accrued interest paid to the seller of a debt instrument.

The key here is to distinguish between the interest you actually earned and the accrued interest you paid to acquire the asset. While both are reported to you on Form 1099-INT, they are treated differently for tax purposes.

IRS Form 1099-INT Explained - How to Account for Accrued Interest on

Why "Other Accrued Interest Paid" Matters

The inclusion of accrued interest paid in Box 1 can lead to overreporting of taxable interest income if not properly adjusted. Taxpayers must understand how to account for this accrued interest to avoid paying taxes on income they didn't truly earn.

Accounting for Accrued Interest Paid: The IRS Perspective

The IRS allows you to reduce your taxable interest income by the amount of accrued interest you paid when you purchased a bond or other debt instrument. This prevents you from being taxed on interest that was already earned by the previous owner.

Form 1099-INT: Interest Income Definition

Here's how it generally works:

Identify Accrued Interest Paid: Review your purchase documentation (e.g., brokerage statements) to determine the amount of accrued interest you paid to the seller. This information should be clearly stated on the transaction confirmation.

Subtract from Box 1 Amount: Subtract the accrued interest paid from the total interest reported in Box 1 of your 1099-INT. The result is the actual taxable interest income you received.

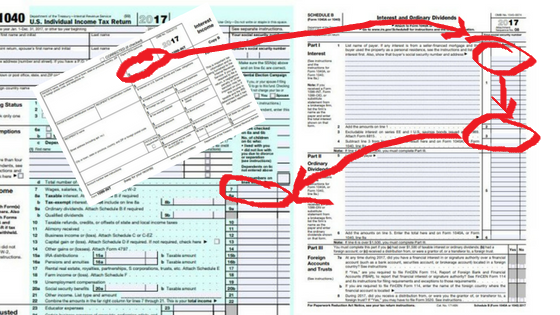

Report on Schedule B: When reporting your interest income on Schedule B (Form 1040), you can include a statement explaining the adjustment. For example, you might write "Accrued Interest Paid - See Attached Statement." On the attached statement, list the payer's name and the amount of accrued interest paid, clearly indicating that you are reducing the reported interest income by this amount.

Example: You purchase a bond in the secondary market on July 1st. The bond pays interest semi-annually on January 1st and July 1st. You pay $50 in accrued interest to the seller for the interest earned from January 1st to July 1st. At the end of the year, you receive a 1099-INT showing $200 in interest income from that bond. Your taxable interest income is actually $200 (reported) - $50 (accrued interest paid) = $150.

Irs 1099 Form Editable Form Resume Examples - Bank2home.com

Where to Find the Accrued Interest Paid Information

The most reliable source of information regarding accrued interest paid is your brokerage or financial institution. Your transaction confirmations and account statements should clearly specify the amount of accrued interest included in the purchase price. If you have trouble locating this information, contact your broker directly for assistance.

Common Scenarios Involving Accrued Interest

Bond Purchases: As illustrated in the example above, bond purchases in the secondary market are the most common scenario where accrued interest is involved.

Sales of Certificates of Deposit (CDs): While less frequent, accrued interest can also be relevant when selling a CD before its maturity date. Penalties may apply for early withdrawal, but if the CD is sold to another party, accrued interest needs to be accounted for.

Treasury Securities: Similar to corporate bonds, Treasury bills, notes, and bonds can also involve accrued interest when traded in the secondary market.

Potential Pitfalls and Considerations

Record Keeping: Maintaining accurate records of your bond purchases and sales is crucial for properly accounting for accrued interest. Keep copies of transaction confirmations and brokerage statements.

Complexity: The rules surrounding accrued interest can be complex, especially for those new to bond investing. Consulting with a tax professional is highly recommended if you're unsure how to handle these situations.

Wash Sales: Be aware of the wash sale rule, which can disallow a loss on the sale of a security if you purchase a substantially identical security within 30 days before or after the sale. This rule can also impact the treatment of accrued interest in certain situations.

Original Issue Discount (OID): If you purchase a bond with OID, the tax treatment can be even more complex. OID is the difference between a bond's stated redemption price at maturity and its issue price. It's essentially a form of interest that is accrued over the life of the bond.

Disclaimer: This article provides general information and should not be considered as tax advice. Consult with a qualified tax professional for personalized guidance on your specific situation.

How to Report Interest Income to IRS [Form 1040] | Serving Those Who Serve

The Importance of Accuracy and Transparency

Accurately reporting your interest income, including adjustments for accrued interest paid, is essential for complying with tax laws and avoiding potential penalties. Transparency in your tax filings demonstrates your commitment to fulfilling your tax obligations and helps to maintain a fair and equitable tax system.

Seeking Professional Guidance

If you find the concept of "Other Accrued Interest Paid" confusing or if you have complex investment holdings, seeking professional tax advice is always a prudent step. A qualified tax advisor can help you navigate the intricacies of tax law and ensure that you are properly reporting your income and deductions.

Remember:

Document everything relating to your investment transactions.

If you are unsure, seek professional advice from a tax expert.

Understand that accurate reporting is crucial for compliance.

Summary

While "Other Accrued Interest Paid" isn't a specifically labeled box on Form 1099-INT, understanding how it affects your taxable income is crucial. It represents interest you paid to a seller when purchasing a debt instrument, which needs to be subtracted from the total interest reported to avoid overpaying taxes. Proper record-keeping and, if necessary, seeking professional guidance are essential for accurately reporting this income and maintaining compliance with tax regulations. Ignoring it can lead to inaccurate tax calculations and potential issues with the IRS, highlighting the importance of understanding this aspect of Form 1099-INT reporting.

:max_bytes(150000):strip_icc()/ScreenShot2020-02-03at11.47.45AM-80a4044783b44a7b85412e8cd21bcbbc.png)

![How to Report Interest Income to IRS [Form 1040] | Serving Those Who Serve](https://stwserve.com/wp-content/uploads/2024/03/Picture1-1099-INT.png)