Movement Mortgage 30 Year Fixed Rates

Understanding mortgage interest rates is crucial for anyone considering purchasing a home. A mortgage is a loan secured by real property, and the interest rate determines the cost of borrowing. The 30-year fixed-rate mortgage is a prevalent choice, offering stability and predictability for homeowners. This article delves into the specifics of Movement Mortgage's 30-year fixed rates, providing a comprehensive overview for potential borrowers.

What is a 30-Year Fixed-Rate Mortgage?

A 30-year fixed-rate mortgage is a home loan with a fixed interest rate and a repayment period of 30 years. The "fixed-rate" aspect means that the interest rate remains constant throughout the entire 30-year term, ensuring that your monthly principal and interest payments remain the same, irrespective of market fluctuations. This stability is a significant advantage for budget-conscious homeowners.

For example, if you obtain a $300,000 mortgage at a fixed interest rate of 6%, your monthly principal and interest payment will remain consistent for the entire 30-year duration, allowing you to plan your finances accordingly.

Must Read

Movement Mortgage Overview

Movement Mortgage is a national mortgage lender that offers a variety of loan products, including 30-year fixed-rate mortgages. The company emphasizes a customer-centric approach, aiming to provide a transparent and efficient lending process. Understanding Movement Mortgage's offerings is the first step to potentially securing a mortgage with them.

Factors Influencing Movement Mortgage's 30-Year Fixed Rates

Several factors influence the interest rates offered by Movement Mortgage, similar to other lenders. These include:

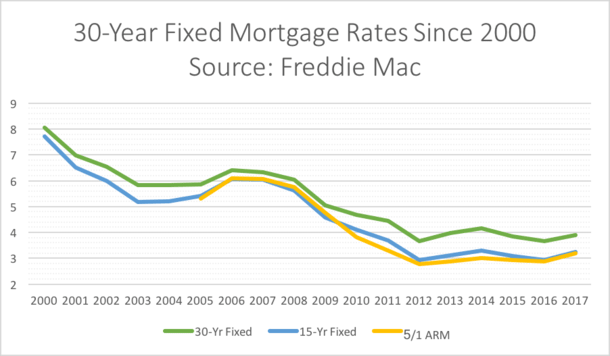

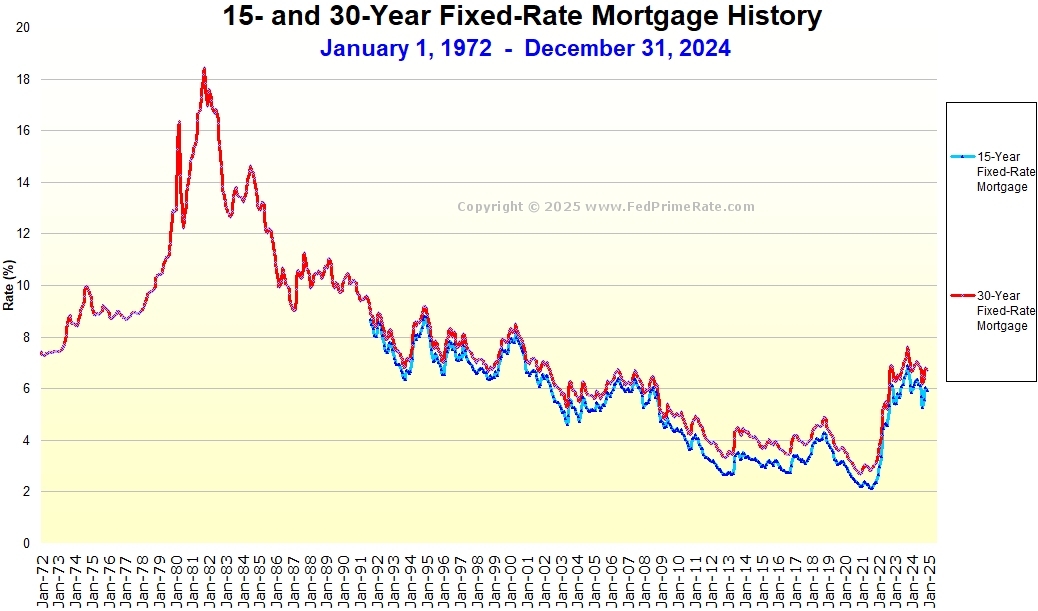

- The Federal Funds Rate: This is the target rate that the Federal Reserve (the Fed) wants banks to charge one another for the overnight lending of reserves. While the Fed Funds Rate doesn't directly translate into mortgage rates, it significantly influences the prime rate, which in turn affects mortgage rates.

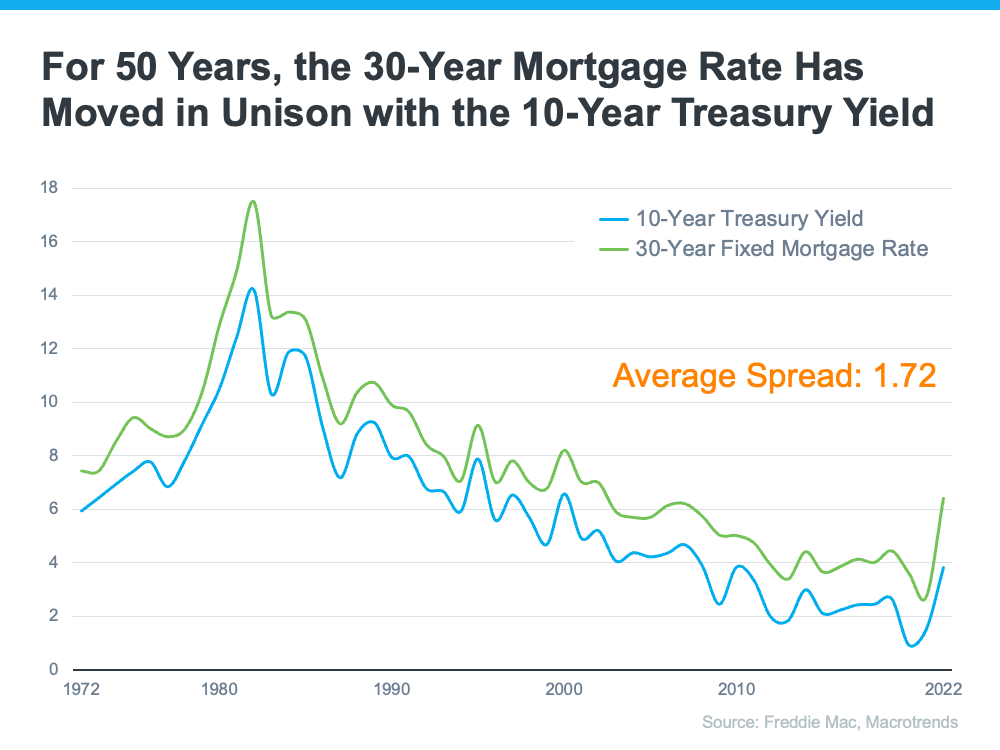

- The 10-Year Treasury Yield: This is considered a benchmark for long-term interest rates. Mortgage rates often follow the trend of the 10-year Treasury yield. When the yield rises, mortgage rates tend to increase as well.

- Inflation: Inflation erodes the value of money over time. Lenders factor in inflation expectations when setting interest rates to compensate for the decreased purchasing power of future payments. Higher inflation typically leads to higher interest rates.

- Economic Growth: A strong economy typically results in higher demand for credit, which can push interest rates upward. Conversely, a weak economy can lead to lower interest rates as lenders try to stimulate borrowing.

- Mortgage-Backed Securities (MBS): These are bundles of mortgages sold to investors. The demand for MBS directly affects mortgage rates. When demand is high, rates tend to be lower, and vice versa.

- Credit Score: Your credit score is a numerical representation of your creditworthiness. A higher credit score typically qualifies you for lower interest rates, as it indicates a lower risk of default.

- Down Payment: The size of your down payment affects the lender's risk. A larger down payment reduces the loan-to-value ratio (LTV), making you a less risky borrower and potentially qualifying you for a lower interest rate.

- Loan Type: Different loan types (e.g., conventional, FHA, VA) have varying risk profiles and eligibility requirements, which can impact interest rates.

- Debt-to-Income Ratio (DTI): This ratio compares your monthly debt payments to your gross monthly income. A lower DTI indicates that you have more disposable income, making you a less risky borrower.

- Property Location: Interest rates can vary slightly depending on the location of the property.

How to Find Movement Mortgage's 30-Year Fixed Rates

To find Movement Mortgage's current 30-year fixed rates, you can explore several avenues:

- Movement Mortgage's Website: Visit Movement Mortgage's official website. Many lenders display their current rates online, though these are often advertised rates and may not reflect the actual rate you'll qualify for.

- Contact a Loan Officer: The most accurate way to determine the rates you qualify for is to contact a Movement Mortgage loan officer directly. They can assess your financial situation and provide a personalized rate quote.

- Use Online Comparison Tools: Several websites allow you to compare mortgage rates from different lenders, including Movement Mortgage. These tools can give you a general idea of the market rates, but it's essential to verify the information with the lender directly.

The Application Process with Movement Mortgage

Applying for a 30-year fixed-rate mortgage with Movement Mortgage typically involves the following steps:

:max_bytes(150000):strip_icc()/4-16-6af7ee57050a458792245da7af98f493.png)

- Pre-Approval: Get pre-approved for a mortgage before you start shopping for a home. This involves providing Movement Mortgage with your financial information, such as income, assets, and debts. Pre-approval gives you a realistic idea of how much you can afford and strengthens your offer when you find a property.

- Loan Application: Once you've found a property and your offer has been accepted, you'll complete a formal loan application with Movement Mortgage. This application requires detailed information about your finances and the property.

- Document Submission: You'll need to provide supporting documentation to verify the information provided in your application. This may include pay stubs, tax returns, bank statements, and other financial documents.

- Underwriting: Movement Mortgage's underwriting team will review your application and supporting documents to assess your creditworthiness and the risk associated with lending to you.

- Appraisal: An appraisal will be ordered to determine the fair market value of the property. This ensures that the lender isn't lending more than the property is worth.

- Closing: If your application is approved, you'll proceed to closing. At closing, you'll sign the loan documents and pay closing costs, and the loan will be funded.

Tips for Securing the Best 30-Year Fixed Rate

Here are some practical tips to help you secure the best possible 30-year fixed rate from Movement Mortgage or any other lender:

- Improve Your Credit Score: Check your credit report for errors and take steps to improve your credit score. Paying bills on time, reducing your credit card balances, and avoiding new credit inquiries can all help boost your score.

- Save for a Larger Down Payment: A larger down payment reduces the lender's risk and may qualify you for a lower interest rate. Aim for a down payment of at least 20% if possible.

- Shop Around: Don't settle for the first rate you're offered. Get quotes from multiple lenders to compare rates and fees.

- Consider Discount Points: Discount points are upfront fees you pay to the lender in exchange for a lower interest rate. Determine whether paying points makes sense based on how long you plan to stay in the home.

- Negotiate: Don't be afraid to negotiate with the lender. If you've received a lower rate from another lender, let Movement Mortgage know. They may be willing to match or beat the offer.

- Lock in Your Rate: Once you've found a rate you're comfortable with, lock it in to protect yourself from potential rate increases during the loan processing period.

Practical Advice

Understanding the nuances of 30-year fixed-rate mortgages and how lenders like Movement Mortgage operate empowers you to make informed decisions. Stay informed about economic trends and how they affect interest rates. Regularly monitor your credit score and take steps to improve it. Comparing offers from multiple lenders is crucial to ensure you're getting the best possible rate. Don't hesitate to ask questions and seek clarification from loan officers about any aspects of the mortgage process you don't understand. By taking a proactive and informed approach, you can increase your chances of securing a favorable mortgage rate and achieving your homeownership goals.

:max_bytes(150000):strip_icc()/4-19-4d58b65dc4934bcfa046532acd24ebca.png)

:max_bytes(150000):strip_icc()/usvCv-last-90-days-of-30-year-mortgage-rate-average-0cffcbc963214551ac20083dcaf4799f.png)

:max_bytes(150000):strip_icc()/hZrRl-last-90-days-of-30-year-mortgage-rate-average-march-29-2024-5008b67132f04d5c9248f7d63e40827a.png)

:max_bytes(150000):strip_icc()/12-13-23-last-120-days-of-30-year-mortgage-rate-average-dec-13-2023-4b916fe38b9140f6b6d57a0968bd5b31.png)