Loans Based On Income Not Credit Score

In the realm of personal finance, securing a loan is often contingent upon one's credit score. This metric, a numerical representation of creditworthiness, heavily influences loan eligibility and interest rates. However, a growing number of lenders are offering an alternative: loans based on income, not primarily on credit score. This approach provides opportunities for individuals with limited or impaired credit histories to access much-needed funds.

Understanding Income-Based Loans

Income-based loans prioritize an applicant's ability to repay the loan based on their current income and employment stability, rather than focusing solely on their past credit behavior. While credit history might still be considered, it carries less weight in the approval process. The core principle is that a consistent income stream demonstrates a borrower's capacity to manage debt obligations.

Key Characteristics

- Emphasis on Income Verification: Lenders meticulously verify income through pay stubs, bank statements, and employment verification.

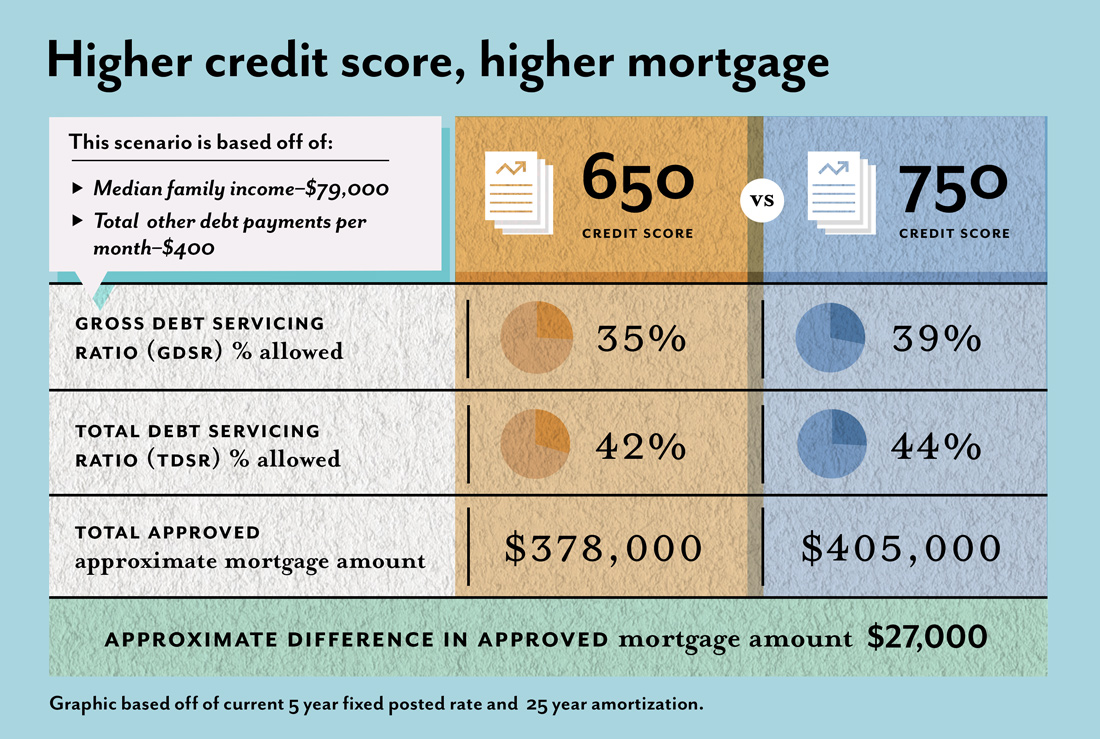

- Debt-to-Income Ratio (DTI): A crucial factor is the borrower's DTI, which represents the percentage of gross monthly income that goes towards debt payments. A lower DTI indicates a greater ability to comfortably handle additional debt.

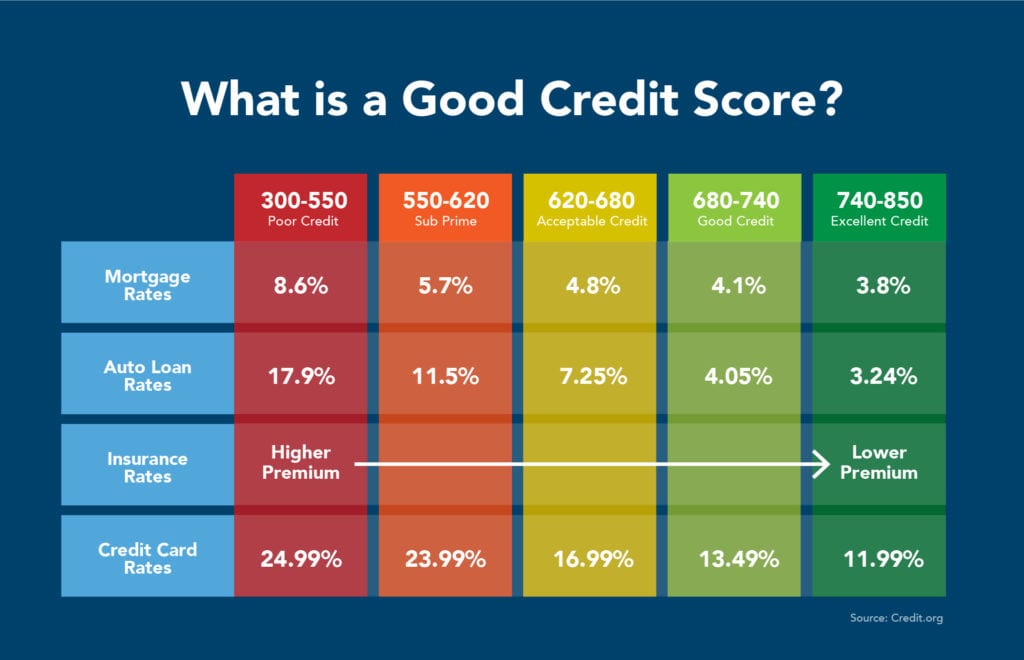

- Higher Interest Rates: Given the increased risk associated with lending to individuals with potentially less-than-perfect credit, income-based loans often carry higher interest rates compared to traditional loans.

- Potential for Smaller Loan Amounts: Lenders may offer smaller loan amounts to mitigate their risk, especially for borrowers with limited credit history.

- Alternative Data Sources: Some lenders may utilize alternative data sources, such as utility bill payments or rent payment history, to assess creditworthiness.

Types of Income-Based Loans

The specific types of income-based loans available vary depending on the lender and the intended purpose of the loan. Some common examples include:

Must Read

Personal Loans

Unsecured personal loans can be used for various purposes, such as debt consolidation, home improvement, or unexpected expenses. Lenders offering income-based personal loans focus on assessing your income and DTI to determine your ability to repay.

Example: Sarah needs to consolidate her high-interest credit card debt. Her credit score is low due to past financial difficulties. She applies for an income-based personal loan. The lender reviews her stable employment history, verifies her income with recent pay stubs, and calculates her DTI. Despite her low credit score, her manageable DTI and consistent income allow her to qualify for a loan, albeit at a slightly higher interest rate.

Auto Loans

While traditionally heavily reliant on credit scores, some auto lenders are beginning to consider income and employment stability more prominently. This can be particularly helpful for individuals needing reliable transportation for work.

Mortgage Loans

Although less common than with personal or auto loans, some mortgage lenders offer programs that place greater emphasis on income and employment history, especially for first-time homebuyers or those with non-traditional credit profiles. These programs often require higher down payments and may have stricter underwriting guidelines.

Payday Alternative Loans (PALs)

Offered by credit unions, PALs are designed as a more affordable alternative to payday loans. Credit unions consider income and ability to repay when approving PALs.

Benefits of Income-Based Loans

The primary benefit of income-based loans is the increased accessibility to credit for individuals who might otherwise be denied due to their credit history. This can be particularly advantageous for:

- Individuals with limited credit history: Young adults or those new to the country may have limited credit history, making it difficult to qualify for traditional loans.

- Individuals with past credit challenges: Past financial difficulties, such as bankruptcies or late payments, can negatively impact credit scores for years. Income-based loans offer a pathway to rebuild credit.

- Self-employed individuals: Self-employed individuals may have fluctuating income, making it challenging to meet the strict credit requirements of traditional lenders. Income-based loans can provide more flexible options.

Risks and Considerations

While income-based loans offer opportunities, it's crucial to be aware of the associated risks:

- Higher Interest Rates: As mentioned earlier, income-based loans typically come with higher interest rates, increasing the overall cost of borrowing.

- Potential for Debt Trap: If not managed carefully, the higher interest rates can lead to a debt trap, making it difficult to repay the loan.

- Stricter Repayment Terms: Lenders may have stricter repayment terms, such as shorter loan durations or more frequent payments.

- Limited Loan Amounts: The amount you can borrow may be restricted based on your income and DTI.

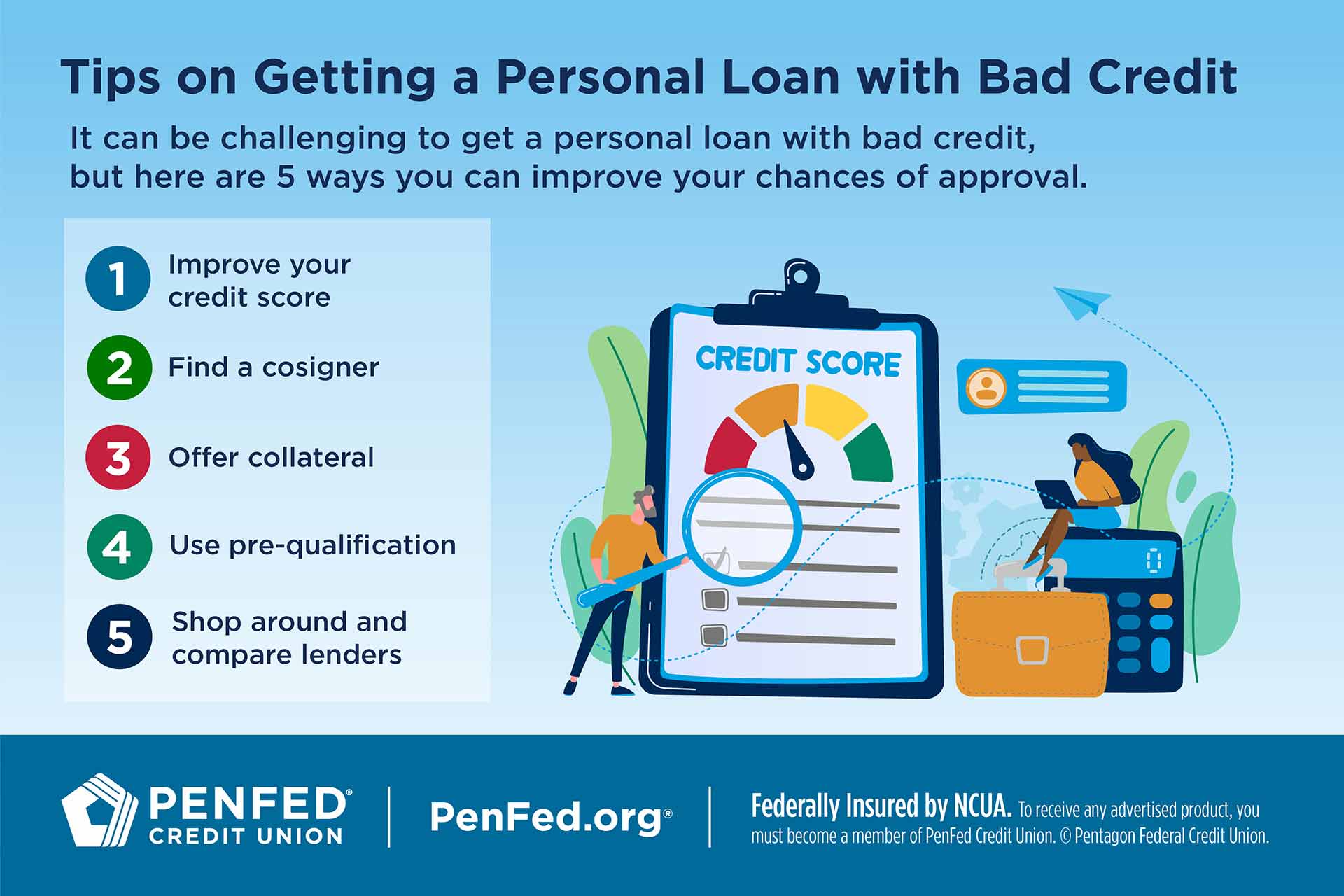

Securing an Income-Based Loan: A Step-by-Step Guide

If you're considering an income-based loan, follow these steps to increase your chances of approval and minimize potential risks:

- Assess Your Financial Situation: Carefully evaluate your income, expenses, and existing debt obligations. Determine how much you can realistically afford to repay each month. Calculate your Debt-to-Income (DTI) ratio.

- Improve Your DTI: If your DTI is high, explore ways to lower it. This might involve paying down existing debts or increasing your income.

- Gather Documentation: Collect all necessary documentation, including pay stubs, bank statements, tax returns, and proof of employment.

- Shop Around: Compare offers from multiple lenders. Pay close attention to interest rates, fees, repayment terms, and loan amounts. Do not settle for the first offer you receive.

- Read the Fine Print: Carefully review the loan agreement before signing. Understand all the terms and conditions, including any penalties for late payments or early repayment.

- Borrow Responsibly: Only borrow what you need and can comfortably repay. Avoid taking on more debt than you can handle.

Practical Advice and Insights

Income-based loans can be a valuable tool for accessing credit when traditional options are limited. However, they should be approached with caution and used responsibly. Here are some practical tips:

- Focus on Improving Your Credit Score: While pursuing an income-based loan, simultaneously work on improving your credit score. This will give you more options in the future and potentially qualify you for lower interest rates.

- Create a Budget: Develop a detailed budget to track your income and expenses. This will help you manage your finances effectively and ensure you can afford your loan payments.

- Consider Credit Counseling: If you're struggling with debt, consider seeking assistance from a credit counseling agency. They can provide guidance and support to help you get back on track.

- Explore Alternative Options: Before resorting to an income-based loan, explore other options, such as borrowing from family or friends, or seeking assistance from community organizations.

- Always prioritize responsible borrowing: Never borrow more than you can realistically afford to repay.

By understanding the principles of income-based loans and following these guidelines, you can make informed decisions and access the financial resources you need while minimizing the risks.