K Purchased A Life Insurance Policy

Okay, let's talk about something that might not be as exciting as planning a vacation to Bali, but is definitely more important in the long run: life insurance. Imagine your friend, let's call her K, just bought a life insurance policy. You might be thinking, "Life insurance? Sounds…adult. And maybe a bit morbid?" But trust me, it's not as scary as it sounds. In fact, it’s a super thoughtful, proactive, and dare I say, loving thing to do. Think of it like this: K just built a financial safety net, not just for herself, but for the people she cares about most.

Why Should You Even Care?

So, why are we even discussing K's life insurance policy? Because understanding what it means could seriously benefit you. Let’s face it, life can throw some curveballs. And while we can't predict the future (wouldn't that be cool, though?), we can prepare for it. Life insurance is like having an umbrella on a cloudy day – you might not need it, but you'll be incredibly grateful if it starts pouring rain.

The "What If" Factor (But In a Good Way!)

The core idea behind life insurance is pretty simple. It's a contract between you and an insurance company. You pay regular premiums (think of them as little deposits into your 'future security' fund), and in exchange, the insurance company promises to pay a lump sum of money (called a death benefit) to your beneficiaries if you were to, well, not be around anymore. Morbid, I know. But let's reframe it: it's about making sure your loved ones are taken care of if the unexpected happens.

Must Read

Think of it like this: imagine you’re baking a cake (a delicious chocolate one, perhaps!). You’ve carefully measured all the ingredients, followed the recipe perfectly, and created something wonderful. Life insurance is like adding a layer of frosting to that cake - it just makes everything a little sweeter and a little more secure. It protects the people who matter most to you.

Let's say K has a partner and a couple of adorable golden retrievers that she considers her family. If something were to happen to her, the death benefit from her life insurance policy could help her partner pay off the mortgage, cover living expenses, and even take care of those furry family members. It’s a way of ensuring their lives aren't completely upended financially during an already difficult time. See? Not so morbid, just…considerate.

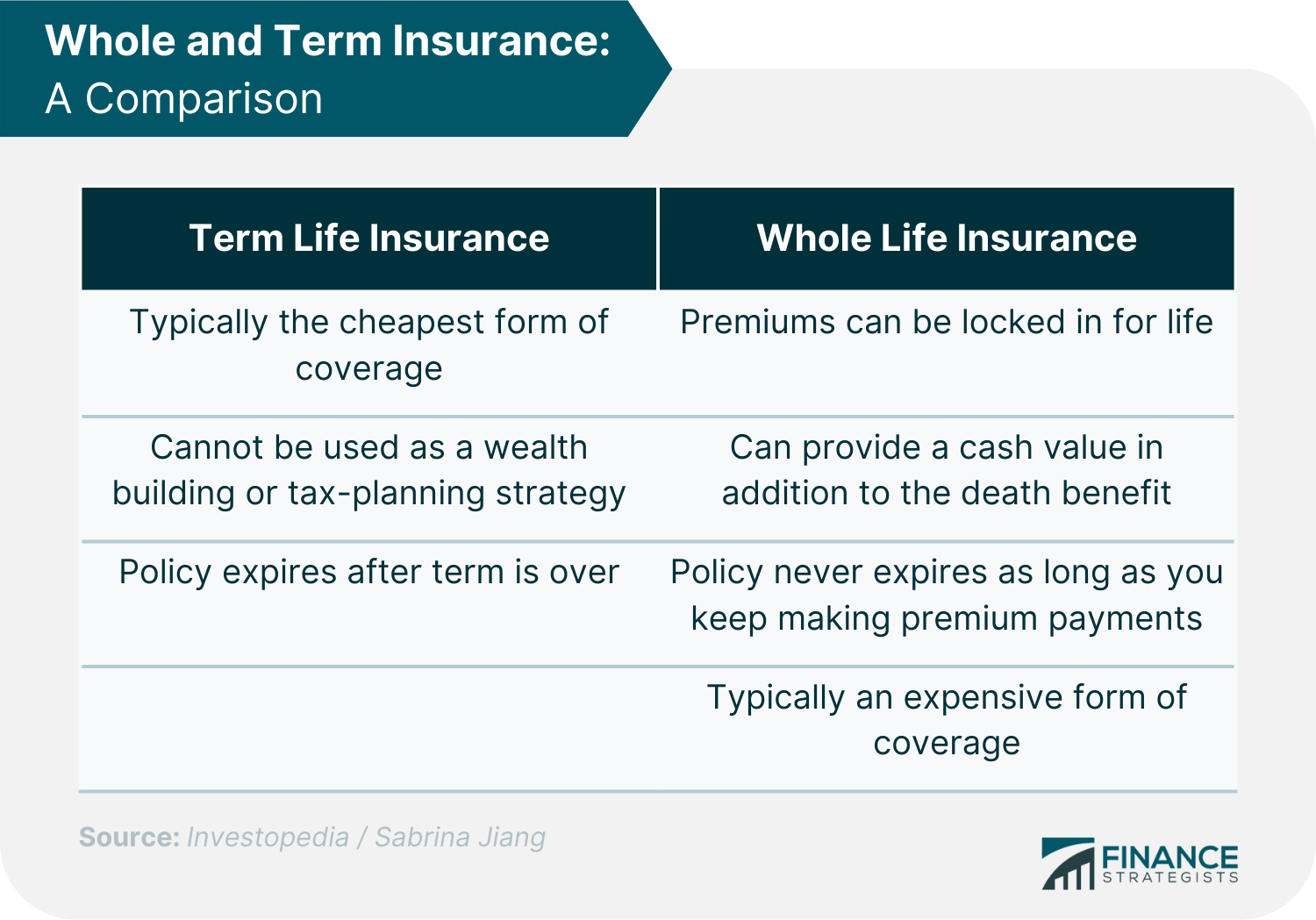

Beyond the Basics: Types of Life Insurance

Now, there are different flavors of life insurance, just like there are different flavors of ice cream. The two main types are term life insurance and whole life insurance.

Term life insurance is like renting an apartment. You pay for coverage for a specific period of time (the "term"), like 10, 20, or 30 years. It's generally more affordable than whole life insurance, which makes it a great option for young families or people on a budget. If you outlive the term, the policy expires, and you'd need to renew it (usually at a higher rate because you're older).

Whole life insurance is more like buying a house. It provides coverage for your entire life (as long as you keep paying the premiums), and it also builds cash value over time. This cash value can be borrowed against or withdrawn, which can be useful for things like paying for a child's education or supplementing retirement income. However, whole life insurance is typically more expensive than term life insurance.

:max_bytes(150000):strip_icc()/Life-Insurance-a8aee8e3024145a8b454ea19df030418.png)

K might have opted for a term life insurance policy because she's focused on covering her family during a specific period, like while her partner is building their business or while her pets are still young and require more care. Or she might have chosen a whole life policy because she wants the added benefit of cash value accumulation. The "best" type of life insurance depends entirely on your individual needs and circumstances.

Think About Your Own "What If"

Now, take a moment to consider your own situation. Do you have loved ones who depend on you financially? Maybe you have a spouse, children, aging parents, or even beloved pets. If something were to happen to you, would they be able to cover their expenses without your income? This is where life insurance can provide a huge sense of security.

:max_bytes(150000):strip_icc()/how-long-does-a-beneficiary-have-to-claim-a-life-insurance-policy-5075605-Final-ed5c6c806fb0446e8ce2bf27af06b4e1.jpg)

Imagine you're a single parent raising two energetic kids. Life is already a whirlwind of school drop-offs, soccer practices, and homework battles. If you were no longer around, would your children be able to continue living in their home, go to college, and pursue their dreams? Life insurance can help ensure that their future remains bright, even in the face of tragedy.

Or perhaps you're part of a dual-income household, and you and your partner are working towards a shared goal, like buying a home or starting a business. Life insurance can provide a safety net in case one of you passes away, allowing the other to continue pursuing those dreams without being burdened by overwhelming financial hardship.

It's Not Just About Money: It's About Peace of Mind

While the financial benefits of life insurance are undeniable, it's also important to consider the emotional benefits. Knowing that your loved ones will be taken care of if something happens to you can provide immense peace of mind. It's like knowing you've packed a first-aid kit on a camping trip – you hope you won't need it, but it's good to have it just in case.

Think about it: no one wants to leave their family with financial worries on top of the emotional grief of losing a loved one. Life insurance can help alleviate that burden, allowing your family to focus on healing and moving forward. It’s a gift of love and responsibility, ensuring their well-being even when you're not there.

It's easy to put off thinking about life insurance. It can seem like a complicated and unpleasant topic. But just like K, taking the time to learn about your options and choose a policy that fits your needs is one of the most responsible and caring things you can do for yourself and your loved ones. Don't wait until it's too late. Start exploring your options today!

Take the First Step: Educate Yourself!

So, what's the takeaway from K's wise decision? Don't be intimidated by life insurance. It’s not about dwelling on the negative; it’s about proactively planning for the future and protecting the people you love most. Research different types of policies, talk to a financial advisor, and get quotes from multiple insurance companies. Think of it as an investment in your family’s future – a future where they are financially secure, regardless of what life throws their way. You wouldn't leave your bike out in the rain without a lock, right? So, why leave your loved ones financially unprotected? Take that first step, and give yourself (and them!) the gift of peace of mind.

:max_bytes(150000):strip_icc():format(webp)/BestChildrensLifeInsuranceCompanies-v1-6f02811dfdcb4f7a8ebe56ad202a62b4.png)