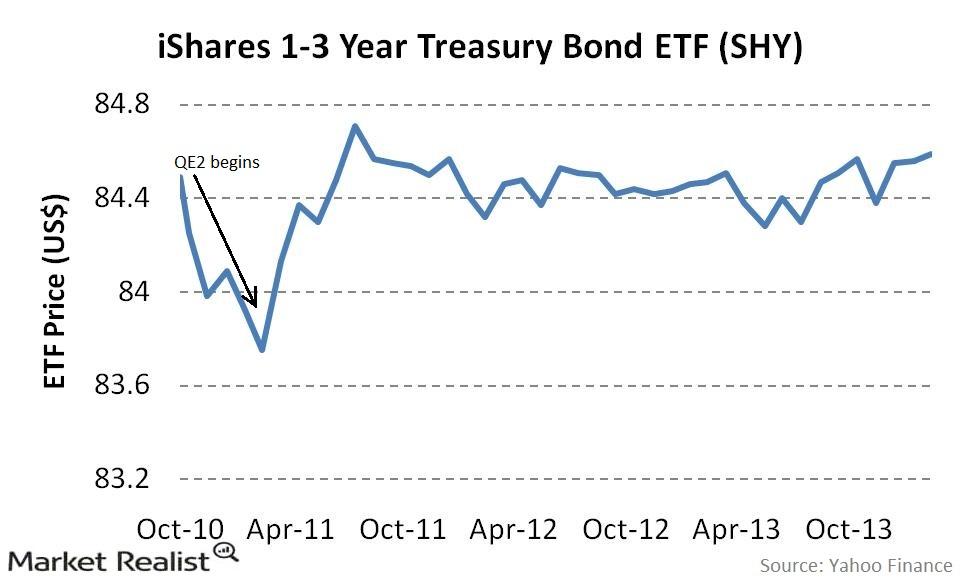

Ishares 1 3 Year Treasury Bond Etf

The iShares 1-3 Year Treasury Bond ETF (SHY) provides a relatively safe and liquid way to invest in short-term U.S. government debt. Knowing how it works can help you manage your cash, diversify your portfolio, and even understand broader economic trends.

Understanding the Basics

SHY tracks the investment results of an index composed of U.S. Treasury bonds with remaining maturities between one and three years. It's essentially a basket of these bonds, offering exposure to this specific segment of the fixed-income market without needing to purchase individual bonds directly.

Why Short-Term Treasuries?

Treasury bonds are considered very safe because they are backed by the full faith and credit of the U.S. government. Short-term maturities (1-3 years) are less sensitive to interest rate changes than longer-term bonds. This means that the price of SHY is less likely to fluctuate dramatically when interest rates rise or fall. If you're concerned about preserving capital and don't want to take on too much risk, this is a key characteristic.

Must Read

How SHY Works in Practice

When you buy shares of SHY, you're essentially buying a proportional share of the underlying bond portfolio. The ETF's price will fluctuate based on several factors, primarily changes in interest rates and the prices of the bonds held within the fund. SHY also pays out dividends, which represent the interest income earned from the bonds in the portfolio, minus the ETF's expense ratio. These dividends are typically paid monthly.

Applying This Knowledge in Daily Life and Work

Here's how you can leverage SHY for various financial goals:

Cash Management and Emergency Fund

A common use case for SHY is as a component of a cash management strategy or emergency fund. Traditional savings accounts offer low interest rates. While SHY carries slightly more risk than a FDIC-insured savings account, it generally provides a higher yield. You can park a portion of your emergency fund or short-term savings in SHY, knowing it offers liquidity (you can easily buy and sell shares) and a reasonable level of safety.

Example: You have $10,000 set aside for unexpected expenses. Instead of keeping it all in a low-yield savings account, you could allocate $5,000 to SHY. This could potentially generate more income while still providing relatively quick access to your funds if needed. Remember to consider your risk tolerance and investment time horizon.

Portfolio Diversification

SHY can be used to diversify a portfolio that is heavily weighted in stocks or other riskier assets. Bonds, in general, tend to have a low or even negative correlation with stocks. This means that when stocks decline, bonds may hold their value or even increase in value, helping to cushion the overall portfolio. Adding SHY provides a specific allocation to short-term U.S. Treasury bonds.

Example: If your portfolio is primarily composed of stocks, consider adding a small percentage (e.g., 5-10%) to SHY. This can help reduce the overall volatility of your portfolio and provide a more stable return profile. Rebalance your portfolio periodically to maintain your desired asset allocation.

Hedging Against Economic Uncertainty

Treasury bonds are often seen as a safe-haven asset during times of economic uncertainty. When investors become fearful of a recession or a stock market downturn, they often flock to the safety of U.S. Treasury bonds, driving up their prices (and driving down yields). By holding SHY, you can potentially benefit from this "flight to safety."

Important Note: SHY's performance is not guaranteed to be positive during economic downturns. While Treasury bonds tend to be relatively stable, they can still decline in value if interest rates rise unexpectedly or if investor sentiment shifts for other reasons.

Understanding Interest Rate Risk and Inflation

Even though short-term Treasury bonds are less sensitive to interest rate risk than longer-term bonds, they are not immune. If interest rates rise significantly, the price of SHY could decline. This is because newly issued bonds will offer higher yields, making existing bonds (with lower yields) less attractive. Also, inflation can erode the real return of SHY, especially if inflation rates are higher than the yield. Always consider the impact of inflation when evaluating fixed-income investments.

Comparing SHY to Other Fixed Income Investments

SHY is just one option among many fixed-income investments. Consider how it stacks up against other possibilities:

- Savings Accounts and CDs: SHY typically offers higher yields than savings accounts but carries more risk. CDs offer fixed interest rates for a specific term, providing more predictability but less liquidity.

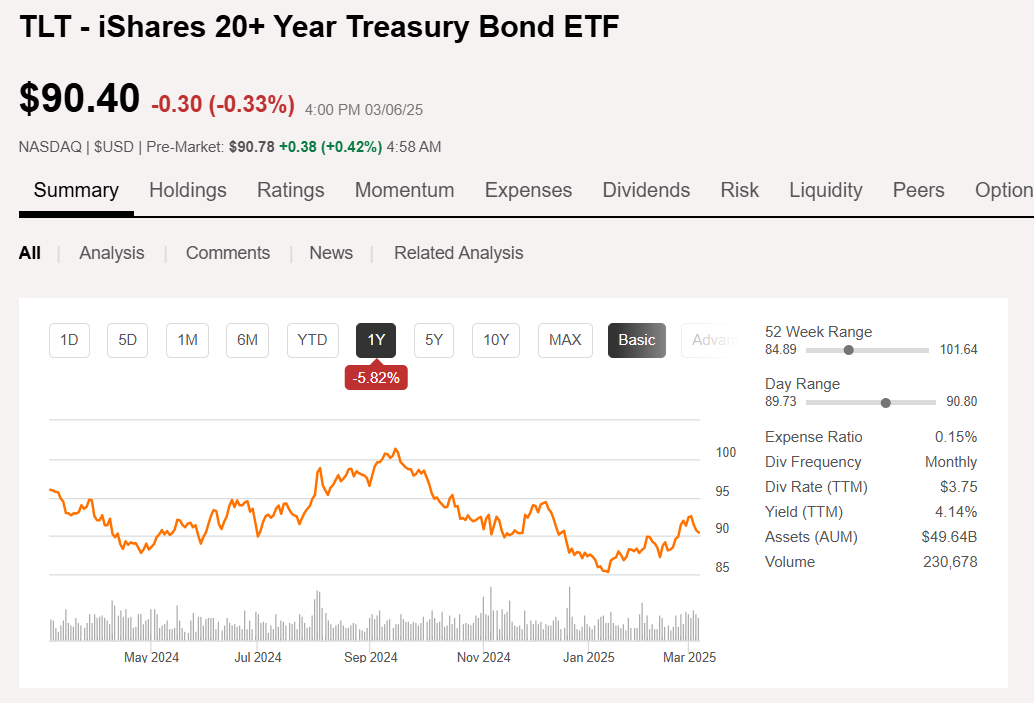

- Other Bond ETFs: Longer-term Treasury bond ETFs (e.g., TLT) offer potentially higher yields but are more sensitive to interest rate risk. Corporate bond ETFs offer higher yields than Treasury bond ETFs but carry credit risk (the risk that the issuer could default).

- Individual Bonds: Buying individual Treasury bonds allows you to tailor your portfolio to specific maturities and yields. However, it requires more research and involves higher transaction costs for smaller investors.

Tax Implications

The dividends paid by SHY are generally taxable as ordinary income at the federal level. Depending on your state and local tax laws, they may also be subject to state and local taxes. If you sell shares of SHY for a profit, you will be subject to capital gains taxes. Consult with a tax advisor to understand the specific tax implications of investing in SHY in your situation.

Practical Tips and Advice

- Dollar-Cost Averaging: Consider investing in SHY gradually over time using dollar-cost averaging. This can help mitigate the risk of buying at a high price and smooth out your returns.

- Rebalancing: Periodically rebalance your portfolio to maintain your desired asset allocation. If SHY has performed well and its allocation has grown too large, consider selling some shares and reinvesting in other assets.

- Monitor Interest Rate Trends: Keep an eye on interest rate trends and Federal Reserve policy. This can help you anticipate potential changes in the price of SHY.

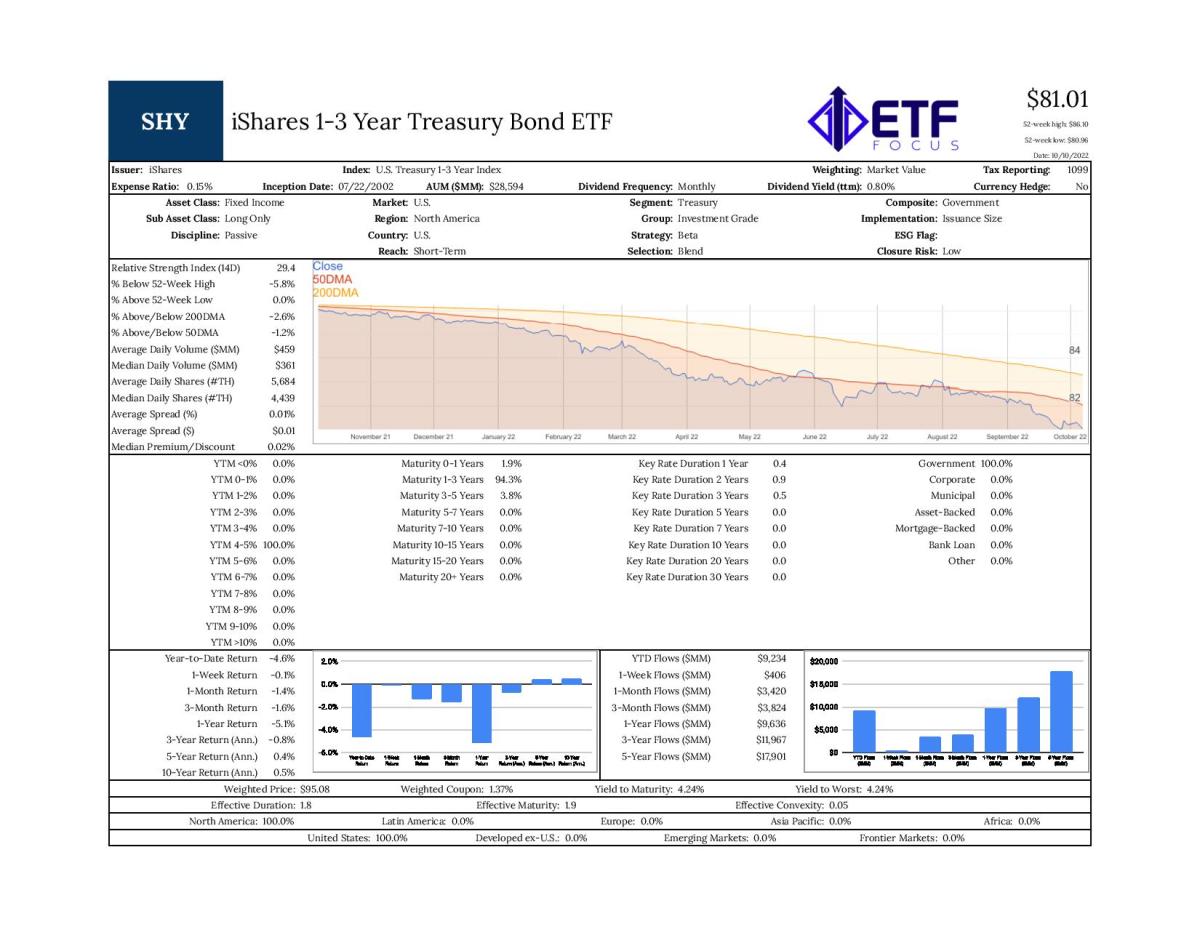

- Understand the Expense Ratio: SHY has a relatively low expense ratio, but it's important to be aware of it. The expense ratio represents the annual cost of managing the ETF, expressed as a percentage of the fund's assets.

- Consider Your Investment Time Horizon: SHY is best suited for short- to intermediate-term investment goals. If you have a long-term investment horizon, you may want to consider other assets with higher potential returns, such as stocks.

Checklist/Guideline

- Define Your Financial Goals: Determine why you want to invest in SHY. Is it for cash management, portfolio diversification, or hedging?

- Assess Your Risk Tolerance: Understand your ability to withstand potential losses. SHY is relatively safe, but it's not risk-free.

- Determine Your Investment Time Horizon: How long do you plan to hold SHY?

- Compare SHY to Other Options: Evaluate alternative fixed-income investments and consider their pros and cons.

- Understand the Tax Implications: Consult with a tax advisor to understand how SHY will affect your taxes.

- Invest Gradually: Consider using dollar-cost averaging to mitigate risk.

- Monitor Performance: Track the performance of SHY and make adjustments as needed.

- Rebalance Periodically: Maintain your desired asset allocation by rebalancing your portfolio.