Is Mortgage Payable A Current Liability

Okay, picture this: you're at a party, right? And someone starts talking about, like, liabilities and assets. Suddenly, everyone's eyes glaze over. But then you chime in, knowing exactly what's up with, say, a mortgage payable. You're the financial guru of the night! That's what we're aiming for here.

Seriously though, understanding basic accounting terms, like whether your mortgage is a current liability, is super important, especially if you're managing your own finances or even just want to sound impressive at parties. 😉 So, let’s dive in!

What's a Liability Anyway? (And Why Should I Care?)

First, let's break down the jargon. A liability is simply something you owe to someone else. Think of it as a debt. It could be money borrowed from a bank, services you've received but haven't paid for yet, or even wages owed to your employees.

Must Read

Why should you care? Well, liabilities are a key part of understanding your overall financial health. Knowing what you owe helps you plan for the future, make informed decisions, and avoid nasty surprises (like suddenly realizing you can't afford that yacht you've been eyeing – just kidding… mostly!).

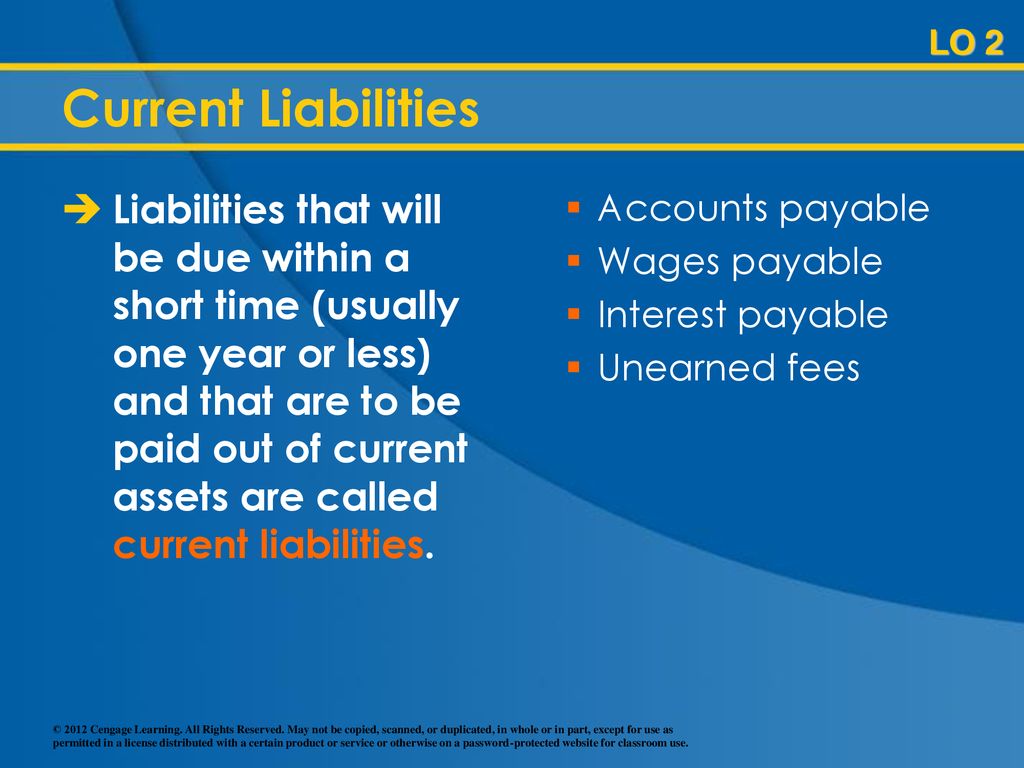

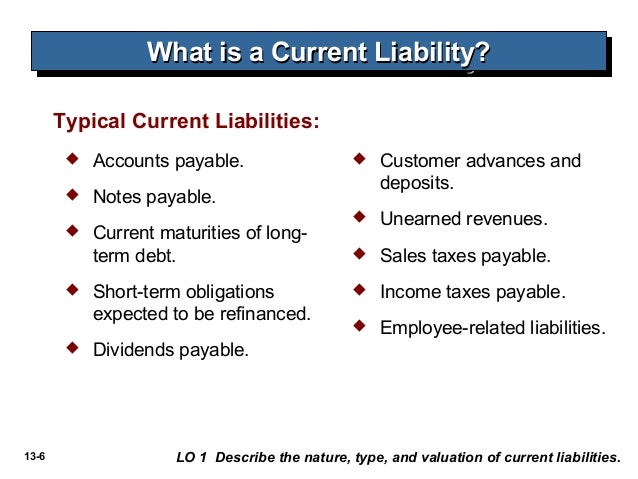

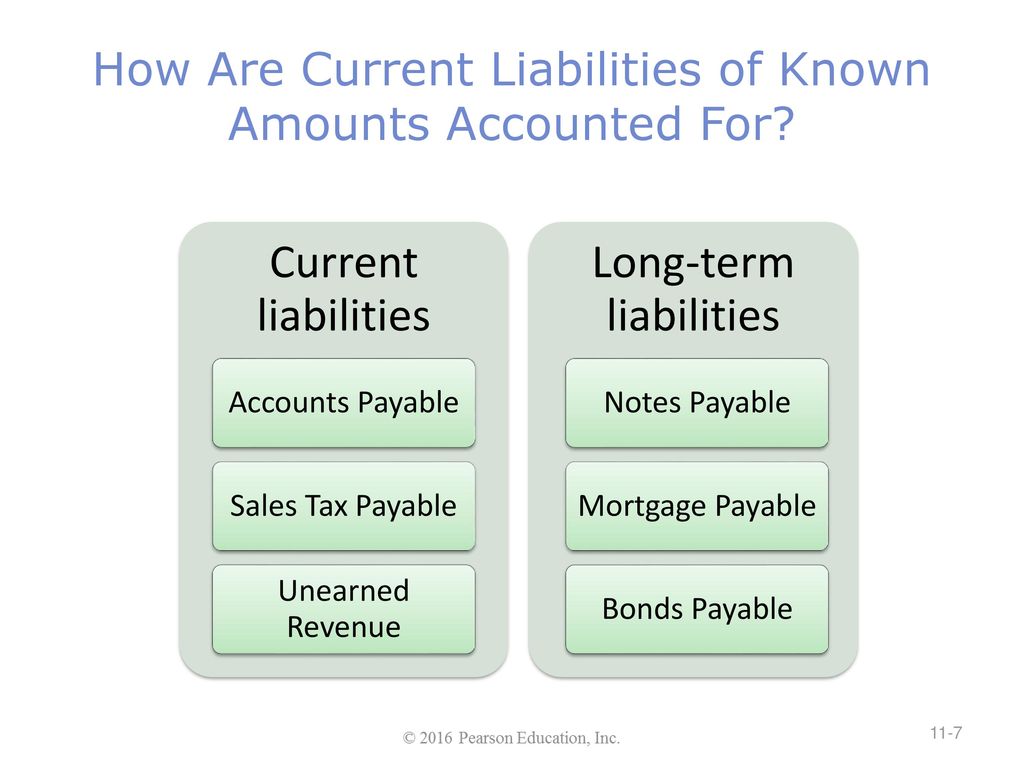

Current vs. Non-Current Liabilities: The Big Divide

Liabilities come in two main flavors: current and non-current. The difference boils down to time. This is important, so pay attention!

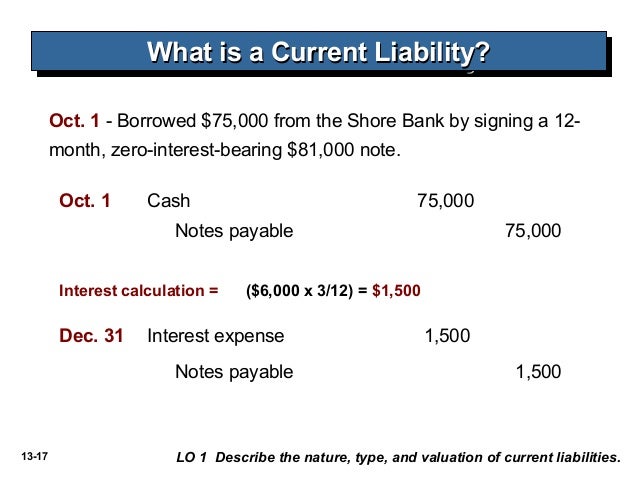

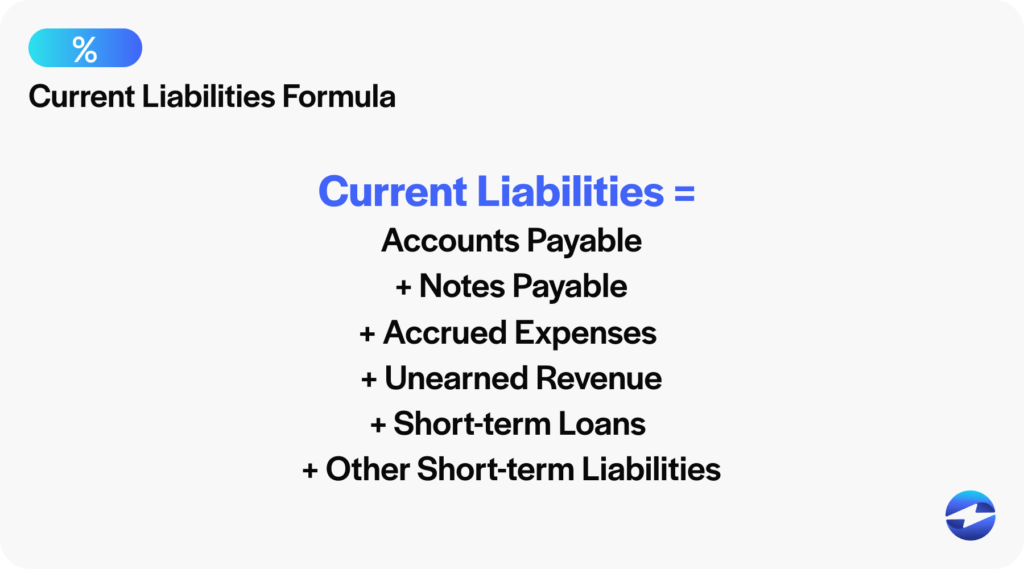

- Current Liabilities: These are debts you're expected to pay off within one year. Think of things like accounts payable (money you owe to suppliers), short-term loans, and the portion of a long-term debt that's due within the next year.

- Non-Current Liabilities: These are debts that are due in more than one year. Examples include long-term bank loans, bonds payable, and deferred tax liabilities. Basically, debts you can kick down the road a little (or a lot!).

So, that's the basic difference. Now, how does this relate to your mortgage?

Mortgage Payable: The Million-Dollar (Or, You Know, $300,000) Question

Okay, let's get to the heart of the matter: Is your mortgage payable a current liability? The answer, as with many things in finance, is: it depends. (I know, I know, you hate that answer. But it's true!)

Here's the breakdown:

- The Portion Due Within One Year: The portion of your mortgage that you're scheduled to pay off within the next 12 months is considered a current liability. This includes both the principal and interest payments.

- The Remaining Balance: The remaining balance of your mortgage, the part you won't pay off within the next year, is classified as a non-current liability (also known as a long-term liability).

Let's say you have a $300,000 mortgage. And let's also pretend that your mortgage statement says that over the next 12 months, you'll pay off $10,000 of the principal balance. That $10,000 is your current liability. The remaining $290,000 is your non-current liability.

See? Not so scary after all. 😊

Why This Matters for Your Financial Statements

So why do accountants split the mortgage into current and non-current portions? Because it provides a clearer picture of your financial health. Here’s how:

- Understanding Short-Term Obligations: By knowing the amount of your mortgage due within the year, you can assess your ability to meet your immediate financial obligations. This is crucial for managing your cash flow and avoiding financial strain. Think of it like this: can you really afford that fancy new gadget if it means struggling to make your mortgage payments?

- Assessing Long-Term Solvency: The non-current portion of your mortgage helps lenders and investors evaluate your long-term financial stability. A large non-current liability can indicate a higher level of financial risk, but it’s also normal for mortgages. It’s all about context!

- Accurate Financial Reporting: Correctly classifying your mortgage liability ensures that your financial statements accurately reflect your financial position. This is essential for making sound financial decisions and complying with accounting standards. (Okay, maybe you don't personally care about accounting standards, but your bank definitely does!)

How to Figure Out Your Current Mortgage Liability

Alright, so now you know why it's important to separate your mortgage liability. But how do you actually figure out the current portion? Thankfully, it's usually pretty straightforward.

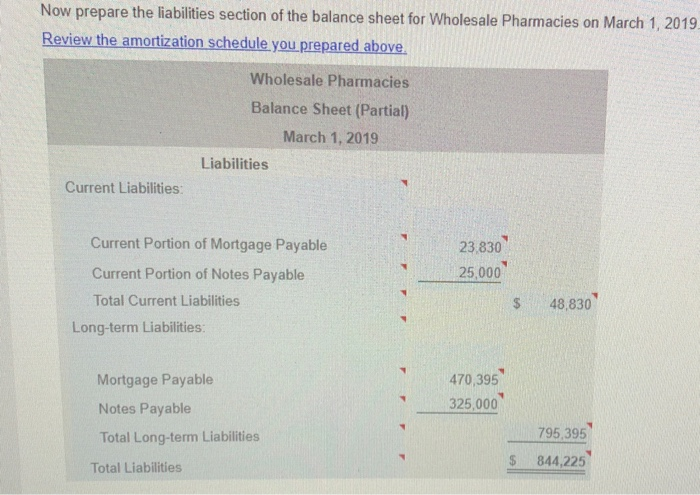

- Check Your Mortgage Statement: Your mortgage statement typically shows a breakdown of your payments, including the amount allocated to principal and interest. The portion of the principal payment that will be made within the next 12 months is your current mortgage liability. Pro Tip: Look for a section labeled "Principal Reduction" or something similar.

- Use an Amortization Schedule: An amortization schedule is a table that shows the breakdown of each mortgage payment over the life of the loan. It details how much of each payment goes towards principal and interest. You can usually get this from your lender or create one yourself online (there are tons of free tools available!). Just add up all the principal payments scheduled for the next 12 months.

- Consult Your Accountant: If you're feeling unsure, don't hesitate to ask your accountant for help. They can review your mortgage documents and accurately determine the current and non-current portions of your liability. (That's what they're there for, after all!)

A Quick Example: Let's Get Real

Let's say you get your mortgage statement and see that your monthly payment is $1,500. Of that, $500 goes toward principal and $1,000 goes toward interest. Over the next 12 months, you'll pay a total of $6,000 toward the principal ($500/month * 12 months).

Therefore, your current mortgage liability is $6,000.

The remaining mortgage balance (let's say it's $294,000 after that first year) is your non-current mortgage liability.

Simple as that! 🎉

Potential Pitfalls and Gotchas (Things to Watch Out For!)

While calculating your current mortgage liability is usually straightforward, there are a few things to keep in mind:

- Prepayments: If you make extra principal payments, this will affect the amount of your current mortgage liability. You'll need to adjust your calculations accordingly. (Good problem to have, though, right?)

- Refinancing: If you refinance your mortgage, you'll essentially be taking out a new loan. This will create a new amortization schedule, and you'll need to recalculate your current and non-current liabilities.

- Adjustable-Rate Mortgages (ARMs): With ARMs, your interest rate (and therefore your monthly payment) can change over time. This will affect the amount of principal you pay each month, so you'll need to update your calculations accordingly. Side Note: ARMs can be a bit tricky, so make sure you fully understand the terms before signing up for one.

- Changes in Accounting Standards: While unlikely to affect everyday people, accounting standards can change over time. It’s good to be aware of this, especially if you are recording this for business or investing purposes. If major changes happen, consult a professional!

Why All This Matters in the Real World

Okay, so we've covered the basics of mortgage liabilities and how to classify them. But why does this matter in the real world? Here are a few reasons:

- Personal Financial Planning: Understanding your mortgage liabilities helps you create a realistic budget, track your progress towards paying off your debt, and make informed decisions about your spending and saving habits.

- Credit Score: While your mortgage liability itself doesn't directly impact your credit score, your ability to make timely mortgage payments does. Consistently paying off the current portion of your mortgage on time is a great way to build a positive credit history.

- Investment Decisions: Knowing your mortgage obligations can help you make informed investment decisions. For example, you might decide to prioritize paying down your mortgage before investing in other assets, or vice versa. It's all about finding the right balance for your individual circumstances.

- Real Estate Investments: If you're involved in real estate investing, understanding mortgage liabilities is essential for evaluating the profitability and risk of different properties.

Final Thoughts: You're Now a Mortgage Liability Master!

So, there you have it! You've successfully navigated the sometimes-confusing world of mortgage liabilities. You now know that the portion of your mortgage due within one year is a current liability, while the remaining balance is a non-current liability. And you know why this distinction matters.

Now go forth and impress your friends at parties with your newfound financial knowledge! Just kidding (sort of). The real benefit is that you're now better equipped to manage your finances, make informed decisions, and achieve your financial goals. Congratulations!

Remember, personal finance is a journey, not a destination. Keep learning, keep asking questions, and keep striving to improve your financial literacy. You've got this!

Disclaimer: I am not a financial advisor, and this article is for informational purposes only. Always consult with a qualified professional before making any financial decisions.