Is 650 A Good Credit Score To Buy A Car

Alright, gather 'round, friends! Let's talk about something near and dear to everyone's heart (or at least their wallets): buying a car! And more specifically, what that magical number, your credit score, has to do with it. Today's burning question: Is 650 a good credit score to buy a car? Buckle up, because we're about to take a wild ride through the world of finance!

The Credit Score Conundrum: 650 - Friend or Foe?

So, you've checked your credit score (hopefully not by sacrificing a chicken to the Credit Gods... there are easier ways, I promise!), and it's sitting pretty at 650. The question is: are you cruising down Easy Street, or are you stuck in a financial pothole? The answer, my friend, is… it's complicated. Think of it like ordering a pizza. A 650 credit score isn't the gourmet, truffle-oil-drizzled masterpiece. It's more like a solid, dependable pepperoni. It gets the job done, but you might wish you'd sprung for extra cheese.

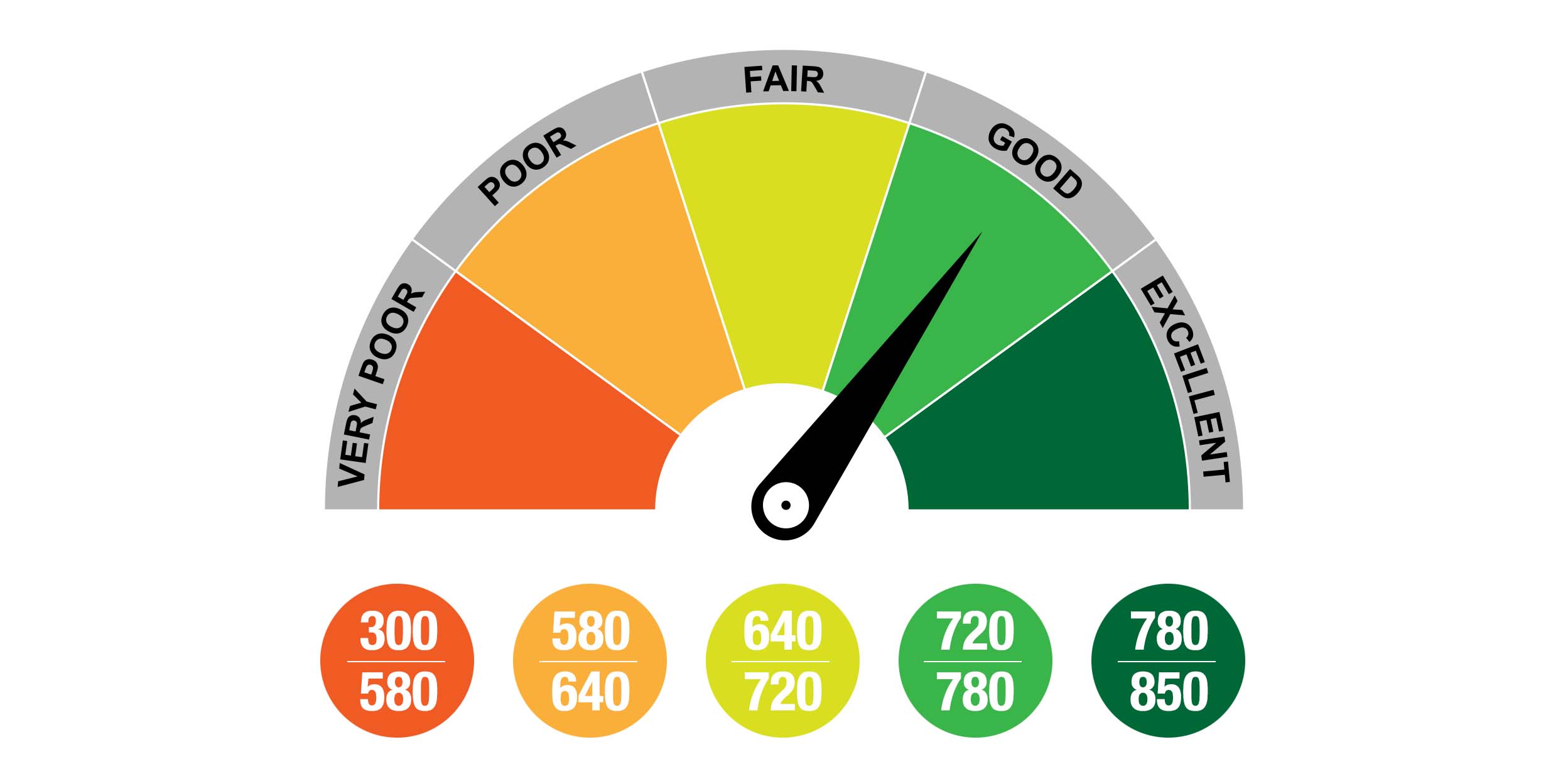

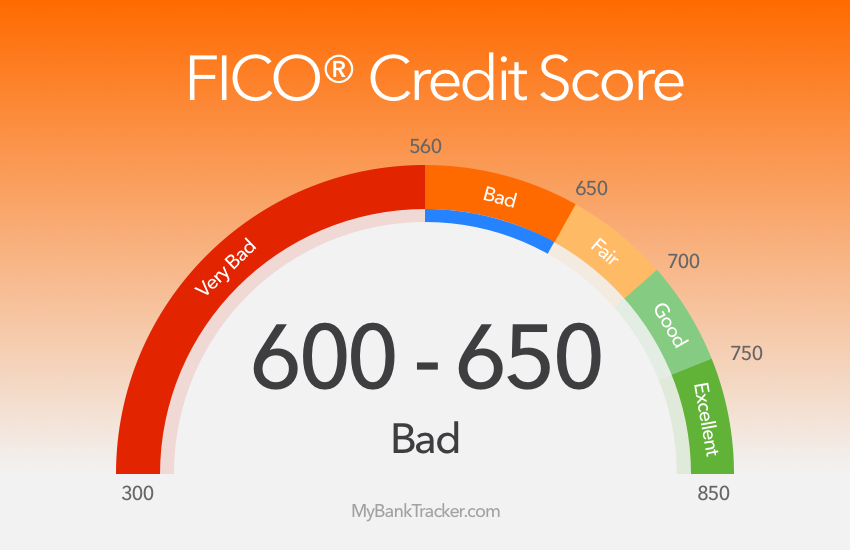

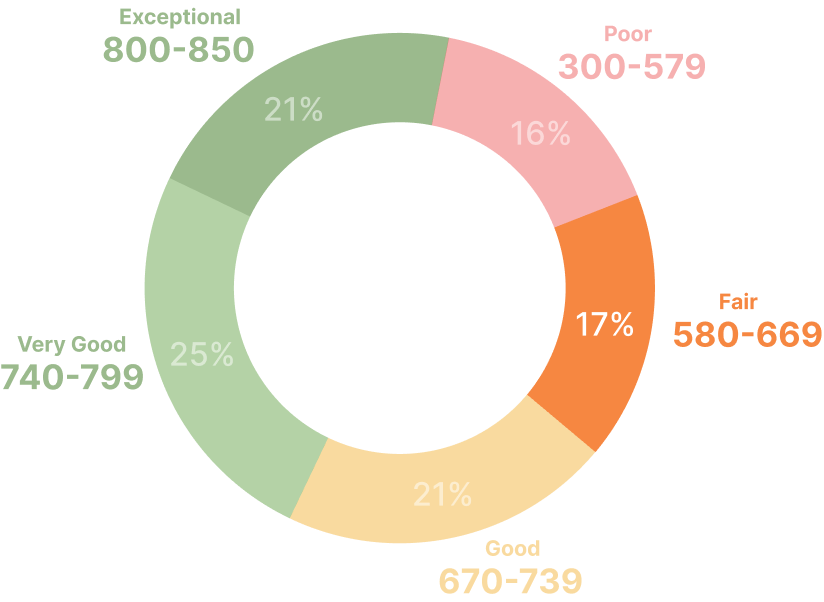

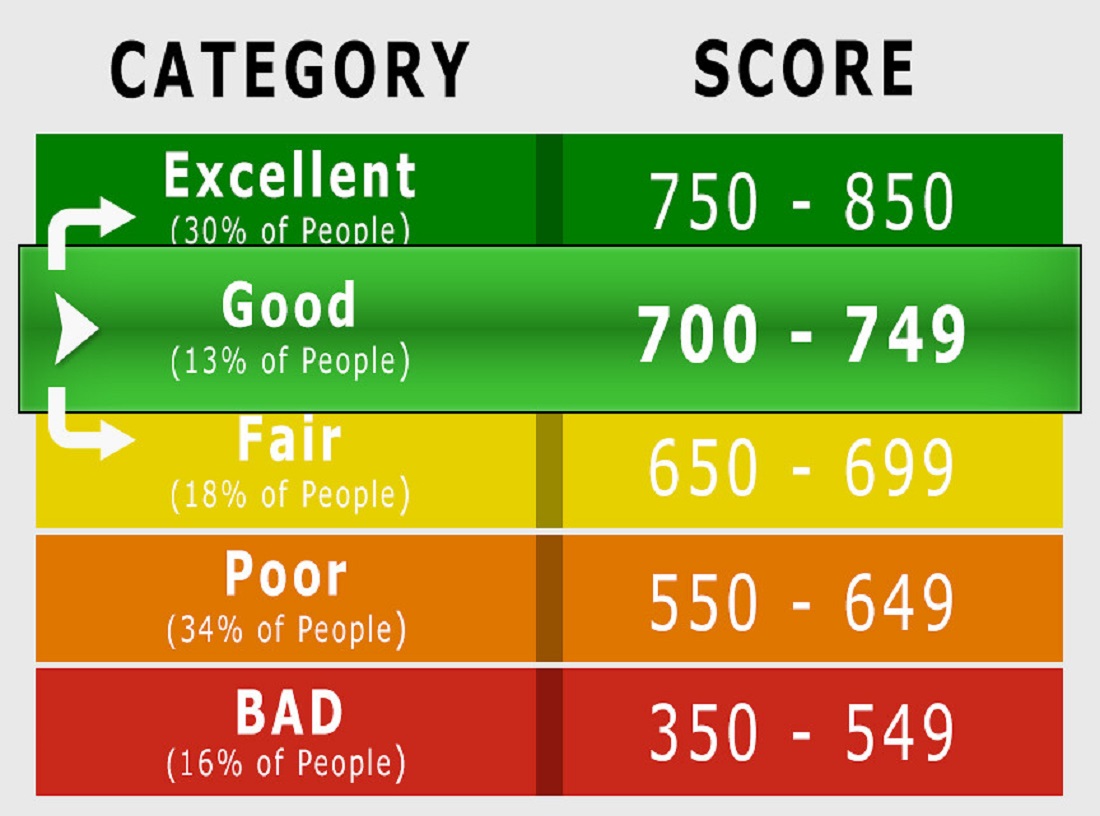

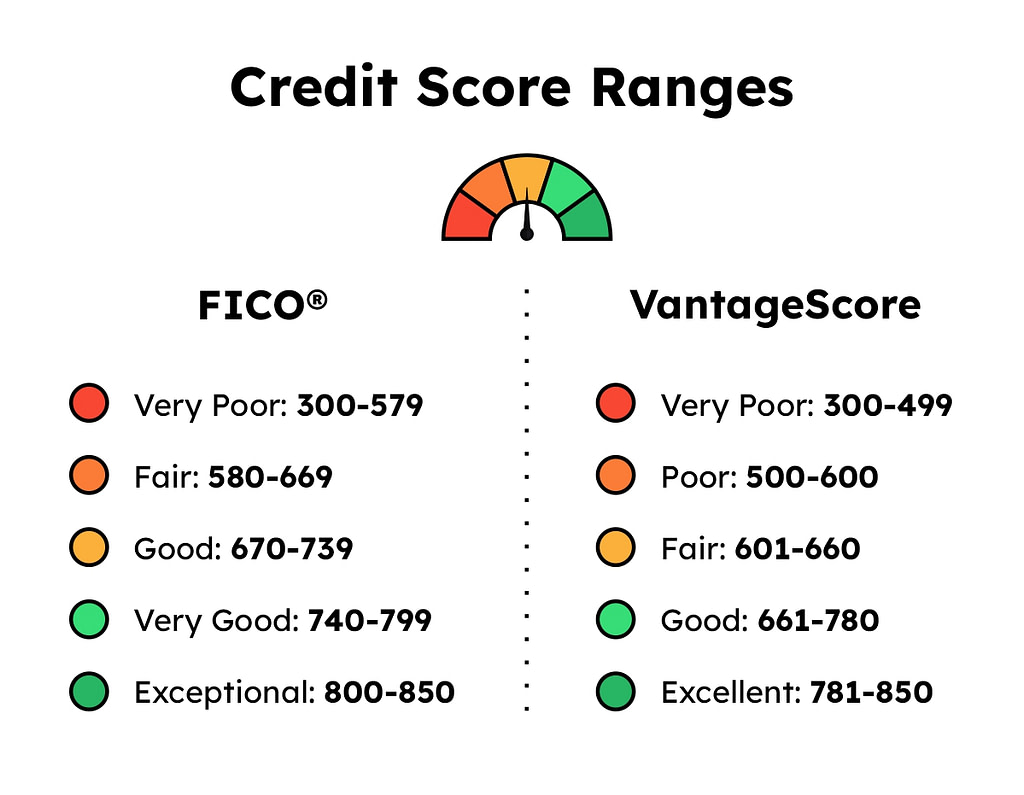

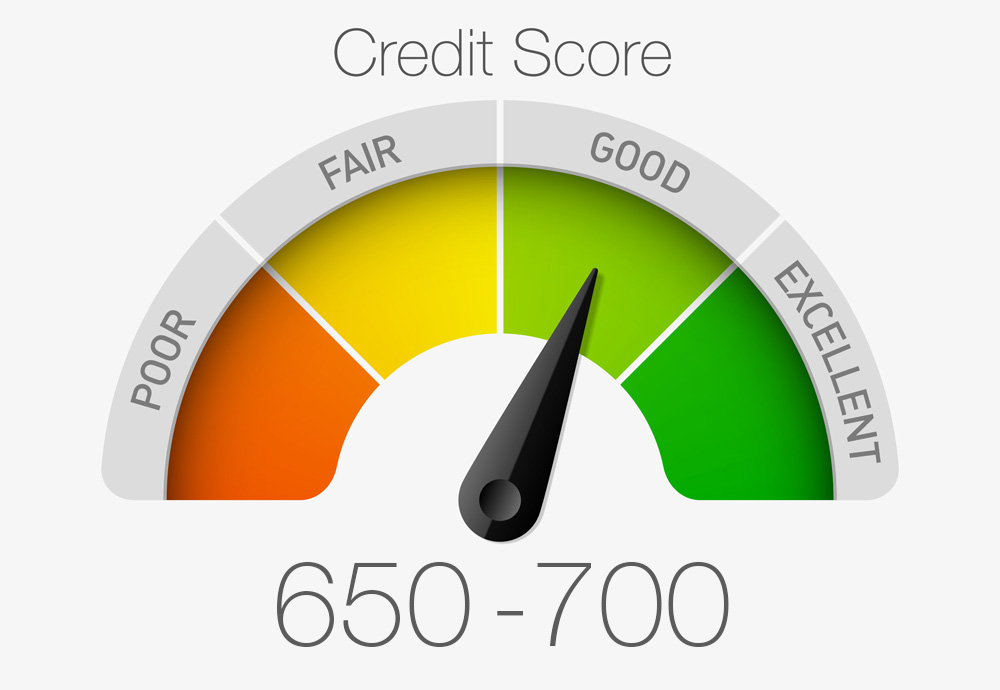

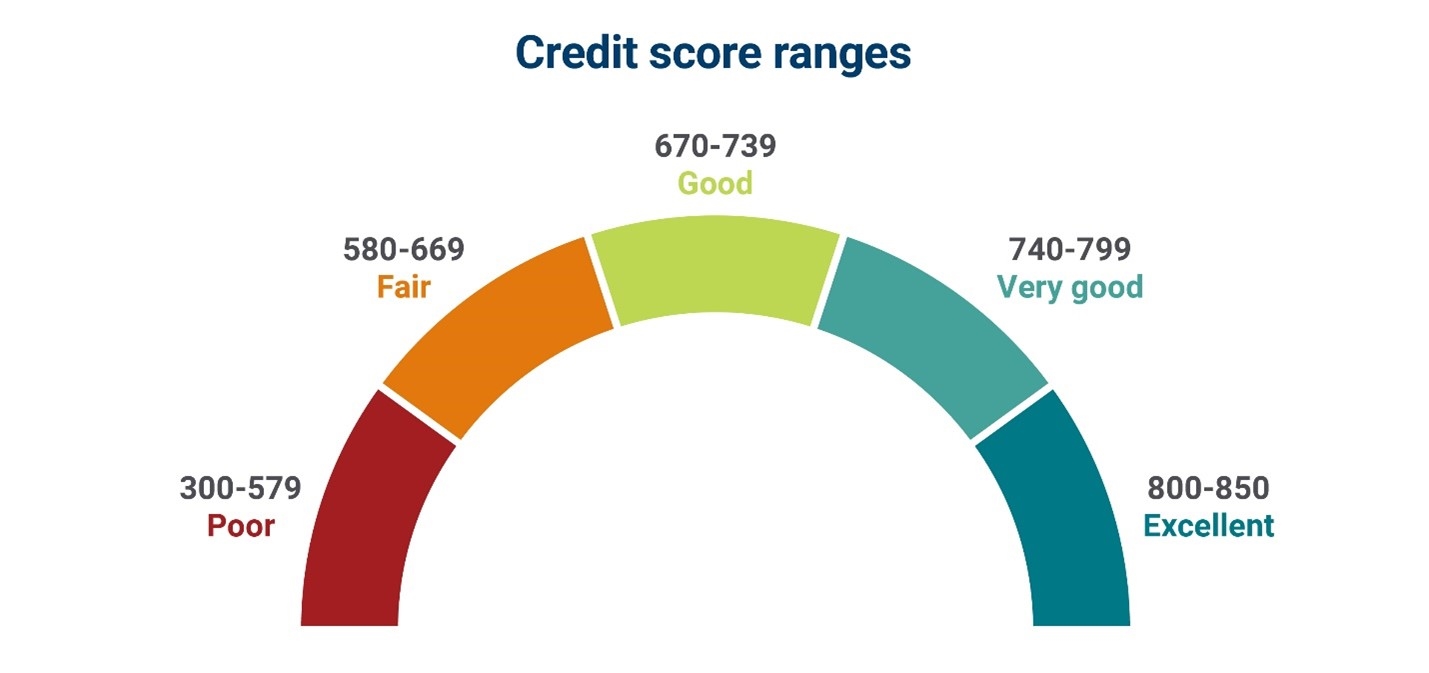

A 650 credit score generally falls into the "fair" credit score range. It’s not terrible, but it's not exactly going to roll out the red carpet at the dealership either. In the grand scheme of credit scores (which range from 300 to 850), 650 is hanging out somewhere in the middle. You're not in the credit score wilderness, but you’re also not exactly sipping mojitos on Credit Score Island.

Must Read

The Good News (Because There's Always Some, Right?)

The good news is, you can absolutely buy a car with a 650 credit score. You're not relegated to walking, biking uphill in a blizzard, or relying on your eccentric Aunt Mildred and her "reliable" (read: held together with duct tape) station wagon. Dealerships are in the business of selling cars, and they know that not everyone has a perfect credit score. They're willing to work with you... for a price.

The Not-So-Good News (Prepare for a Slight Bump in the Road)

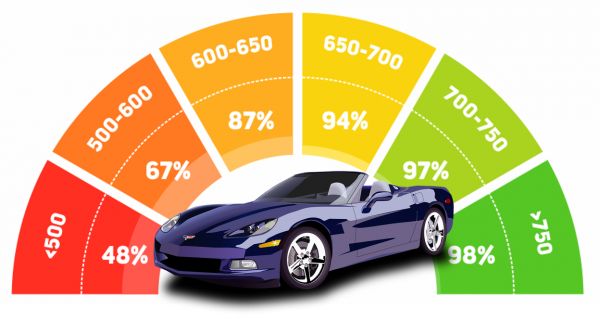

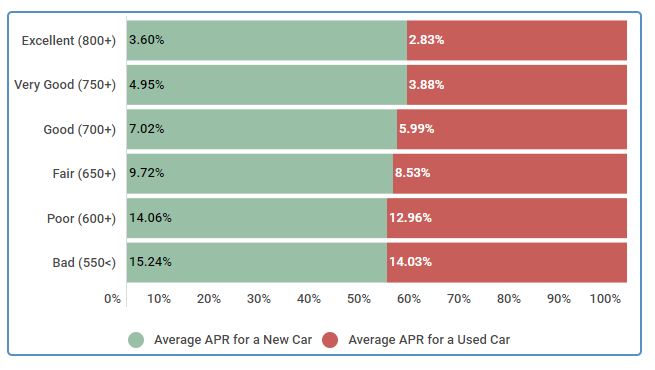

Here's where things get a little less sunshine and rainbows. With a 650 credit score, you're likely going to face a few challenges:

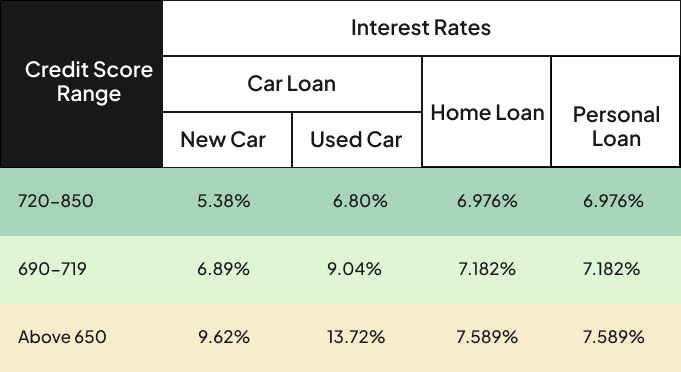

- Higher Interest Rates: This is the big one. Lenders see you as a slightly riskier borrower, so they'll charge you a higher interest rate to compensate. Think of it like this: they're charging you extra because they're afraid you might disappear to a remote island with their money. (Don't do that, please!) Over the life of the loan, this can add up to a significant amount of extra cash.

- Less Favorable Loan Terms: You might not get the longest loan term or the lowest monthly payment. Lenders might offer you shorter repayment periods, which means higher monthly payments. Ouch!

- Limited Selection: You might not qualify for the absolute best financing deals or incentives. Those "0% APR for highly qualified buyers" ads? Yeah, those are probably out of reach for now.

- Bigger Down Payment: Some lenders might require a larger down payment to offset the perceived risk. This is actually a good thing in disguise, since a larger down payment reduces the total amount you have to borrow and pay interest on.

Navigating the Car-Buying Maze with a 650 Credit Score: Survival Tips

Okay, so you know the challenges. Now, let's equip you with the tools you need to survive (and maybe even thrive!) in the car-buying jungle.

- Shop Around for Financing: Don't just accept the first offer you get from the dealership. Get pre-approved for a car loan from your bank or credit union. This gives you a baseline to compare against and puts you in a stronger negotiating position. Knowledge is power!

- Improve Your Credit Score (Even a Little Helps): Before you even start looking at cars, take steps to improve your credit score. Even a small bump can make a difference in the interest rate you qualify for. Pay down credit card debt, dispute any errors on your credit report, and make all your payments on time. Think of it as a credit score makeover!

- Consider a Co-Signer: If you have a friend or family member with excellent credit, ask them to co-sign your loan. This can significantly improve your chances of getting approved for a lower interest rate. Just make sure you understand the risks involved for both parties. Don't want to ruin Thanksgiving dinner over a car loan!

- Be Realistic About Your Budget: Don't fall in love with a car that's way outside your budget. Factor in not only the monthly loan payment but also insurance, gas, maintenance, and other expenses. Remember, that shiny new sports car won't look so shiny when you're eating ramen noodles every night.

- Negotiate, Negotiate, Negotiate!: Don't be afraid to haggle on the price of the car. Dealerships often mark up prices knowing that customers will negotiate. Do your research ahead of time to know the fair market value of the car you're interested in. And remember, silence can be your friend! Sometimes, the first person to speak loses.

- Consider a Used Car: A gently used car can be a great option, especially if you're on a budget. You can often get a better deal on a used car, and it will depreciate less quickly than a new car. Plus, you won't have to worry about that initial "new car smell" fading away. (Okay, some people like that smell. I find it vaguely suspicious.)

- Put Down a Larger Down Payment: The more you can put down, the less you have to borrow, and the less interest you'll pay. It also shows the lender that you're serious about the loan. Plus, you can feel good about yourself knowing you're not starting off with a huge debt hanging over your head.

The Bottom Line: 650 and the Road Ahead

So, is 650 a good credit score to buy a car? It's not the best, but it's certainly not the worst. You can definitely buy a car with a 650 credit score, but you'll need to be prepared to shop around for financing, negotiate aggressively, and potentially pay a higher interest rate. But don't despair! With a little planning and effort, you can drive off the lot in the car of your (reasonable) dreams. Just remember to avoid the temptation of adding that "turbo-charged, self-folding, cupholder warmer" option. Your wallet (and your credit score) will thank you.

And one last piece of advice: always read the fine print! Those contracts can be longer than a Tolstoy novel, but understanding the terms of your loan is crucial. Happy car hunting, and may the odds be ever in your favor!

:max_bytes(150000):strip_icc()/what-credit-score-do-you-need-to-buy-a-car-5181034_final-70360ef3611a47d7af938b7d7a3525ab.png)