Installment Loans For Bad Credit Ohio

Finding an installment loan with bad credit in Ohio can feel daunting, but understanding your options and taking a strategic approach can increase your chances of approval. This article outlines the key steps and considerations involved in securing an installment loan, even with a less-than-perfect credit history.

Assessing Your Credit and Financial Situation

Before you even begin applying for loans, it's crucial to get a clear picture of your credit score and overall financial standing. Knowing where you stand empowers you to target the right lenders and anticipate potential challenges.

Check Your Credit Report

Obtain a copy of your credit report from each of the three major credit bureaus: Experian, Equifax, and TransUnion. You can get a free copy annually from www.annualcreditreport.com. Review the reports carefully for any errors or inaccuracies. Disputing and correcting these errors can improve your credit score.

Must Read

Understand Your Credit Score Range

Your credit score is a numerical representation of your creditworthiness. Generally, scores range from 300 to 850. Here's a typical breakdown:

- Excellent: 750-850

- Good: 700-749

- Fair: 650-699

- Poor: 550-649

- Very Poor: 300-549

Knowing your range helps you understand what type of interest rates and loan terms you might expect.

Calculate Your Debt-to-Income Ratio (DTI)

Lenders use your DTI ratio to assess your ability to repay a loan. Calculate your DTI by dividing your total monthly debt payments (including rent/mortgage, credit card payments, and other loan payments) by your gross monthly income (before taxes). Aim for a DTI below 43% for better loan options. A lower DTI signals less risk to lenders.

Evaluate Your Budget

Create a detailed budget to understand your income and expenses. Identify areas where you can cut back to increase your disposable income and demonstrate your ability to manage debt responsibly. This strengthens your application.

Identifying Lenders Offering Installment Loans for Bad Credit

Not all lenders are created equal. Some specialize in working with individuals who have less-than-perfect credit. It's crucial to research and identify these lenders in Ohio.

Explore Online Lenders

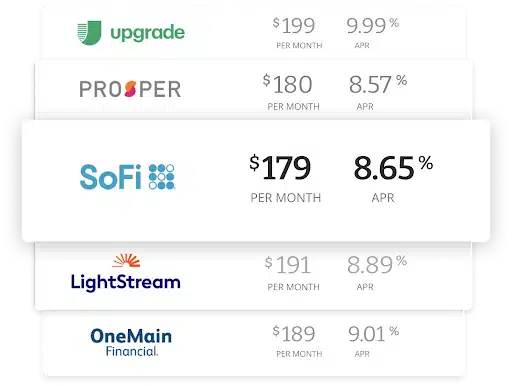

Numerous online lenders cater to borrowers with bad credit. These lenders often have less stringent requirements than traditional banks and credit unions. Some popular options include:

- OppLoans

- Rise Credit

- NetCredit

- OneMain Financial (also has physical branches)

Important Note: Always check the lender's reputation and read reviews before applying. Look for lenders with clear terms and conditions, and be wary of those with excessive fees or predatory lending practices.

Consider Credit Unions

Credit unions are member-owned financial institutions that often offer more favorable terms than banks, especially to members with less-than-perfect credit. Many Ohio credit unions offer installment loans. Research credit unions in your local area and see if you qualify for membership.

Check with Local Banks

While banks typically have stricter credit requirements, it's still worth exploring your options with local banks, especially if you have an existing relationship with them. They might be willing to work with you based on your history.

Compare Interest Rates and Fees

Crucially, compare interest rates and fees from multiple lenders. The APR (Annual Percentage Rate) is the best way to compare the true cost of a loan, as it includes both the interest rate and any fees. Don't just focus on the monthly payment; consider the total cost of the loan over its entire term.

Strengthening Your Loan Application

Even with bad credit, there are steps you can take to improve your chances of approval and secure more favorable loan terms.

Secure a Co-Signer

A co-signer with good credit can significantly improve your application's strength. The co-signer agrees to be responsible for repaying the loan if you default, reducing the lender's risk.

Offer Collateral

Securing the loan with collateral, such as a vehicle or other valuable asset, can also increase your chances of approval. This reduces the lender's risk, as they can seize the collateral if you fail to repay the loan.

Demonstrate a Stable Income

Provide proof of a stable and consistent income. This could include pay stubs, bank statements, or tax returns. Lenders want to see that you have the ability to repay the loan.

Reduce Your Existing Debt

If possible, pay down some of your existing debt before applying for a new loan. This will lower your DTI ratio and make you a more attractive borrower.

Be Prepared to Explain Your Credit History

Be honest and upfront about any past credit problems. Prepare to explain the circumstances surrounding any late payments, defaults, or bankruptcies. Demonstrate that you have taken steps to improve your financial situation.

Understanding Loan Terms and Conditions

Before signing any loan agreement, carefully review all the terms and conditions. Make sure you understand the following:

Interest Rate and APR

Know the exact interest rate and APR. Understand whether the interest rate is fixed or variable.

Loan Term

The loan term is the length of time you have to repay the loan. Shorter terms typically have higher monthly payments but lower total interest paid. Longer terms have lower monthly payments but higher total interest paid.

Fees

Be aware of any fees associated with the loan, such as origination fees, prepayment penalties, or late payment fees.

Repayment Schedule

Understand your repayment schedule, including the due date of each payment and the accepted methods of payment.

Default Penalties

Know the consequences of defaulting on the loan, such as late payment fees, increased interest rates, or legal action.

Managing Your Installment Loan Responsibly

Once you've secured an installment loan, it's crucial to manage it responsibly to rebuild your credit and avoid future financial difficulties.

Make Payments on Time

The most important thing you can do is make all your payments on time. Set up automatic payments to ensure you never miss a due date.

Avoid Taking on More Debt

Avoid taking on additional debt while you're repaying your installment loan. This will help you stay on track and avoid overwhelming yourself.

Monitor Your Credit Report

Continue to monitor your credit report regularly to track your progress and identify any errors or inaccuracies.

Consider Refinancing

As your credit improves, consider refinancing your installment loan to secure a lower interest rate. This can save you money over the long term.

Checklist for Securing an Installment Loan with Bad Credit in Ohio

- Check Your Credit Report: Obtain your credit report from all three major bureaus and dispute any errors.

- Calculate Your DTI Ratio: Determine your debt-to-income ratio to assess your affordability.

- Create a Budget: Understand your income and expenses to demonstrate responsible financial management.

- Research Lenders: Identify online lenders, credit unions, and local banks that offer loans for bad credit.

- Compare Interest Rates and Fees: Compare APRs and loan terms from multiple lenders.

- Gather Documentation: Prepare proof of income, identification, and other required documents.

- Consider a Co-Signer or Collateral: Explore options to strengthen your application.

- Read the Loan Agreement Carefully: Understand all terms and conditions before signing.

- Make Payments on Time: Set up automatic payments to avoid late fees and negative credit impact.

- Monitor Your Credit Report: Track your progress and identify any potential issues.

By following these steps, you can increase your chances of securing an installment loan in Ohio, even with bad credit, and begin rebuilding your financial future.