Immediate Line Of Credit For Bad Credit

Securing an immediate line of credit with bad credit can feel like navigating a maze, but understanding your options and taking strategic steps can improve your chances. This article focuses on actionable strategies to help you access funds quickly, even with a less-than-perfect credit history.

Understanding the Landscape of Bad Credit Lines of Credit

First, let's acknowledge the reality. Lines of credit for individuals with bad credit typically come with higher interest rates and stricter terms than those offered to borrowers with good credit. This is because lenders perceive you as a higher risk. However, options do exist.

Here's a breakdown of common avenues and considerations:

Must Read

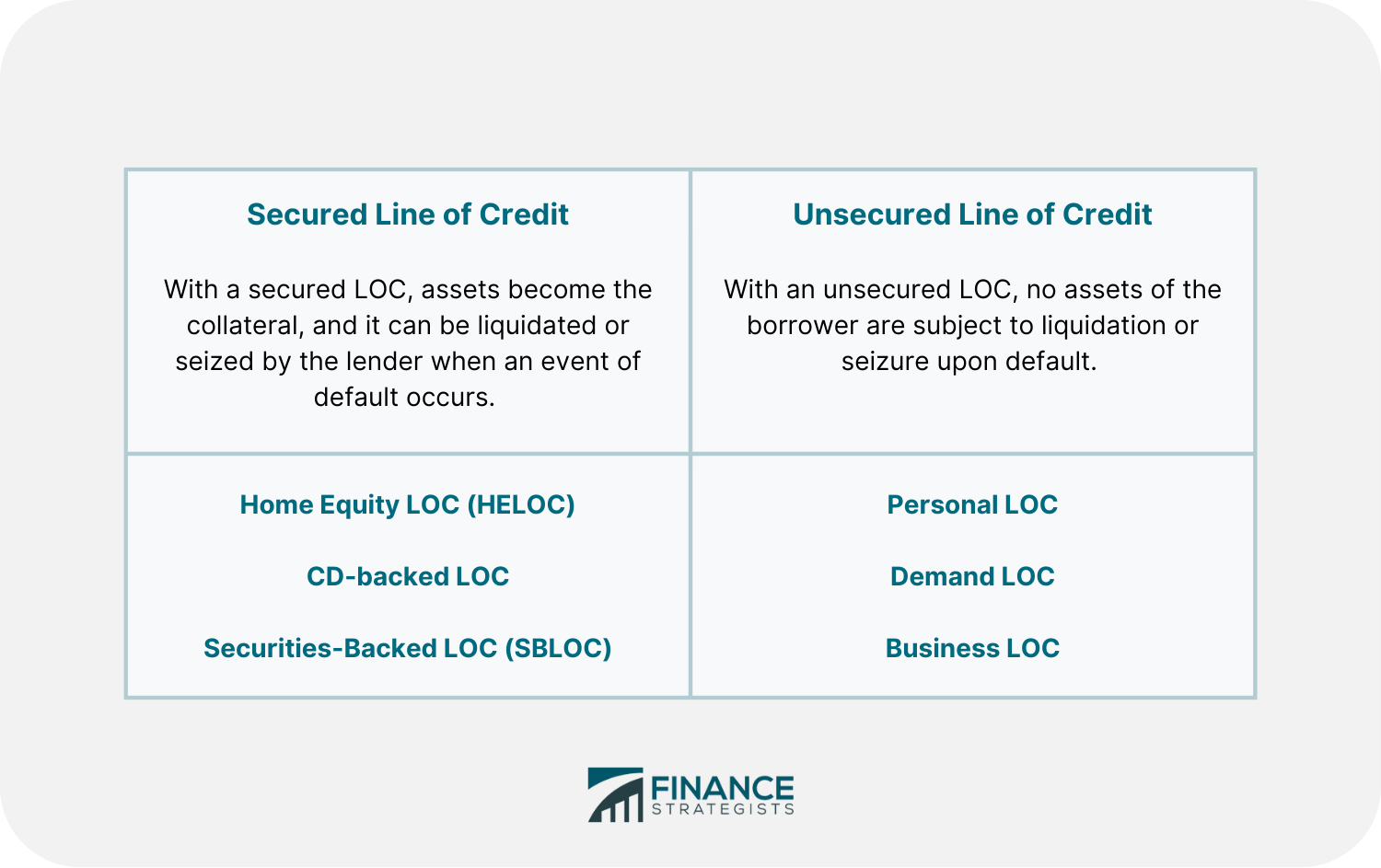

Secured Lines of Credit

A secured line of credit is backed by an asset, such as a savings account or a certificate of deposit (CD). This collateral reduces the lender's risk, making them more willing to extend credit to someone with a lower credit score.

Practical Tip: If you have savings you can afford to tie up for a period, a secured line of credit can be a good way to access funds and potentially rebuild your credit history through responsible usage. However, be aware that the asset is at risk if you default on your payments.

The credit limit is usually proportional to the value of the asset securing it. For example, a $1,000 CD might secure a $750 line of credit.

Credit Builder Loans

While not a traditional line of credit, credit builder loans can be a valuable tool. In this scenario, you borrow a small amount of money, but instead of receiving the funds upfront, the lender places them in a secured account. You then make regular payments over a set period. Once you've repaid the loan, you receive the funds. The primary benefit is the positive credit reporting to credit bureaus, helping you improve your score.

Practical Tip: Think of this as a forced savings account that simultaneously boosts your credit. The money is yours in the end, but the structured repayment schedule builds a positive payment history. Many community banks and credit unions offer these types of loans.

Personal Loans for Bad Credit

While personal loans are installment loans (meaning you receive a lump sum and repay it over time), some lenders specialize in offering loans to individuals with bad credit. These loans often come with higher interest rates and fees, but they can provide access to funds when a line of credit isn't readily available.

Practical Tip: Carefully compare interest rates, fees, and repayment terms from multiple lenders before committing to a personal loan. Look for lenders who report to all three major credit bureaus (Experian, Equifax, and TransUnion). Always prioritize responsible borrowing and repayment.

Pawn Shops

Pawn shops offer short-term, secured loans. You bring in an item of value as collateral (jewelry, electronics, etc.), and the pawn shop gives you a loan based on the item's estimated worth. If you repay the loan within the agreed-upon timeframe (typically 30-90 days) with interest, you get your item back. If you don't repay, the pawn shop keeps the item.

Practical Tip: Pawn shops should be used only as a last resort. Interest rates are typically very high, and you risk permanently losing your valuable belongings if you can't repay the loan.

Payday Loans (Avoid If Possible)

Payday loans are short-term, high-interest loans typically due on your next payday. These should be avoided if at all possible. The extremely high interest rates and short repayment terms can easily trap borrowers in a cycle of debt.

Practical Tip: Explore all other options before considering a payday loan. The potential for financial hardship far outweighs any perceived benefit.

Improving Your Chances of Approval

Even with bad credit, you can take steps to increase your chances of securing a line of credit or a loan:

- Check Your Credit Report: Obtain a copy of your credit report from all three major credit bureaus and dispute any errors. Correcting inaccuracies can improve your credit score.

- Reduce Your Debt-to-Income Ratio (DTI): DTI is the percentage of your gross monthly income that goes towards debt payments. Lowering your DTI makes you a more attractive borrower. You can achieve this by paying down existing debt or increasing your income.

- Consider a Co-signer: A co-signer with good credit can vouch for your ability to repay the loan, significantly increasing your chances of approval. However, make sure your co-signer understands the risks involved. They are legally responsible for the debt if you default.

- Demonstrate Stable Income: Provide proof of stable employment and income to demonstrate your ability to repay the debt.

- Apply Strategically: Don't apply for multiple lines of credit or loans at the same time. Each application triggers a hard credit inquiry, which can negatively impact your credit score. Focus on the options that are most likely to approve you based on your current credit profile.

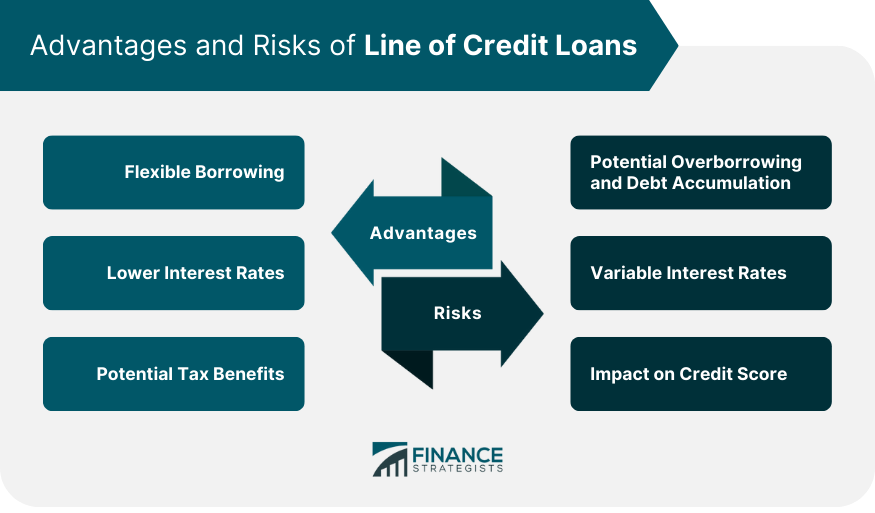

Using a Line of Credit Responsibly

Once you've secured a line of credit, responsible usage is crucial for rebuilding your credit and avoiding further financial difficulties:

- Make Payments on Time: Payment history is the most important factor in your credit score. Always pay your bills on time, every time.

- Keep Your Credit Utilization Low: Credit utilization is the amount of credit you're using compared to your total credit limit. Aim to keep your utilization below 30%. For example, if you have a $1,000 credit line, try to keep your balance below $300.

- Avoid Cash Advances: Cash advances typically come with high fees and interest rates. Only use them in emergencies.

- Monitor Your Credit Report Regularly: Keep an eye on your credit report to ensure that your payments are being reported correctly and to identify any potential errors or fraudulent activity.

Remember: A line of credit is a financial tool, not a solution to underlying financial problems. If you're struggling with debt, consider seeking guidance from a credit counselor.

Checklist: Immediate Line of Credit for Bad Credit

Use this checklist to guide your search and application process:

- Assess Your Needs: Determine how much credit you need and for what purpose.

- Check Your Credit Report: Obtain your report from all three major bureaus and dispute any errors.

- Explore Secured Lines of Credit: If you have assets, this is often the easiest route.

- Research Credit Builder Loans: A great option for rebuilding credit while saving money.

- Compare Personal Loans (Bad Credit Lenders): If a lump sum is needed, compare offers carefully.

- Consider a Co-signer: If possible, a co-signer can improve your chances.

- Avoid Payday Loans: Explore all other options first.

- Improve DTI: Reduce debt or increase income.

- Apply Strategically: Don't apply for too many options at once.

- Use Credit Responsibly: Make on-time payments and keep utilization low.

By understanding your options, taking proactive steps to improve your credit profile, and using credit responsibly, you can navigate the challenges of securing a line of credit with bad credit and work towards a brighter financial future.