How To Write A Check For 70 Dollars

Writing a check for seventy dollars appears, on the surface, to be a simple task. However, understanding the proper execution of this seemingly mundane act reveals underlying principles of financial literacy, security, and trust within a system predicated on written instruments. This article will dissect the process of writing a check for $70, examining its component parts, their historical context, and the broader implications of accuracy and legibility in financial transactions.

Causes: The Components of a Check

The act of writing a check is comprised of several distinct actions, each serving a crucial purpose. Failure to execute any one of these steps correctly can lead to complications, delays, or even financial loss. These components act as causes leading to the ultimate successful processing of the check.

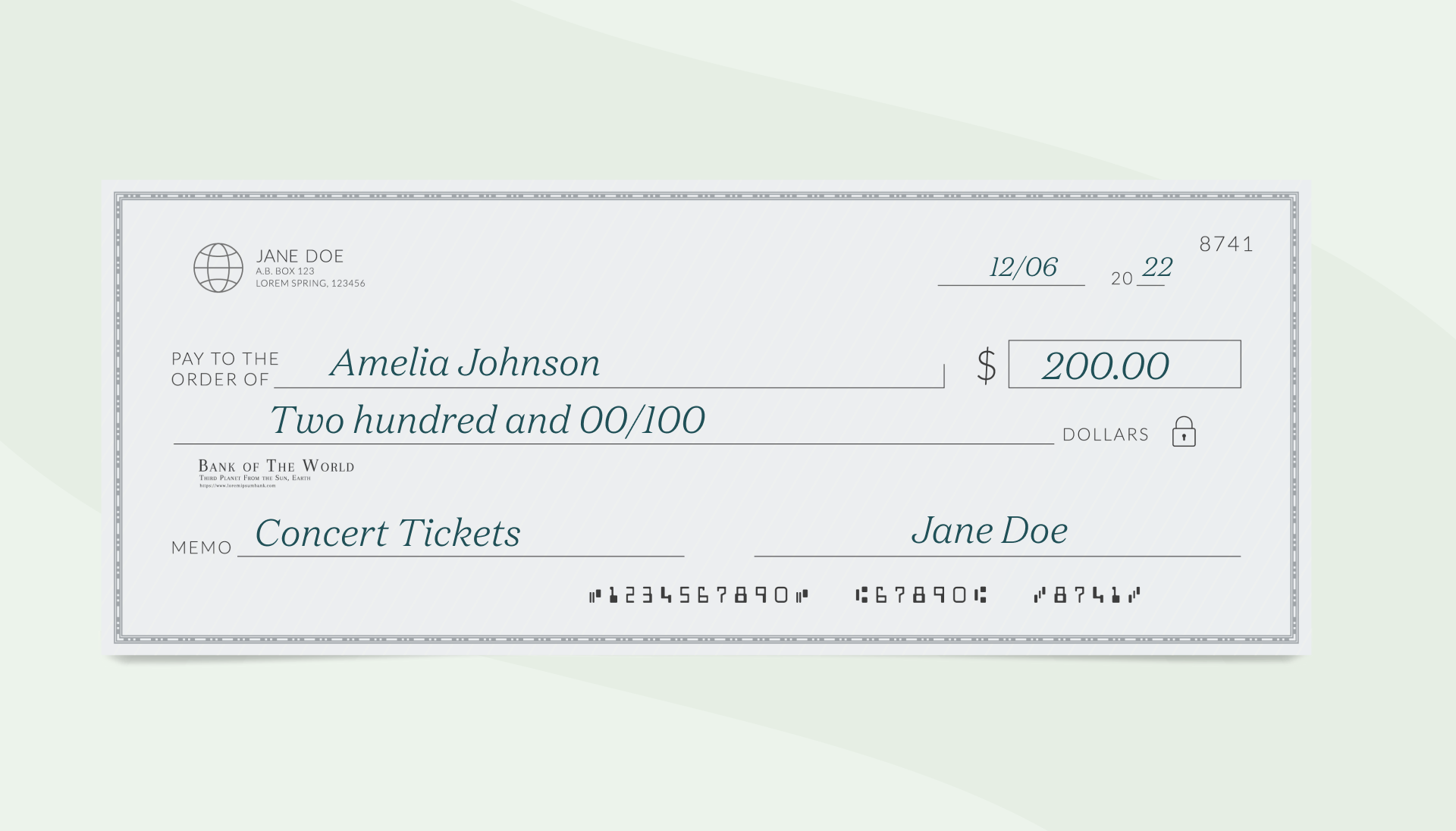

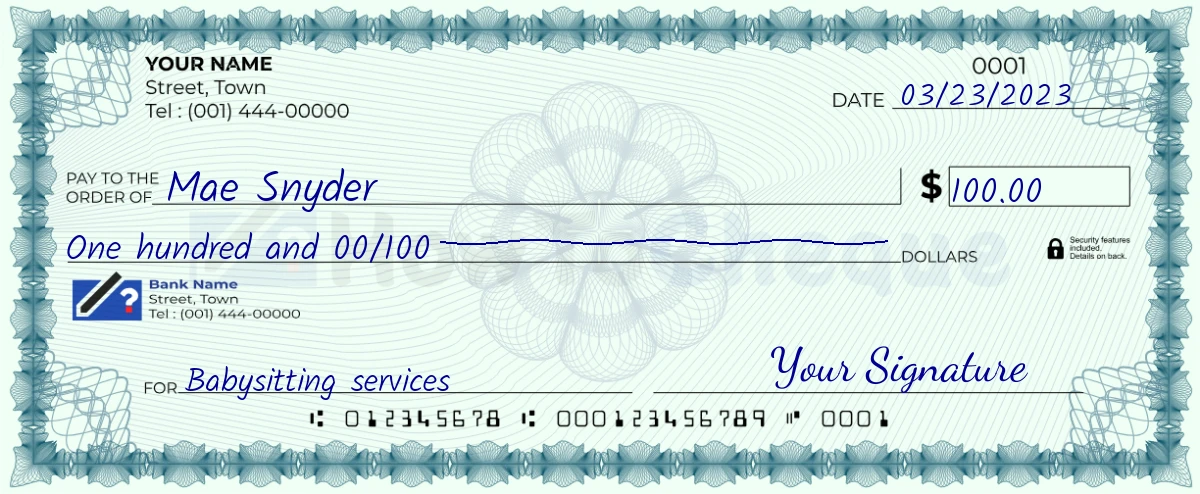

Date

The date is arguably the first, and most straightforward, element. Writing the date correctly, using the proper format (MM/DD/YYYY in the United States), is essential for banks to process the check accurately and to determine its validity. Post-dating or anti-dating a check can have legal ramifications, particularly regarding the enforcement of payment.

Must Read

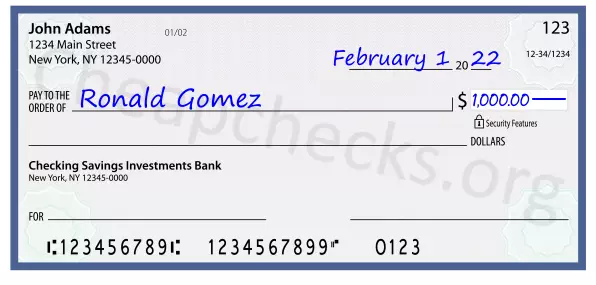

Payee

The "Pay to the Order Of" line dictates who will receive the funds. Accuracy is paramount here. Misspelled names or unclear handwriting can cause delays or even rejection by the bank. The intention is to clearly identify the intended recipient, preventing fraudulent endorsement and ensuring the funds reach the correct party. Imagine, for example, accidentally writing "Smith John" instead of "John Smith"; while seemingly trivial, this discrepancy could allow an unscrupulous individual to claim the funds if bank policies aren't strictly followed.

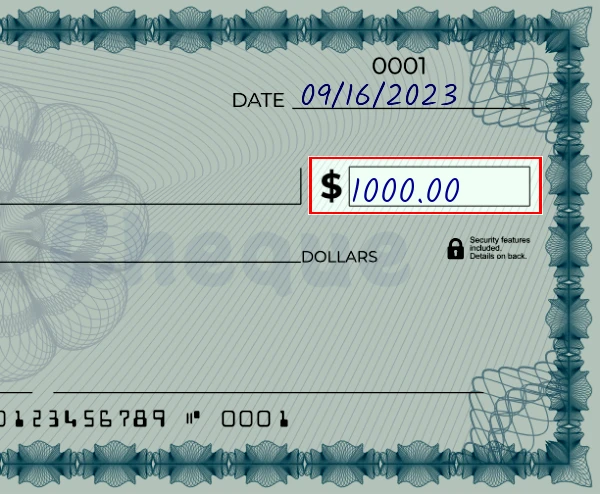

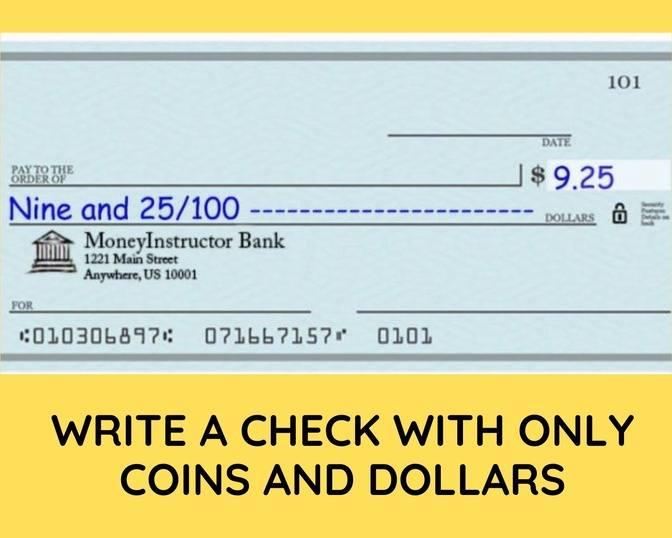

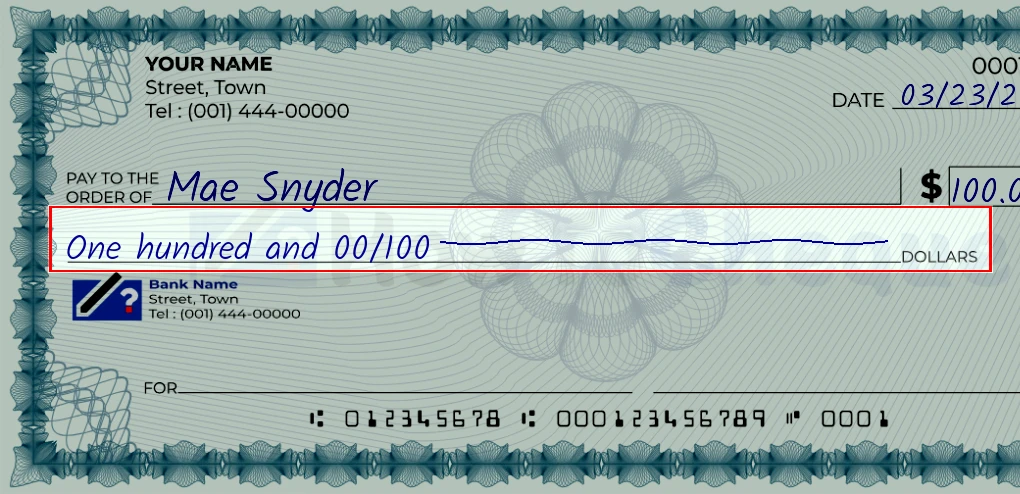

Numerical Amount

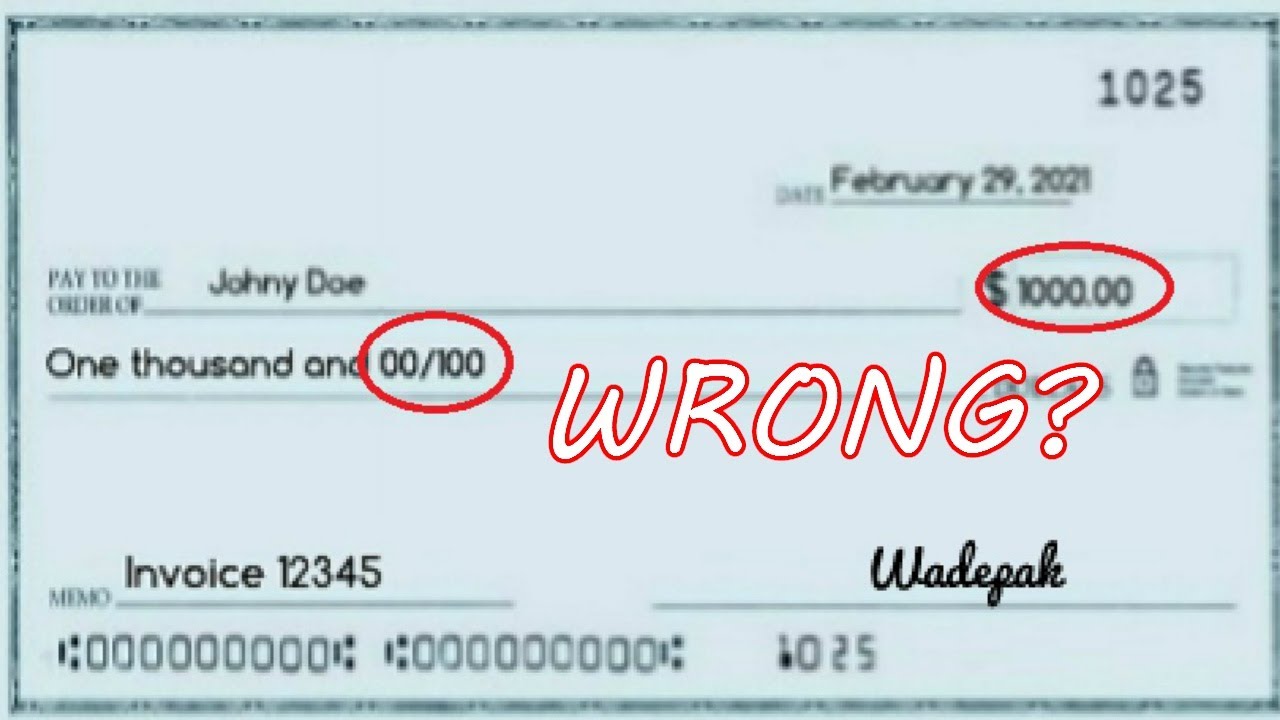

The small box designated for the numerical amount is where the value of the check is clearly stated. Writing "$70.00" is the standard practice. The inclusion of ".00" even for whole dollar amounts reinforces the absence of cents, preventing any ambiguity or potential for alteration. Care should be taken to position the dollar sign closely to the number to avoid someone adding a "1" before the "70," effectively changing the amount to $170.00.

Written Amount

The line dedicated to writing the amount in words is perhaps the most crucial safeguard against fraud. Writing "Seventy and 00/100" provides an unambiguous representation of the intended value. The inclusion of "and 00/100" explicitly clarifies that there are no cents involved. This written representation acts as a cross-reference to the numerical amount; in cases of discrepancy, the written amount generally takes precedence. The Uniform Commercial Code (UCC), which governs commercial transactions in the United States, addresses these types of discrepancies. For example, UCC § 3-114 addresses situations where words and figures differ, stating that words control figures unless the words are ambiguous.

Signature

The signature is the authorization. Without a valid signature matching the account holder's on file, the check is invalid. The signature should be legible and consistent with previous signatures. A forged signature is a serious crime and can lead to legal repercussions. Banks employ various security measures, including signature verification systems, to detect fraudulent checks. The proliferation of check fraud in the late 20th century, reaching an estimated $10 billion annually in the US, prompted banks to invest heavily in these systems.

Memo (Optional)

The memo line is for personal reference. While not legally binding, it provides context for the payment. Writing "Rent," "Utilities," or "Birthday Gift" can help the payer track expenses and reconcile their account. It can also provide helpful information to the payee, especially for businesses managing multiple payments. Although optional, its presence clarifies the check's purpose.

Effects: Consequences of Improper Execution

The effects of not properly writing a check for seventy dollars can range from minor inconveniences to significant financial repercussions. These consequences stem directly from the inaccuracies or omissions in the check's components.

Delayed Processing

Illegible handwriting, misspelled names, or incorrect dates can all lead to delayed processing. Banks may need to contact the payer or payee for clarification, which can hold up the transaction. In some cases, the check may be temporarily rejected until the issue is resolved. This delay can be problematic if the payment is time-sensitive, such as rent or a bill with a late fee.

Rejection

More severe errors, such as a missing signature, a significant discrepancy between the numerical and written amounts, or a mismatch between the payee's name and the endorsement, can result in the check being rejected outright. The payee will not receive the funds, and the payer may incur fees from their bank for a returned check.

Fraud

A poorly written check is vulnerable to fraud. If the numerical or written amount is easily altered, a dishonest individual could change the value of the check. Similarly, an ambiguous payee name could allow someone other than the intended recipient to cash the check. This highlights the importance of careful handwriting and attention to detail.

Financial Loss

In the worst-case scenario, a poorly written check can lead to financial loss. If a fraudulent check is cashed, the account holder may be liable for the loss, depending on the circumstances and the bank's policies. It's important to report any suspected fraud to the bank immediately to mitigate potential losses.

Implications: Broader Significance

The simple act of writing a check for seventy dollars has broader implications beyond the immediate transaction. It reflects on the individual's financial literacy, their understanding of the financial system, and their responsibility as a participant in that system.

Financial Literacy

Mastering the mechanics of check writing is a fundamental aspect of financial literacy. It demonstrates an understanding of how checks function as a form of payment, the importance of accuracy and security, and the potential risks associated with negligence. Check writing, although increasingly less common with the rise of digital payment methods, still serves as a valuable learning tool for understanding financial transactions.

Trust and Accountability

The acceptance of a check relies on trust. The payee trusts that the payer has sufficient funds in their account and that the check is valid. The bank trusts that the payer has authorized the payment. This trust is underpinned by a system of legal and financial accountability. When someone writes a bad check, they are violating that trust and potentially facing legal consequences.

Historical Context

Checks have a rich history, dating back centuries. Their evolution reflects the development of banking systems and the changing nature of commerce. Understanding the historical context of checks provides a deeper appreciation for their role in facilitating economic activity. Originally, checks were largely handwritten documents, and standardization evolved over time. Today's checks contain security features and are often processed electronically, but the underlying principles remain the same.

The Decline of Check Usage

While check usage is declining, understanding the process remains relevant. According to the Federal Reserve Payments Study, check payments accounted for only a small percentage of noncash payments in recent years, with electronic payments (credit cards, debit cards, and ACH transfers) dominating the landscape. However, checks are still used in certain situations, particularly for payments to individuals or small businesses that may not accept other forms of payment. The ongoing decline in check usage underscores the importance of adapting to new payment technologies, but also highlights the continued need for basic financial literacy skills.

In conclusion, writing a check for seventy dollars is more than just filling out a form. It involves a complex interplay of legal requirements, trust, and financial responsibility. While the digital age offers alternative payment methods, understanding the principles behind check writing remains a valuable skill for anyone navigating the financial world. Even as checks become less prevalent, the fundamental concepts of financial accuracy, security, and accountability that they embody remain essential for responsible financial management.

:max_bytes(150000):strip_icc()/how-to-write-cents-on-a-check-315355-final-5be57b294a9044788686c3f54cc35d2d.jpg)