How To Start A New Year In Quickbooks

Closing the Books: A Quickbooks New Year Guide

The end of the fiscal year requires specific procedures within Quickbooks to ensure accurate financial reporting and a smooth transition into the new year. Here's a step-by-step guide.

Reviewing and Reconciling Accounts

Prior to closing the year, perform a comprehensive review. Reconcile all bank accounts, credit card accounts, and other balance sheet accounts. This confirms that your records match external statements. Unreconciled differences should be investigated and resolved.

Ensure accuracy in your financial data through meticulous reconciliation.

Generate and examine key financial reports, including the Balance Sheet, Profit and Loss (Income Statement), and Statement of Cash Flows. Compare these reports to previous periods to identify any anomalies or unexpected fluctuations. Address any discrepancies before proceeding.

Must Read

Making Adjusting Entries

Adjusting entries are necessary to correct errors and ensure that revenues and expenses are recorded in the proper accounting period. Common adjusting entries include accruals, deferrals, and depreciation. Consult with an accountant to identify the necessary adjustments for your business.

Accrue expenses incurred but not yet paid (e.g., utilities, salaries). Defer revenue received but not yet earned (e.g., prepaid services). Record depreciation expense for fixed assets.

Performing Year-End Inventory Reconciliation

If you manage inventory, conduct a physical inventory count and reconcile it with your Quickbooks records. Investigate any discrepancies between the physical count and the recorded inventory levels. Make necessary adjustments to reflect the accurate inventory on hand.

Calculate the Cost of Goods Sold (COGS) based on your inventory valuation method (e.g., FIFO, LIFO, weighted average). Review inventory obsolescence and consider writing down obsolete inventory to its net realizable value.

Running Year-End Reports

Generate the following essential year-end reports:

- Balance Sheet: Provides a snapshot of your assets, liabilities, and equity at the end of the year.

- Profit and Loss (Income Statement): Summarizes your revenues, expenses, and net income or loss for the year.

- Statement of Cash Flows: Reports the movement of cash into and out of your business during the year.

- Trial Balance: Lists all general ledger accounts and their debit and credit balances.

- General Ledger: A detailed record of all transactions affecting each account.

- Customer and Vendor Balance Detail Reports: Shows outstanding balances for each customer and vendor.

Archive these reports in a secure location for future reference and audit purposes. You may need to provide these reports to your accountant or tax preparer.

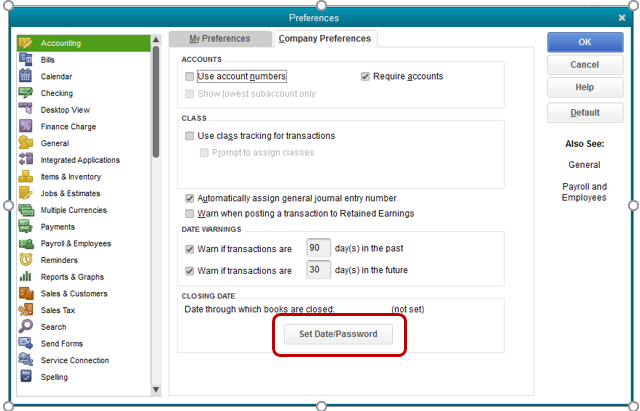

Closing the Year in Quickbooks Desktop

In Quickbooks Desktop, the process involves setting a closing date and password.

- Go to the Company menu.

- Select Set Closing Date.

- Enter the last day of your fiscal year as the closing date.

- Enter and confirm a password. This password will prevent unauthorized users from making changes to transactions prior to the closing date.

- Click OK.

Note the password carefully. Losing it can complicate making legitimate corrections to prior-year data.

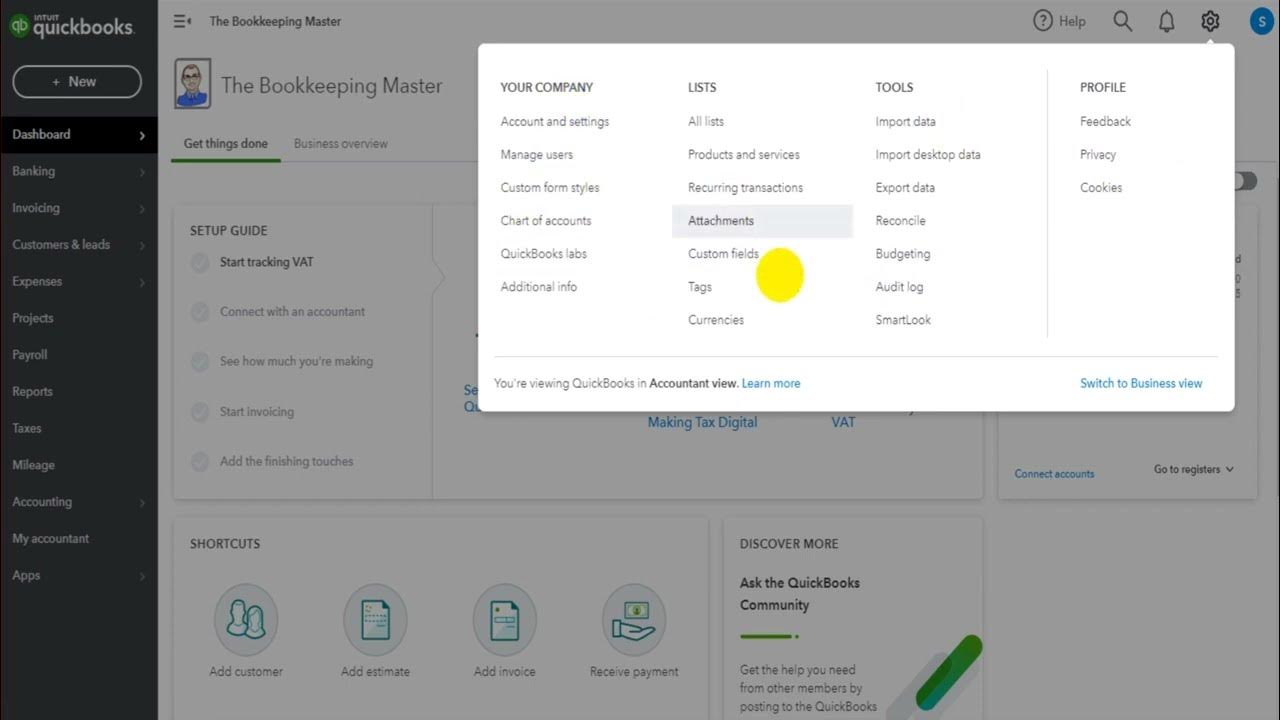

Closing the Year in Quickbooks Online

Quickbooks Online uses a similar process but is found in a different location.

- Click the Gear icon in the top right corner.

- Select Account and Settings.

- Go to the Advanced tab.

- In the Accounting section, click Edit.

- Turn on Close the books.

- Enter the closing date.

- Enter a password (optional but recommended).

- Click Save and then Done.

The password provides an extra layer of security, preventing accidental or unauthorized changes to closed periods.

Opening a New Fiscal Year

Once the previous year is closed, you can begin recording transactions for the new fiscal year. Quickbooks automatically creates a new fiscal year based on your company settings. No manual creation is necessary.

Maintaining Audit Trails

Quickbooks maintains an audit trail of all transactions and changes made to your data. This audit trail is a valuable resource for tracking down errors and identifying potential fraud. Regularly review the audit trail to ensure the integrity of your financial data.

Access the audit trail from the Reports Center or by searching for "Audit Trail" in Quickbooks.

Handling Prior-Year Adjustments

Even after closing the year, you may need to make adjustments to prior-year transactions. If you discover an error or omission, you can unlock the closed period by entering the closing date password.

After making the necessary adjustments, re-close the year to prevent further changes. Document the reasons for the adjustment and keep a record of the changes made.

Consulting with a Professional

While this guide provides a general overview of the year-end closing process in Quickbooks, it is not a substitute for professional advice. Consult with a qualified accountant or bookkeeper to ensure that you are following the proper procedures for your specific business.

A professional can help you identify and correct errors, optimize your accounting practices, and ensure compliance with tax regulations.

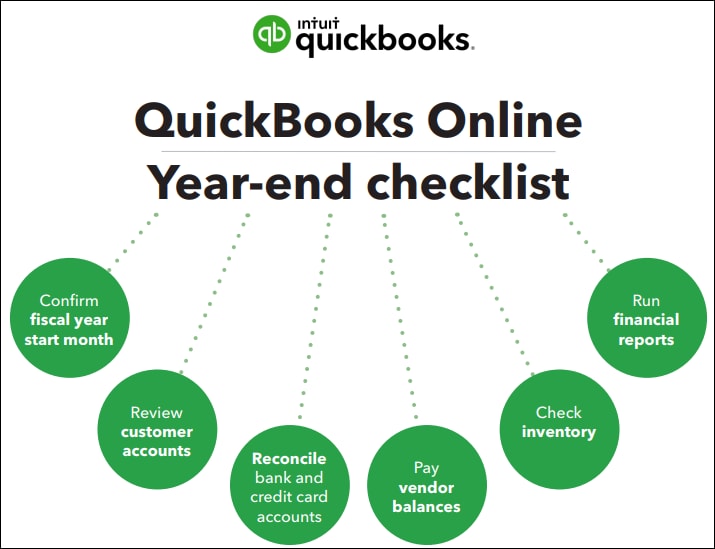

Key Takeaways for a Smooth New Year Transition

Closing the books in Quickbooks is crucial. It ensures accurate financial records for reporting and analysis. Here are the key actions to consider:

- Reconcile all accounts meticulously.

- Run and review key financial reports.

- Make all necessary adjusting entries.

- Set a closing date and password to prevent unauthorized changes.

- Maintain a detailed audit trail.

- Consult with a professional for expert guidance.

By following these steps, you can start the new year with confidence, knowing that your financial records are accurate and reliable.