Recording a 1031 exchange in your accounting records necessitates a meticulous approach to ensure compliance and accurate financial representation. A 1031 exchange, also known as a like-kind exchange, allows investors to defer capital gains taxes when selling an investment property and reinvesting the proceeds into a similar property. The journal entries reflect the transfer of assets and liabilities, the deferral of gains, and the associated costs.

Initial Sale of the Old Property

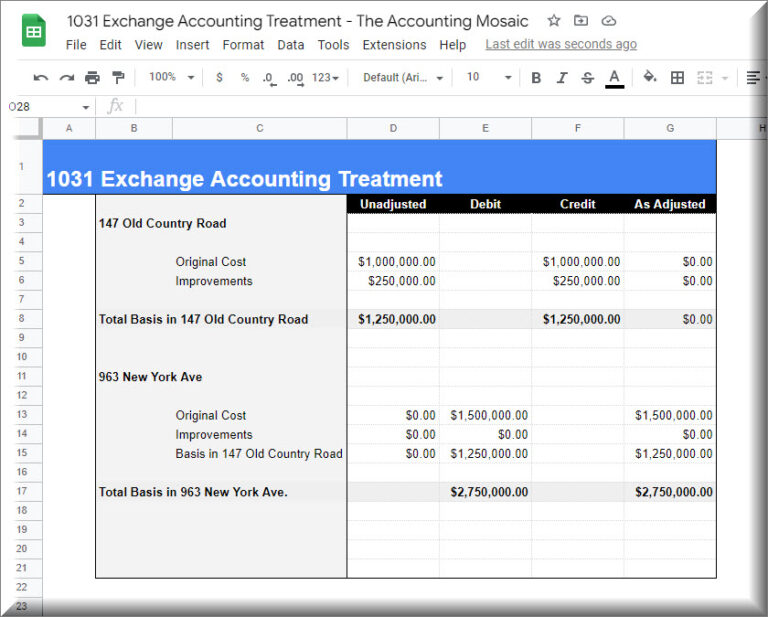

The first step involves recording the sale of the relinquished property. This includes accounting for the removal of the asset from your books, recognizing any cash received, and carefully managing the deferred gain.

Debiting Cash

When you sell the old property, you'll typically receive cash. The amount received should be debited to the cash account. This increases the balance of your cash account, reflecting the inflow of funds from the sale.

The original cost of the property being sold must be removed from your accounting records. This is achieved by crediting the relevant asset account, typically "Investment Property" or "Land and Buildings." This reduces the balance of the asset account, reflecting the disposal of the property.

For example, assuming the original cost was $300,000:

Credit: Investment Property - $300,000

Removing Accumulated Depreciation (Debit)

If the property has been depreciated over time, the accumulated depreciation must also be removed from your books. This is done by debiting the "Accumulated Depreciation" account. This decreases the balance of the accumulated depreciation account, offsetting the accumulated depreciation related to the sold property.

For example, if the accumulated depreciation was $50,000:

Debit: Accumulated Depreciation - $50,000

Recording the Deferred Gain (Credit)

The difference between the selling price (adjusted for expenses) and the property's book value (original cost less accumulated depreciation) represents the gain. However, in a 1031 exchange, this gain is not immediately recognized for tax purposes; it is deferred. A deferred gain liability account is credited to acknowledge this future obligation.

IRS 1031 Exchange Rules: Requirements, Timeline, and Guidelines - YouTube

In our example, the selling price was $500,000, the original cost was $300,000, and the accumulated depreciation was $50,000. Therefore, the gain before considering exchange expenses is $500,000 - ($300,000 - $50,000) = $250,000.

Therefore:

Credit: Deferred Gain on 1031 Exchange - $250,000

Purchase of the New Property

The next set of journal entries focuses on recording the acquisition of the replacement property. This involves accounting for the new asset, any additional cash paid, and the transfer of the deferred gain.

Debiting the New Property

When the replacement property is acquired, it's recorded as an asset on your balance sheet. The cost of the new property, which includes the purchase price plus any eligible acquisition costs, is debited to the appropriate asset account (e.g., "Investment Property").

For example, if the new property costs $600,000:

Debit: Investment Property (New) - $600,000

Crediting Cash (If Applicable)

If the proceeds from the sale of the old property don't fully cover the cost of the new property, you'll need to pay additional cash. This outflow of cash is recorded by crediting the cash account.

In our ongoing example, the original property was sold for $500,000, and the new property cost $600,000. This means you paid an additional $100,000 in cash:

How To Record 1031 Exchange On Tax Return? - CountyOffice.org - YouTube

Credit: Cash - $100,000

Reducing the Deferred Gain Liability (Debit)

With the purchase of the replacement property, a portion or all of the deferred gain from the original sale is now being reinvested. The deferred gain liability account is debited to reduce its balance. This reflects the fact that the gain is still not being recognized, but its deferred status is being carried over to the new property.

In our example, the entire $250,000 gain is deferred to the new property:

Debit: Deferred Gain on 1031 Exchange - $250,000

Recording Exchange Expenses

Expenses directly related to the 1031 exchange, such as qualified intermediary fees, legal fees, and appraisal fees, are treated differently than typical expenses. These costs are typically added to the basis of the new property and reduce the amount of the deferred gain.

Debiting the New Property or Creating a Separate Asset Account

Exchange expenses can either be added directly to the cost basis of the new property or recorded in a separate asset account. The choice depends on the level of detail you want to maintain in your accounting records. Adding directly to the new property account simplifies record-keeping but may make it harder to track specific exchange costs later.

For example, if exchange expenses totaled $10,000:

The payment of these expenses results in a cash outflow, which is recorded by crediting the cash account.

Example of posting journal entries to Quickbooks - YouTube

Continuing the example:

Credit: Cash - $10,000

Adjusting the Deferred Gain (If Necessary)

If the exchange expenses are not added directly to the basis of the new property (and instead are tracked separately), there may be a need to adjust the deferred gain. This occurs if the expenses reduce the net proceeds available for reinvestment, which could potentially trigger some tax liability. This is a complex area, and professional advice is strongly recommended.

Example Summary of Entries

To consolidate these journal entries:

Sale of Old Property:

Debit: Cash - $500,000

Debit: Accumulated Depreciation - $50,000

Credit: Investment Property (Old) - $300,000

Credit: Deferred Gain on 1031 Exchange - $250,000

How To Do A 1031 Exchange With A Rental Property - YouTube

Accurate recording of 1031 exchange journal entries is crucial for several reasons. First, it ensures compliance with tax regulations, demonstrating that the exchange was properly executed and that capital gains taxes have been appropriately deferred. Second, it provides a clear audit trail for future tax audits. Third, it provides a reliable accounting of the property's adjusted basis, which is essential for calculating depreciation and any future capital gains or losses upon a subsequent sale. Finally, it is important for accurate financial reporting and decision-making.

The complexities of 1031 exchanges often necessitate the guidance of a qualified tax advisor or accountant. They can provide tailored advice based on your specific circumstances and ensure that your journal entries accurately reflect the exchange and comply with all applicable regulations.

![How To Do A 1031 Exchange [with Rental Property] - YouTube](https://i.ytimg.com/vi/VCM16kRmJEs/maxresdefault.jpg)