How To Get Out Of Payday Loan Cycle

Alright, gather 'round, friends! Let's talk about something nobody really wants to talk about, but affects way too many of us: the dreaded payday loan cycle. It's like that one houseplant you keep meaning to repot, but never quite get around to, except instead of wilting leaves, it's your bank account that's slowly withering. Don't worry, though! We're going to get you out of this financial swamp, one (slightly sarcastic) step at a time.

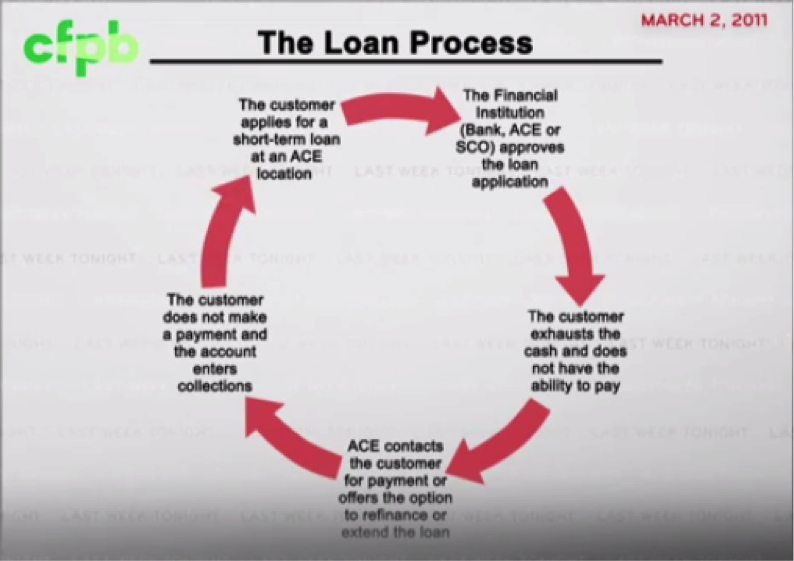

Imagine this: you're strapped for cash, your car decided to throw a tantrum and now needs a new carburetor (or whatever fancy thing modern cars need these days). Your next paycheck is still a week away, and payday loans, with their siren song of "quick cash," seem like the only option. You take out a loan, relieved. But then... BAM! Fees. Interest rates that could make a loan shark blush. Before you know it, you're borrowing again just to pay off the first loan. Sound familiar? You're officially on the payday loan merry-go-round, and nobody's handing out free cotton candy.

Step 1: Admit You Have a Problem (and Maybe Blame the Shiny Advertisements)

Okay, this isn't exactly like a 12-step program, but acknowledging the issue is crucial. Stop telling yourself, "Oh, it's just this one time!" or "I'll totally pay it back next week!" (Famous last words, right?). Be honest with yourself: you're stuck in a cycle, and denial is only going to make the alligators in that swamp bigger and hungrier. You’re not a financial failure, you’re just human! We all make mistakes. Blame the manipulative marketing. Blame the patriarchy! Just admit it, and let's move on.

Must Read

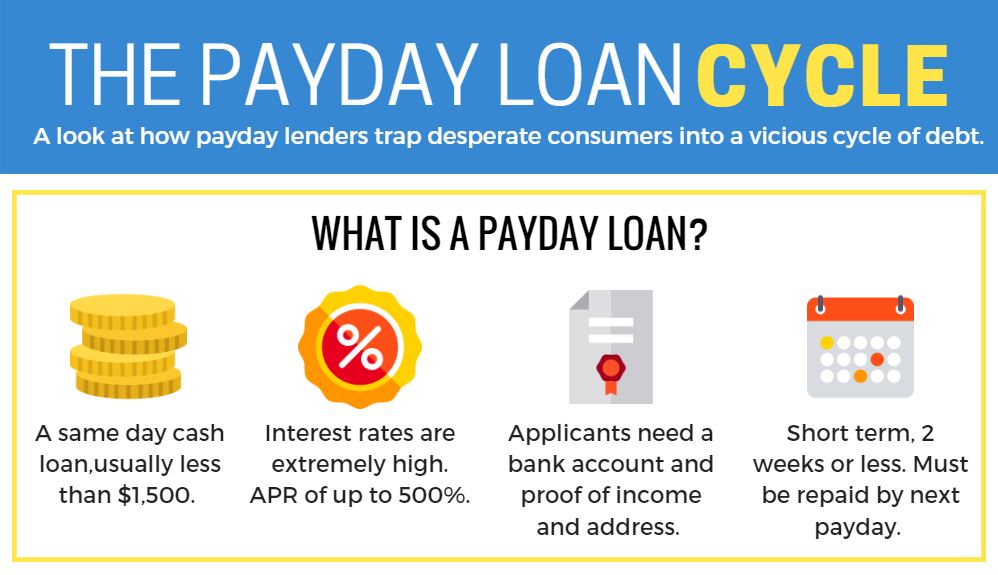

Fun fact: Did you know that the average payday loan borrower takes out eight loans per year? That's like having a birthday every six weeks, except instead of cake, you get debt. Yuck.

Step 2: Stop Digging! (Seriously, Put Down the Shovel!)

This one's a no-brainer, but it needs to be said: stop taking out new payday loans. I know, I know, easier said than done. It's like telling a chocolate addict to stay away from the candy aisle. But you have to resist the urge. Every new loan is just adding fuel to the fire. You’re just creating a bigger problem that you have to deal with in the long run. Think of it as temporary relief but longer pain.

Instead of reaching for another loan, try these:

- Raid your piggy bank: Empty that jar of loose change. You'd be surprised how much it adds up!

- Sell something you don't need: That exercise bike you haven't touched since January? The Beanie Baby collection your mom gave you? Time to say goodbye! Sites like eBay, Craigslist, and Facebook Marketplace are your friends.

- Ask for help (gulp): Talking to a trusted friend or family member can be tough, but sometimes, a small loan from someone who cares can make all the difference. Be sure to agree on a repayment plan and stick to it!

Step 3: Face the Music (and the Interest Rates)

Alright, deep breath. It's time to figure out exactly how much you owe and what those horrifying interest rates are. Gather all your loan documents (or log into your online accounts) and write everything down. Seeing it all in black and white can be scary, but it's the first step towards taking control. Think of it as staring Medusa in the face, but instead of turning to stone, you just get a really bad headache. Then, get a plan to fight Medusa…err…pay off the debt.

Pro Tip: Most payday loans have ridiculously high APRs (Annual Percentage Rates) – sometimes exceeding 400%! That’s basically highway robbery in broad daylight. Knowing this can fuel your determination to escape this financial trap.

Step 4: Strategize Like a Chess Grandmaster (or at Least Play a Game of Checkers)

Now that you know what you're up against, it's time to develop a repayment strategy. Here are a few options:

- The "Avalanche" Method: Focus on paying off the loan with the highest interest rate first, while making minimum payments on the others. This will save you the most money in the long run. Imagine it as strategically eliminating the most dangerous enemy first.

- The "Snowball" Method: Pay off the smallest loan first, regardless of interest rate. This gives you a quick win and boosts your motivation. It's like clearing out the small goblins before tackling the dragon.

- Debt Consolidation Loan: Get a new loan with a lower interest rate and use it to pay off all your payday loans. This simplifies your payments and can save you a ton of money. Think of it as trading in your rusty old sword for a shiny new one. Be cautious! Make sure you qualify and can afford the payments on the new loan.

- Negotiate with the Lender: Believe it or not, some payday lenders are willing to work with you. Explain your situation and ask if they can offer a lower interest rate or a payment plan. The worst they can say is no, and you might be surprised at what you can achieve. It's like haggling at a flea market – you never know what deals you can find!

Step 5: Budget Like a Boss (Even If You Feel Like a Broke Intern)

Creating a budget is essential for getting out of the payday loan cycle and staying out. Track your income and expenses, and identify areas where you can cut back. Do you really need that daily latte? Can you brown-bag your lunch instead of eating out? Every little bit helps. A budget isn’t a restriction, it's a guide to help you achieve your financial goals. Consider using budgeting apps or spreadsheets. There are tons of free resources available online.

:max_bytes(150000):strip_icc()/how-to-get-a-loan-315510_V1-e8212e1a3dfe43358308f689cf51a284.png)

Surprising fact: People who budget are more likely to achieve their financial goals, including getting out of debt. It's like having a map to reach your destination instead of wandering aimlessly through the financial wilderness.

Step 6: Build an Emergency Fund (So You Don't End Up in the Same Mess Again)

Once you're out of the payday loan cycle, it's crucial to build an emergency fund. This is a savings account specifically for unexpected expenses, like that car repair or a medical bill. Having an emergency fund can prevent you from needing to rely on payday loans in the future. Start small, even if it's just $25 a month. Over time, it will grow, and you'll have a financial cushion to fall back on. Aim for 3-6 months' worth of living expenses.

Think of it as building a financial moat around your castle. It might take some time and effort, but it's worth it to protect yourself from future financial dragons.

Step 7: Celebrate Your Victory (But Maybe Not with Another Payday Loan!)

Congratulations! You've escaped the payday loan cycle! Take a moment to celebrate your accomplishment. Treat yourself to something nice, but don't go overboard. Remember, you're trying to build a stable financial future, not throw it all away on a shopping spree.

Remember: Getting out of the payday loan cycle is a marathon, not a sprint. There will be setbacks and challenges along the way. But don't give up! With determination, a solid plan, and a little bit of humor, you can achieve financial freedom. And who knows, maybe one day you'll be the one giving advice to someone else trapped in the payday loan swamp. Now, go forth and conquer!

:max_bytes(150000):strip_icc()/170652617-F-56a066405f9b58eba4b0439b.jpg)

:max_bytes(150000):strip_icc()/GettyImages-520471777-56a066b45f9b58eba4b04529.jpg)