How To Get Out Of A Predatory Car Loan

Okay, so you accidentally signed up for a car loan that feels less like a helping hand and more like a… well, a loan shark wearing a shiny chrome grill. Been there? Maybe not. But knowing how to dodge a predatory auto loan is like knowing a secret handshake. Cool, right?

Don't panic! We're going to break down how to escape this financial fender-bender. Think of it as a treasure hunt, except the treasure is your hard-earned money.

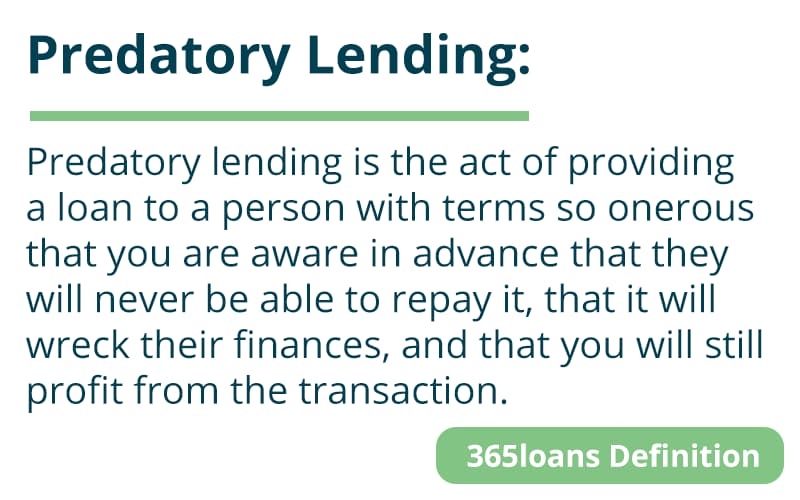

First Things First: What IS a Predatory Car Loan?

Predatory loans are sneaky. They lure you in with promises and then…bam! You're drowning in high interest rates and ridiculous fees. Ever feel like you’re paying more for the oxygen in the car than the actual car? Yeah, that's probably predatory.

Must Read

Here's the gist: They prey on people with bad credit or limited financial knowledge. They're like those carnival games where you can never actually win that giant stuffed animal.

A quirky fact: Did you know the word "predatory" comes from animals that hunt other animals? Makes sense, right? These loans are definitely on the hunt for your wallet!

Red Flags Waving Wildly

So, how do you know if you're dealing with a loan from the dark side? Watch out for these signs:

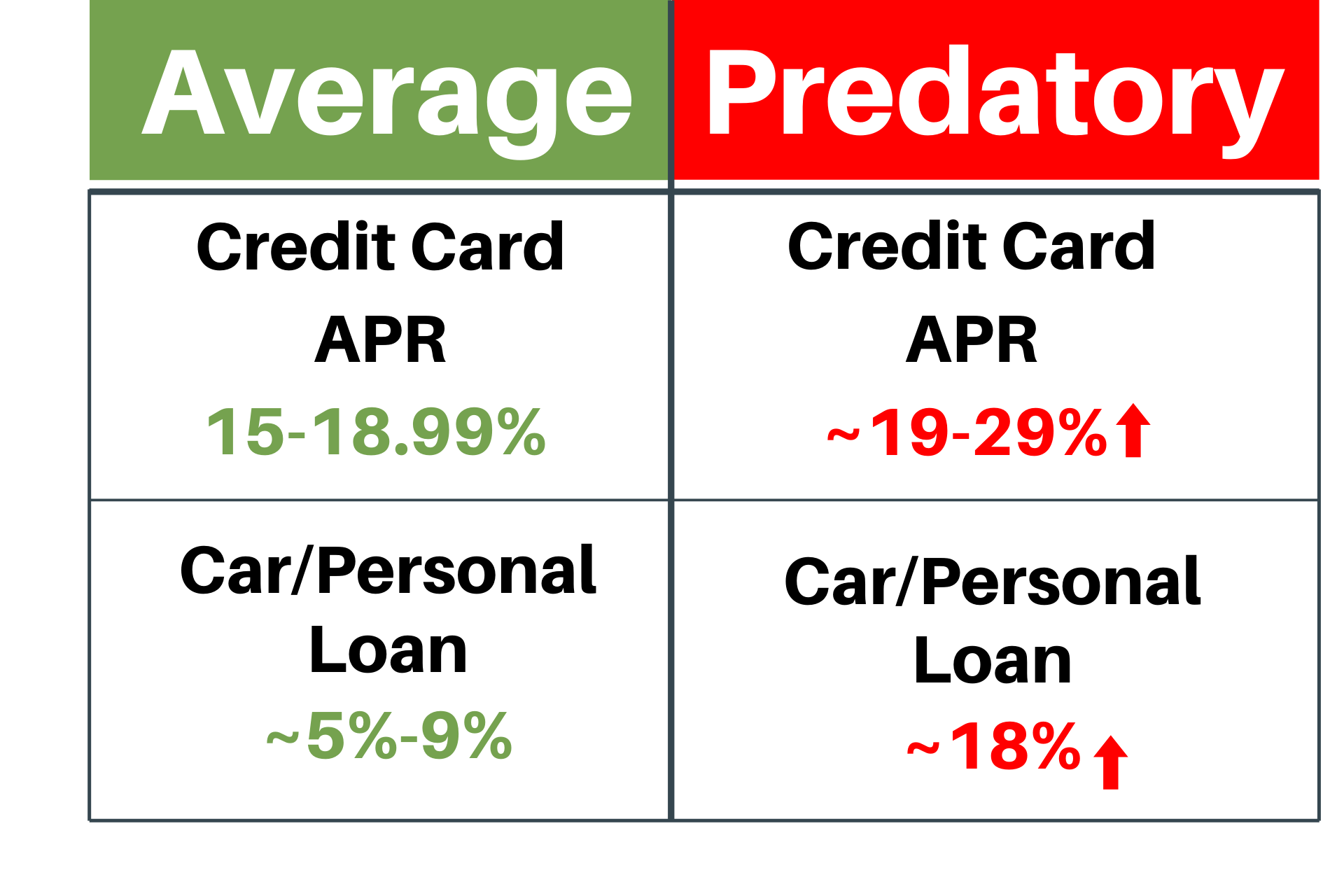

- Insane Interest Rates: Anything way above the average is a huge warning. We're talking rates so high, you might need oxygen just to read them. Seriously, check out the average interest rates online before signing anything.

- Hidden Fees Galore: Application fees, processing fees, documentation fees… the list goes on and on. It’s like a never-ending buffet of fees, but instead of feeling full, you just feel robbed.

- Loan Terms Longer Than a Netflix Binge: Seven-year loan for a car? That's practically a mortgage on wheels! You'll be paying for that car long after it's rusted into oblivion.

- Pressure, Pressure, Pressure: They're rushing you to sign. No time to think, no time to compare. It's like they're playing financial hot potato, and you're about to get burned.

- Crazy Fine Print: So small you need a magnifying glass. Filled with legal jargon only a lawyer could understand. This is where the real nastiness hides.

Remember, knowledge is power! Like knowing that a group of owls is called a parliament. Random, but useful! Just like this info.

Escape Route #1: The “Cooling-Off” Period (Maybe!)

Alright, this is a bit of a long shot. Most states don’t have a "cooling-off" period for car loans. But it’s worth checking!

What’s a cooling-off period? It's a legal window (usually a few days) where you can back out of a deal without penalty. Think of it like a "do-over" button for your financial life.

How to check: Google "[Your State] Car Loan Cooling Off Period." Or contact your state's attorney general's office. They're the superheroes of consumer protection! They might know the legal loopholes you're looking for.

Escape Route #2: Refinance, Baby, Refinance!

This is your most likely route to freedom. Refinancing means taking out a new loan with better terms to pay off the predatory one. It's like trading in your lemon of a loan for a sweet, juicy peach.

Where to refinance: Banks, credit unions, online lenders. Shop around! Get quotes from multiple lenders. Don't be afraid to haggle! It's your money, after all.

Pro Tip: Before you refinance, improve your credit score! Pay your bills on time, reduce your debt, and avoid applying for new credit cards. A better credit score means a better interest rate. Think of it as leveling up in a video game… but instead of slaying dragons, you're slaying debt!

Did you know that the word "mortgage" comes from Old French and literally means "dead pledge"? Let’s not let your car loan become a dead pledge, either!

Escape Route #3: Trade-In Tango

This one is a bit trickier, but if you're desperate, it's worth considering. Trade in your car for a newer (or even just different) vehicle with a more favorable loan.

The Catch: You'll probably lose money on the trade-in. But if the predatory loan is costing you a fortune in the long run, it might be the lesser of two evils.

Do your research! Find out the true market value of your car. Don't let the dealer lowball you. They’ll try! It’s like their Olympic sport. Arm yourself with knowledge. Sites like Kelley Blue Book and Edmunds are your allies.

Important: Make sure the new loan is actually better than the old one! Don't jump out of the frying pan and into the fire. This is a crucial step.

Escape Route #4: The "Negotiate Like a Boss" Strategy

This one requires some serious guts. Contact the lender directly and try to negotiate better terms. It's like talking your way out of a speeding ticket. (Disclaimer: This doesn’t always work, but it’s worth a shot!)

Be polite, but firm. Explain your situation. Point out the unfair terms of the loan. Ask them to lower the interest rate or reduce the fees.

Have evidence ready. Show them comparable loan rates from other lenders. Prove that you've done your homework. Knowledge is power, remember?

Threaten to refinance. Tell them you're considering refinancing with a competitor. This might scare them into offering you a better deal to keep your business.

Fun fact: Did you know that the longest negotiation ever lasted for 36 years? Hopefully, yours won’t take nearly that long.

Escape Route #5: Bankruptcy - The Last Resort

Bankruptcy should only be considered if all other options have failed. It's a drastic measure with serious consequences. Think of it as the nuclear option for your finances.

Talk to a bankruptcy attorney. They can advise you on the pros and cons of filing for bankruptcy and help you navigate the process.

Bankruptcy will damage your credit score. It will stay on your credit report for years. But it might be the only way to escape the crushing weight of a predatory loan.

Preventative Measures: Don’t Get Predated On!

The best way to escape a predatory car loan is to avoid getting one in the first place. It's like preventing a sunburn – much easier than treating one.

- Shop around for loans before you shop for a car. Get pre-approved. Know your budget. Don't let the dealer control the financing process.

- Read the fine print. Every single word. If you don't understand something, ask questions. Don't be afraid to be annoying. It's your money!

- Don't be pressured. Take your time. Walk away if you feel uncomfortable. There are plenty of other dealerships and lenders out there.

- Bring a friend or family member. A second set of eyes (and ears) can help you spot red flags. Plus, moral support is always appreciated.

Remember, buying a car should be exciting, not terrifying. By being informed and proactive, you can drive off into the sunset with a smile on your face… and without a predatory loan hanging over your head!

So, there you have it. Your guide to escaping the clutches of a predatory car loan. Now go forth and conquer your financial fears! And remember, a little knowledge can save you a whole lot of money (and stress!). Happy driving!

/1868188609.jpeg#keepProtocol)