How To Find Profit Maximizing Price

Okay, so picture this: I was at a farmer's market last weekend, totally craving some fresh strawberries. There were two stalls selling them. Stall A had gorgeous, plump berries for $8 a pint. Stall B, right next door, had slightly smaller, maybe not quite as visually appealing berries for $6 a pint. Guess where the line was snaking out from? Yep, Stall B.

It got me thinking, you know? It's not always about having the best product. Sometimes, it's about figuring out the price that gets you the most cash in your pocket. And that, my friends, is the holy grail: the profit-maximizing price.

What is Profit Maximizing Price, Anyway?

Simply put, it's the price point that generates the highest possible profit for your business. Not necessarily the highest revenue (those aren't always the same!), but the one that leaves you with the most money after you've covered all your costs. It’s the sweet spot where you're selling enough units at a high enough price to really make bank.

Must Read

Now, before you start randomly slashing prices, thinking you'll become the next Walmart, hold your horses! Finding that perfect price isn't just guesswork. It involves a little bit of analysis, a dash of understanding your market, and maybe even a sprinkle of experimentation. But don’t worry, we’ll break it down.

Why Bother Finding It? (Spoiler: It’s About More Money)

I mean, duh, right? More profit is always a good thing. But let's dig a little deeper. Finding the profit-maximizing price can do the following:

- Boost your bottom line: Obviously. But think about what you can do with that extra cash. Invest in marketing? Hire more staff? Finally get that fancy espresso machine for the office? The possibilities are endless!

- Improve your competitive edge: Knowing your optimal price allows you to be more strategic in your pricing. Maybe you can afford to undercut your competitors slightly and still make a healthy profit.

- Inform your business decisions: Understanding the relationship between price, demand, and cost gives you valuable insights into your business. It helps you make smarter decisions about production, inventory, and marketing.

The Key Ingredients: Cost, Demand, and Competition

Think of these as the three musketeers of pricing. They all need to work together for you to find that profit-maximizing sweet spot.

1. Understanding Your Costs: Know Your Numbers!

This is non-negotiable. You have to know how much it costs you to produce and sell your product or service. We're talking about everything: raw materials, labor, rent, utilities, marketing, even that subscription to the office coffee service. (Hey, every penny counts!).

There are two main types of costs to consider:

- Fixed Costs: These are costs that don't change regardless of how much you produce. Think rent, salaries (for salaried employees, anyway), insurance, and equipment costs.

- Variable Costs: These costs fluctuate with your production volume. Think raw materials, hourly wages, shipping costs, and commissions.

The sum of these two costs is the total cost. So, if your fixed costs are $10,000 a month and your variable cost per unit is $5, then producing 1,000 units will cost you $15,000 ($10,000 + ($5 x 1,000)).

Knowing your costs is crucial because you need to ensure that your price covers all your expenses and still leaves you with a profit. Selling something for less than it costs you to produce? That's a recipe for disaster, my friend. (Unless, of course, you're running some kind of super-strategic loss leader campaign, but that's a whole other ballgame).

2. Decoding Demand: What Are People Willing to Pay?

Demand refers to how much of your product or service customers are willing to buy at different price points. It's governed by the famous law of demand: as the price goes up, demand usually goes down (and vice versa). Usually. Luxury goods are a different beast altogether. But for most of us, the inverse relationship holds true.

The relationship between price and demand is called the demand curve. It can be tricky to figure out, but there are a few ways to get a handle on it:

- Market Research: This is the gold standard. Surveys, focus groups, and competitor analysis can give you valuable insights into what customers are willing to pay.

- Historical Data: Look at your past sales data. How did sales change when you adjusted prices in the past? This can give you a clue about the price elasticity of demand for your product.

- A/B Testing: Offer your product at different prices to different segments of your audience and see which price point generates the most profit. (Just make sure you're not violating any price discrimination laws!).

- Gut Feeling (Use with Caution!): Sometimes, you just have a hunch. But always back up your intuition with data whenever possible. Don't rely solely on your "expert opinion" – the market rarely agrees with your internal assumptions!

Understanding demand is crucial because it tells you how sensitive customers are to price changes. If demand is elastic (meaning it changes a lot when the price changes), you need to be very careful about increasing prices. If demand is inelastic (meaning it doesn't change much when the price changes), you have more leeway to experiment with higher prices.

3. The Competition: Keep an Eye on Your Rivals!

You don't operate in a vacuum. Your competitors' prices will influence what customers are willing to pay for your product or service. You need to know what they're charging, what their value proposition is, and how your product compares. Don’t be afraid to be a friendly ghost and check out their websites, stores, and marketing materials.

There are a few different pricing strategies you can use in relation to your competitors:

- Price Matching: Offering the same price as your competitors. This is a common strategy in commodity markets where products are largely undifferentiated.

- Underpricing: Offering a lower price than your competitors. This can be a good way to gain market share, but it can also lead to a price war (which nobody wants!).

- Premium Pricing: Offering a higher price than your competitors. This works if you have a strong brand, a superior product, or a unique value proposition. Think Apple.

Knowing your competitive landscape helps you position your product effectively and avoid pricing yourself out of the market. You need to strike a balance between being competitive and maximizing your profit margin.

Methods for Finding That Magic Number

Alright, now let's get into the nitty-gritty. Here are some common methods for finding the profit-maximizing price:

1. Cost-Plus Pricing: Simple, But Maybe Not the Best

This is the simplest method. You calculate your total cost per unit and then add a markup percentage to arrive at your selling price. For example, if your cost per unit is $10 and you want a 50% markup, your selling price would be $15.

Pros: Easy to calculate and ensures you cover your costs. Great for simple businesses or those with very stable costs.

Cons: Doesn't consider demand or competition. Can lead to overpricing or underpricing, depending on the market. It basically ignores the fact that people might not actually want to pay that much, no matter how much it costs you to make.

2. Value-Based Pricing: Understanding What Customers Really Want

This method focuses on the perceived value of your product or service to the customer. What problem does it solve? How much are customers willing to pay to solve that problem?

Pros: Can command a higher price if your product offers significant value. Great for premium products or services.

Cons: Requires a deep understanding of your target market and their needs. It can be challenging to accurately quantify value.

For example, think of a high-end management consultancy. They don't price based on how many hours they work (though they track that internally). They price based on the value they bring to the client – increased revenue, improved efficiency, etc. That’s why some consultants can charge hundreds or thousands of dollars per hour.

3. Competitive Pricing: Keeping Up with the Joneses

This method involves setting your prices based on what your competitors are charging. You can choose to match their prices, undercut them, or price yourself at a premium.

Pros: Easy to implement. Can help you stay competitive in the market.

Cons: Doesn't consider your own costs or value proposition. Can lead to a race to the bottom if everyone is constantly undercutting each other.

4. Price Elasticity of Demand (PED) Formula: The Data-Driven Approach

This one gets a little mathy, but bear with me! The price elasticity of demand (PED) measures how much the quantity demanded of a product changes in response to a change in its price. The formula is:

PED = (% Change in Quantity Demanded) / (% Change in Price)

If the absolute value of PED is greater than 1, demand is elastic (sensitive to price changes). If it's less than 1, demand is inelastic (not very sensitive to price changes). If it’s exactly 1, then it’s unit elastic.

Don’t worry, you can use online calculators to help you with the math!

Knowing your PED allows you to estimate how much your sales will change if you raise or lower your prices. This is crucial for determining the profit-maximizing price.

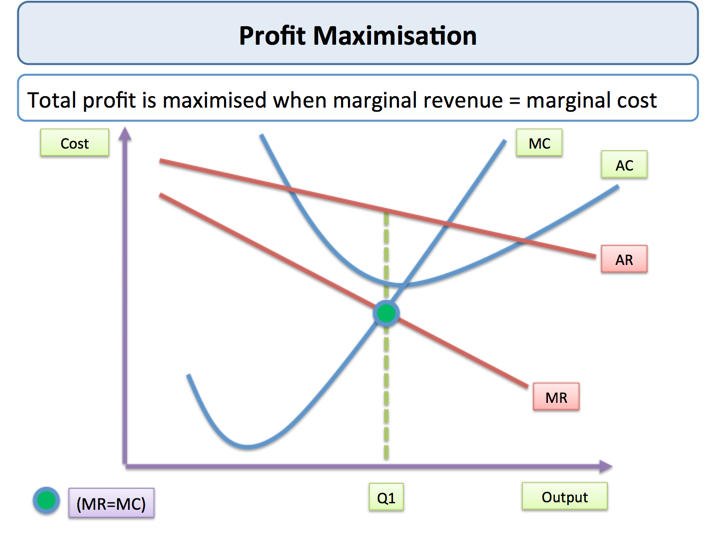

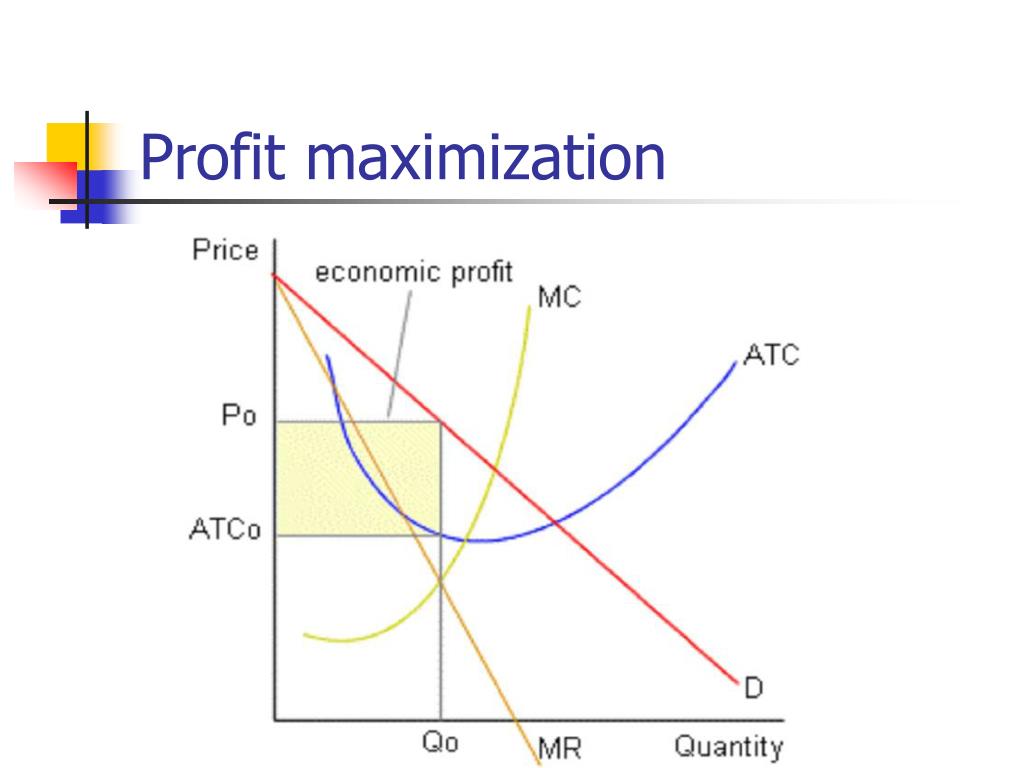

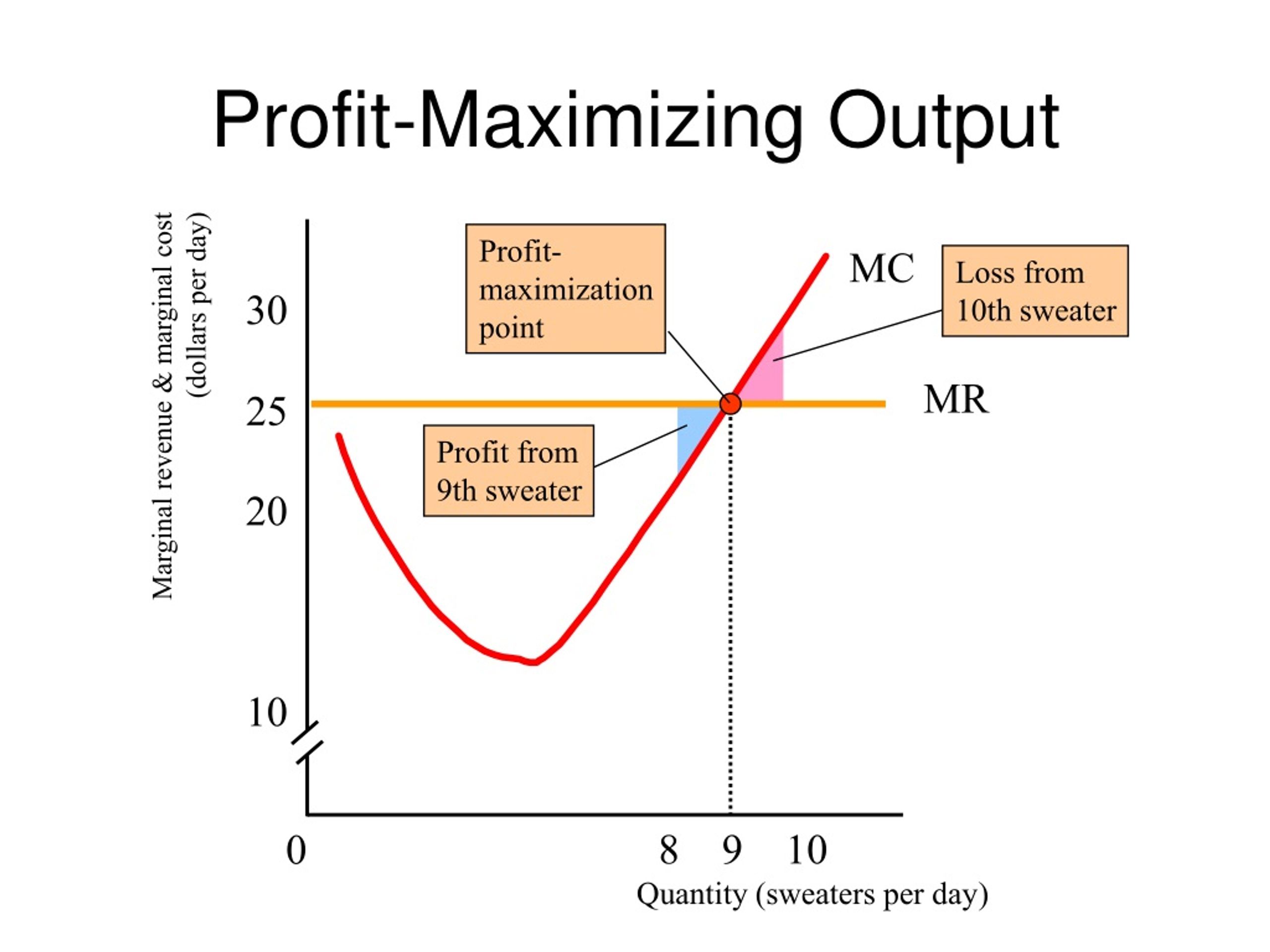

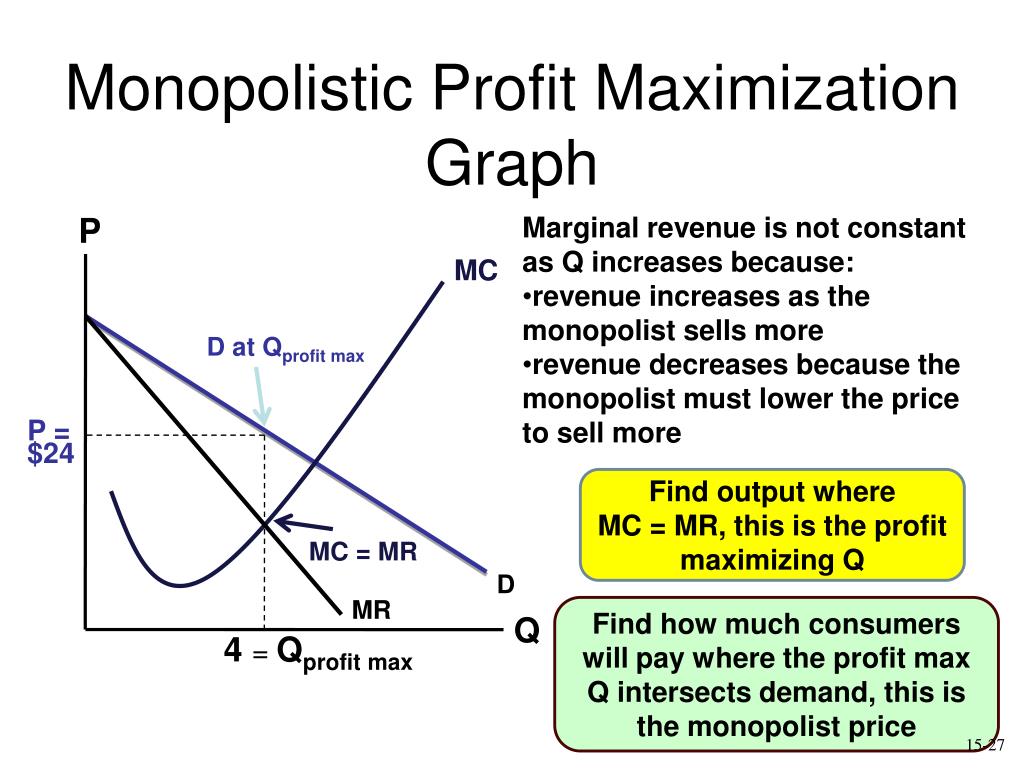

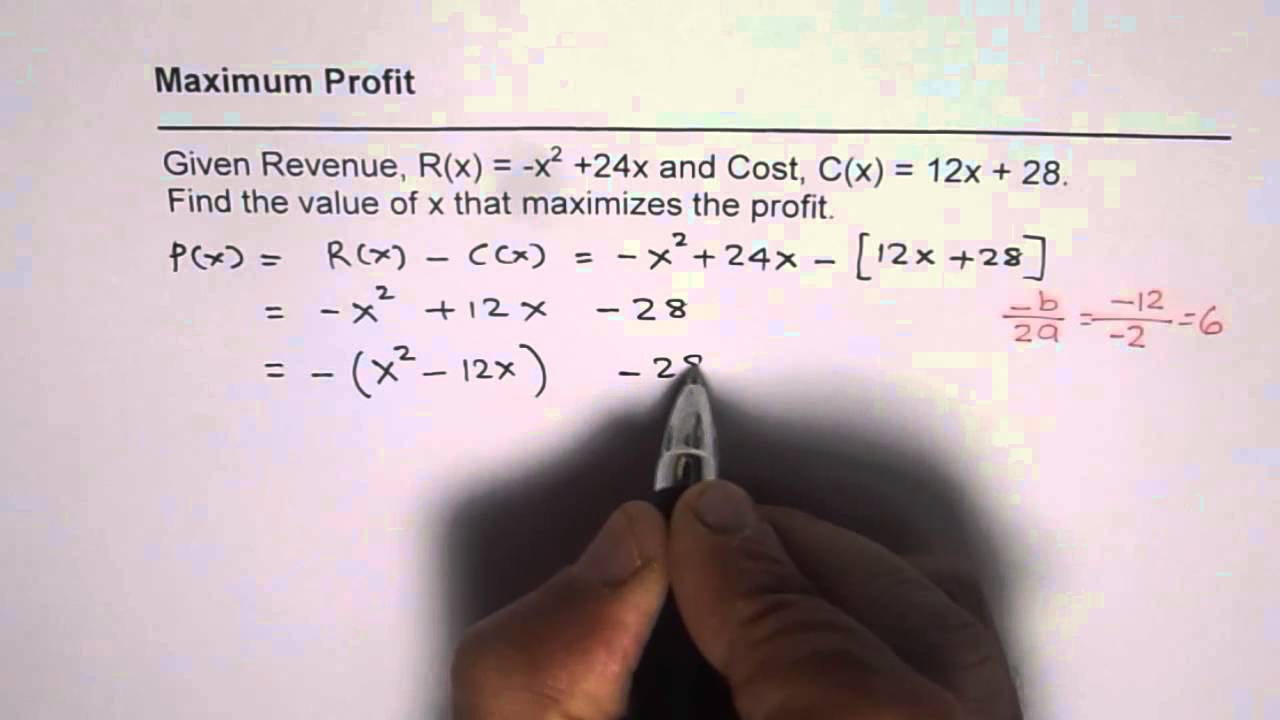

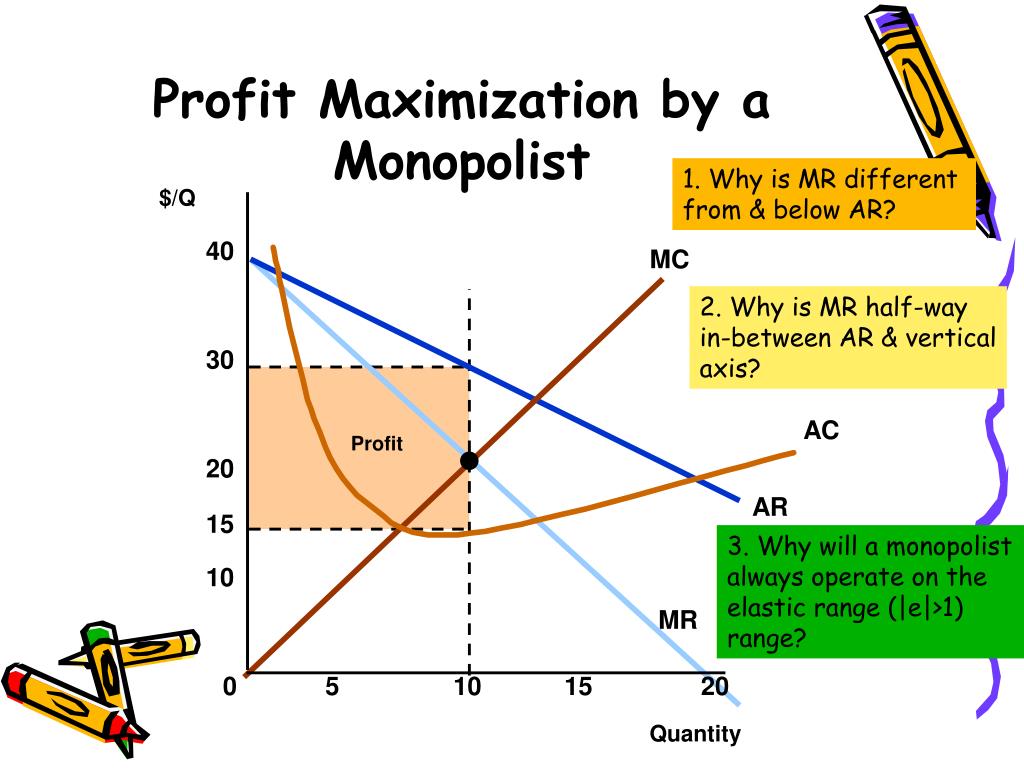

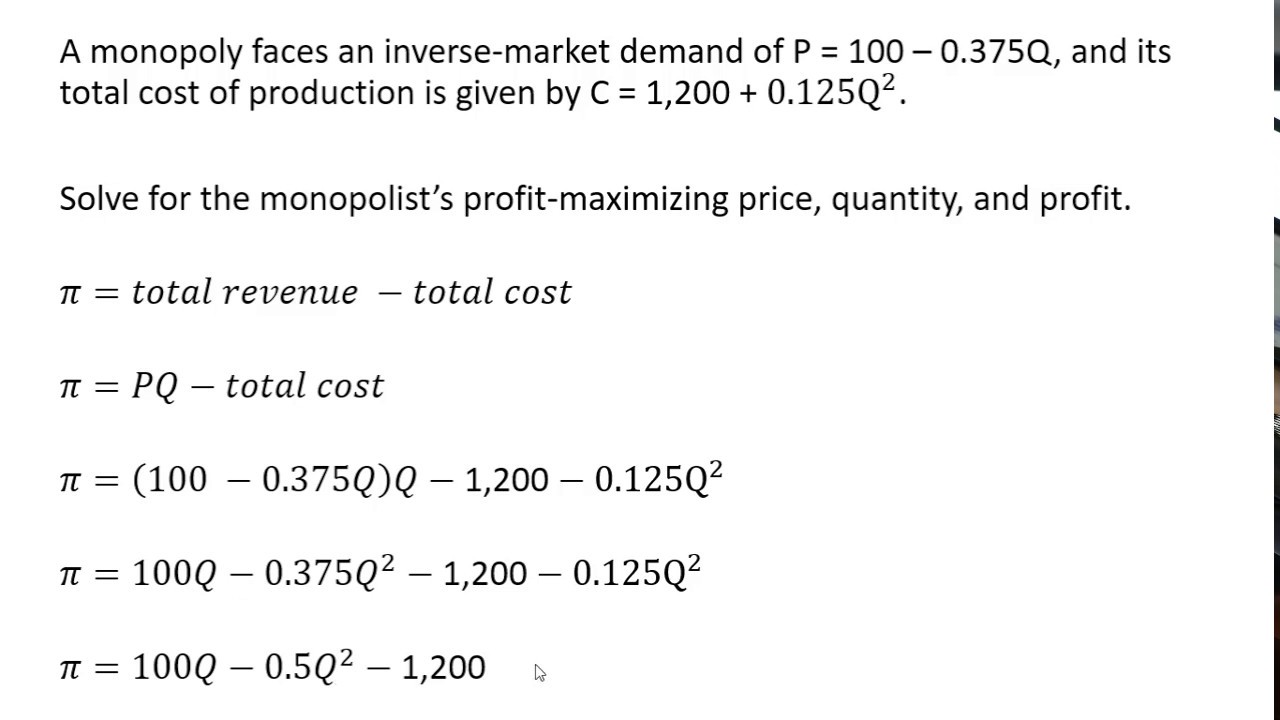

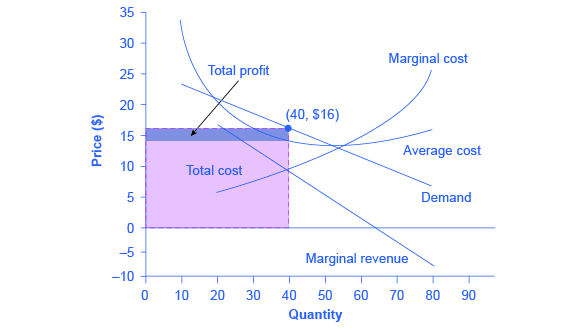

5. Marginal Cost and Marginal Revenue: The Economics Approach

This method involves finding the point where marginal cost (the cost of producing one more unit) equals marginal revenue (the revenue from selling one more unit). At this point, you're maximizing your profit.

Pros: Theoretically sound and can lead to the most accurate pricing decisions.

Cons: Requires accurate data on costs and revenue, which can be difficult to obtain. Also, it's a bit more complex to calculate.

The Iterative Process: Testing, Learning, and Adjusting

Finding the profit-maximizing price isn't a one-time thing. It's an ongoing process of testing, learning, and adjusting. The market is constantly changing, so you need to be prepared to adapt your pricing strategy accordingly.

Don't be afraid to experiment. Try different prices, track your results, and see what works best. Use A/B testing, monitor your competitors' prices, and pay attention to customer feedback.

Be prepared to pivot. If your initial pricing strategy isn't working, don't be afraid to change course. Maybe you need to lower your prices to increase sales volume. Or maybe you need to raise your prices to reflect the value of your product.

Remember: The profit-maximizing price is a moving target. You need to stay agile and responsive to the market to stay ahead of the game.

Wrapping it Up

Finding the profit-maximizing price is a crucial part of running a successful business. It requires a deep understanding of your costs, demand, and competition. By using the methods outlined above, you can increase your profits, improve your competitive edge, and make smarter business decisions.

So go forth, analyze your data, experiment with different prices, and find that sweet spot! Your bank account will thank you for it.

And remember those strawberries at the farmer’s market? Turns out, Stall A lowered their price later that afternoon and sold out completely. Even the prettiest berries need the right price to fly off the shelves!