How Many Rollovers Can You Do In A Year

Understanding Retirement Account Rollovers: A Concise Guide

Navigating the complexities of retirement savings often involves considering rollovers. A rollover allows you to move funds from one retirement account to another, potentially offering greater investment flexibility or cost savings. However, it's crucial to understand the rules governing rollovers, particularly the limitations on how many you can execute within a given year.

Direct vs. Indirect Rollovers: Key Differences

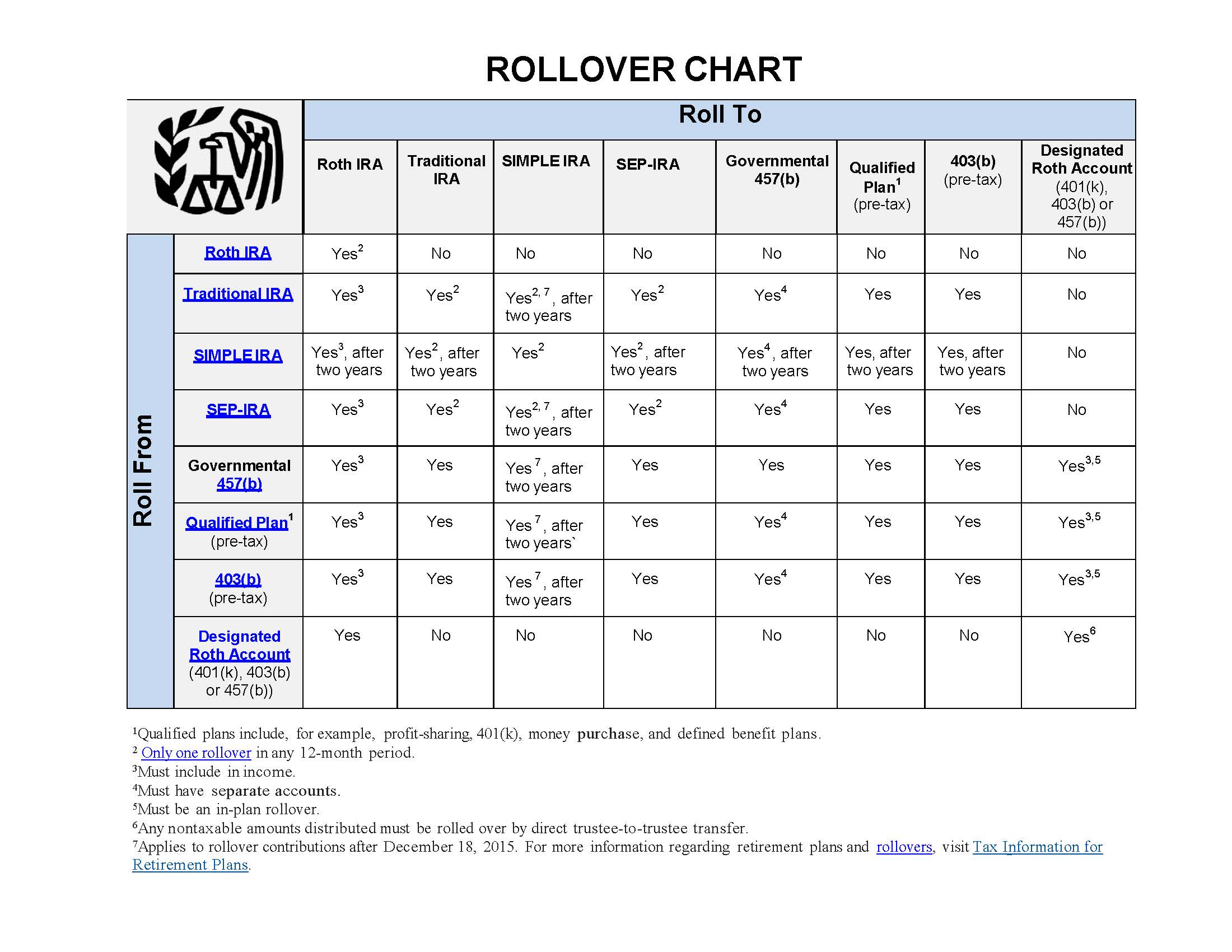

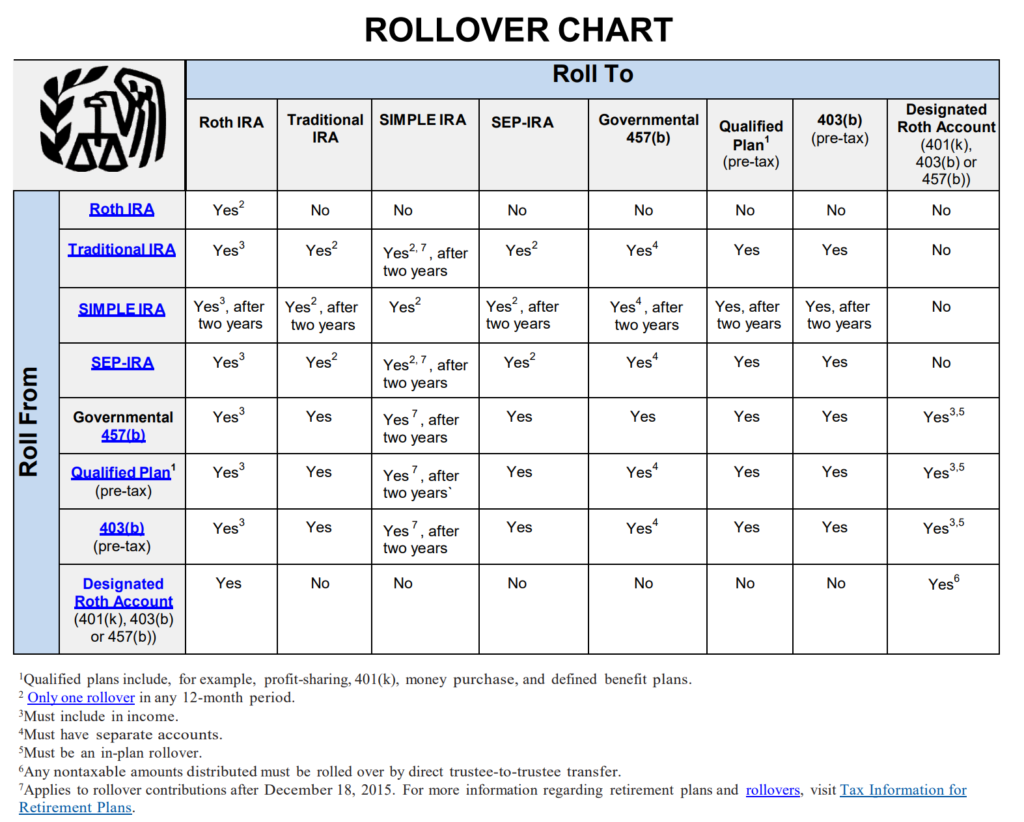

The IRS distinguishes between two primary types of rollovers: direct and indirect. This distinction significantly impacts the frequency with which you can utilize rollovers. A direct rollover occurs when funds are transferred directly from one retirement account custodian to another. You never personally receive the money. An indirect rollover, on the other hand, involves receiving a distribution from your retirement account, and then reinvesting those funds into a new retirement account within a specific timeframe.

"A direct rollover is generally the most straightforward method, as it avoids potential tax implications and the complexities of the 60-day rule,"

Must Read

The One-Rollover-Per-Year Rule: Focusing on Indirect Rollovers

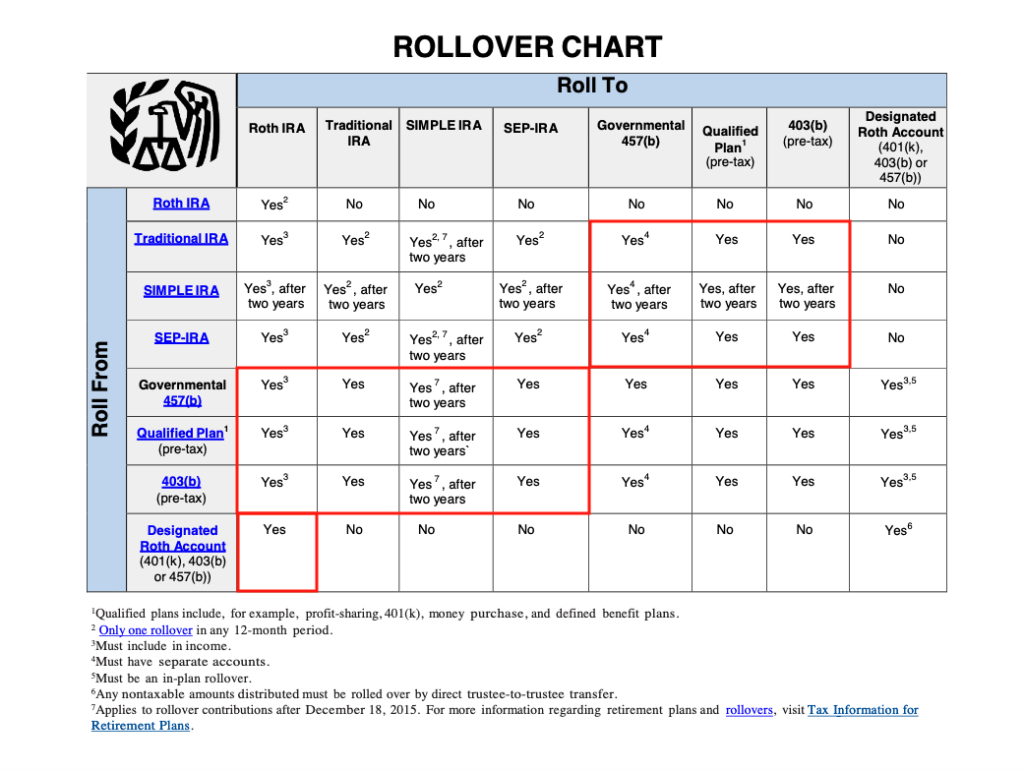

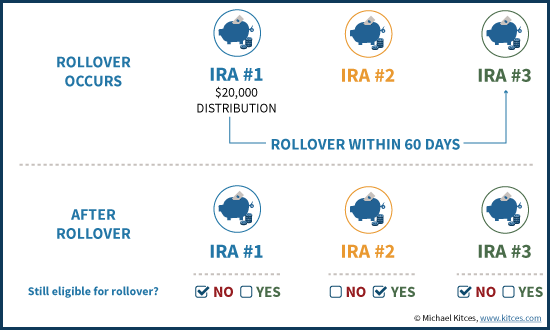

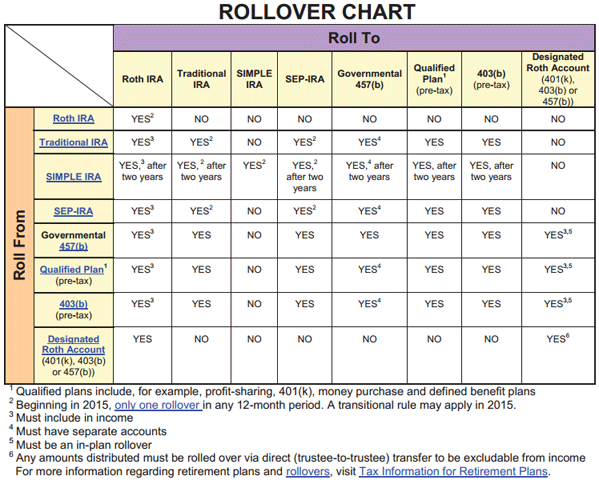

The IRS imposes a “one-rollover-per-year” rule that specifically applies to indirect rollovers. This rule states that you can only roll over funds from one IRA (Individual Retirement Account) to another IRA once in a 365-day period, regardless of how many IRAs you own.

The operative word here is "IRA." This rule applies on an aggregate basis to all of your IRAs. So, if you roll over funds from IRA A to IRA B, you cannot roll over funds from any other IRA to another IRA until one year has passed from the date you received the distribution from IRA A.

Example: Let's say you take a distribution from your Traditional IRA on March 1, 2024, and roll it over into a Roth IRA. Under the one-rollover-per-year rule, you cannot perform another indirect rollover involving any of your IRAs until after March 1, 2025.

Exceptions to the One-Rollover-Per-Year Rule

Several situations are exempt from the one-rollover-per-year rule, providing greater flexibility in managing your retirement savings:

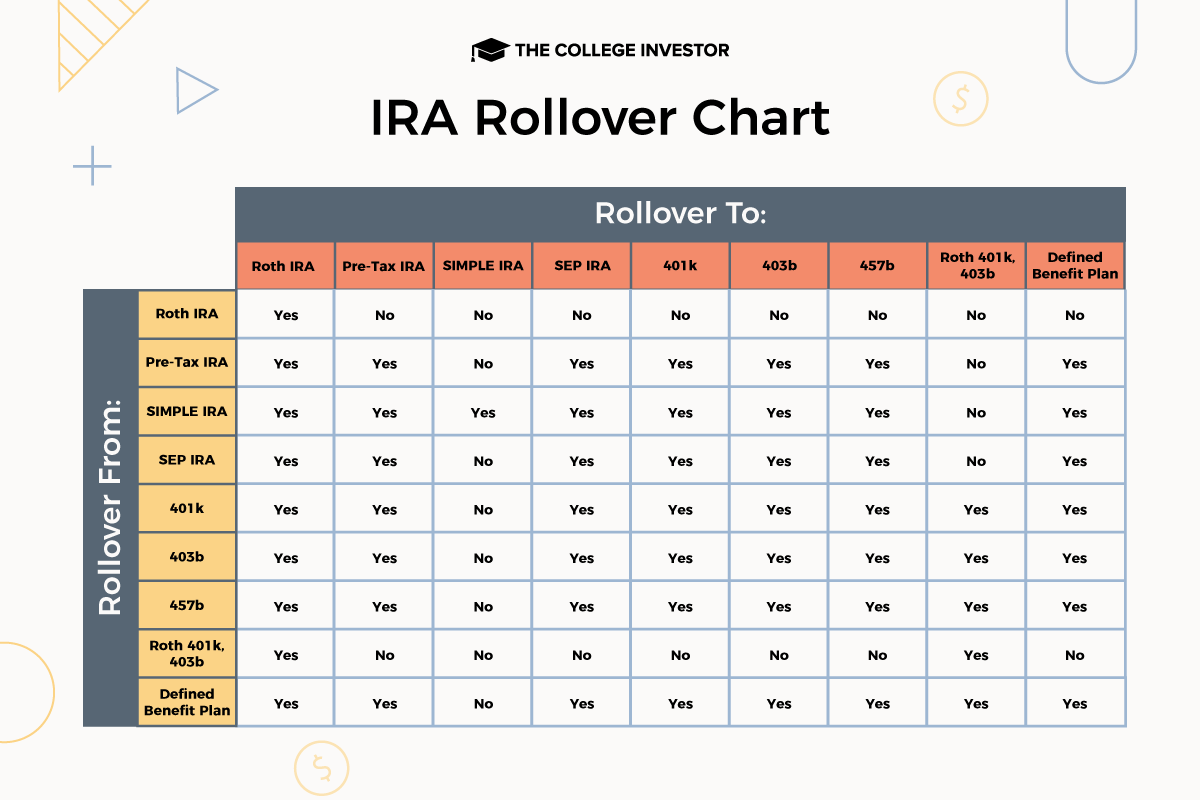

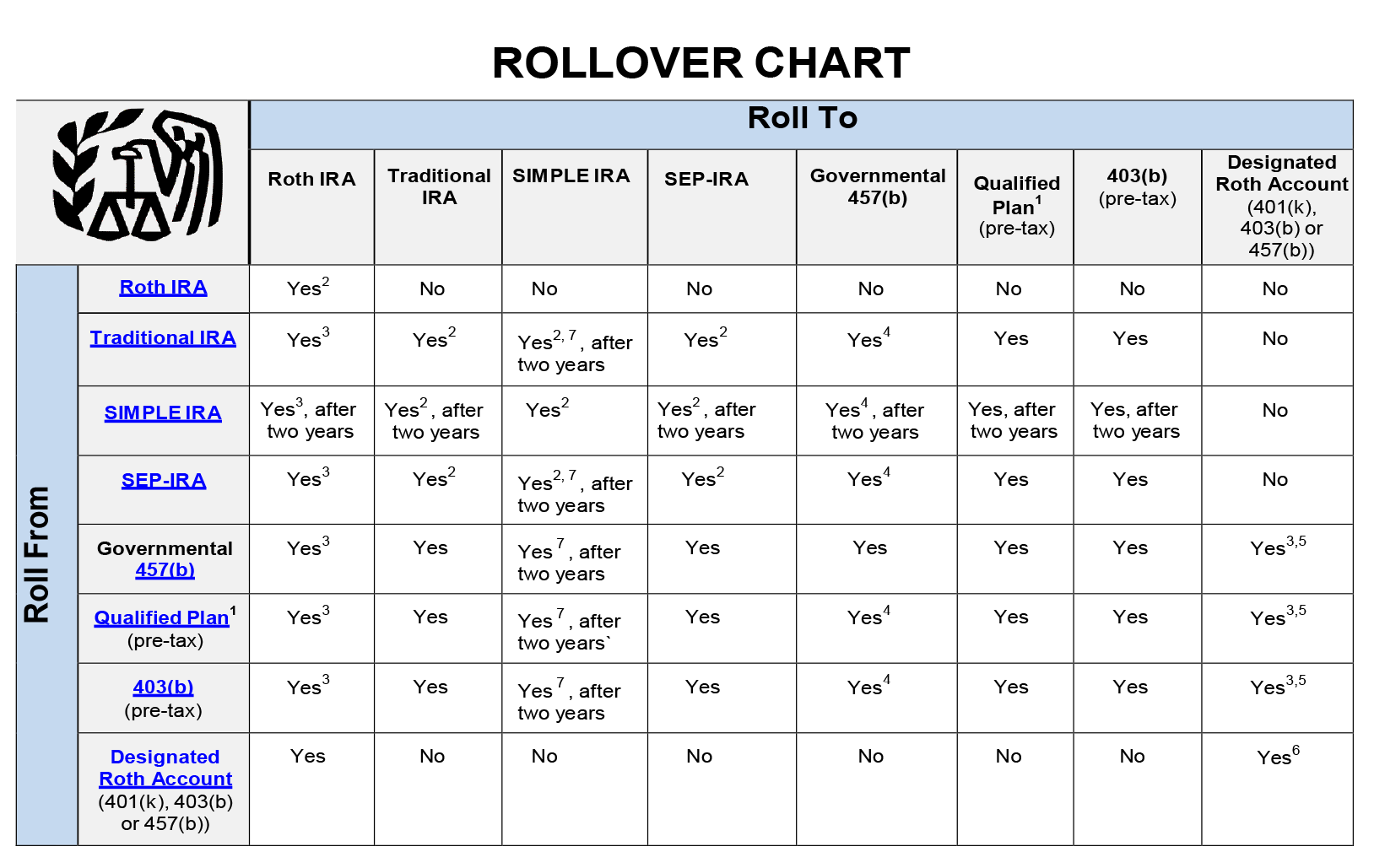

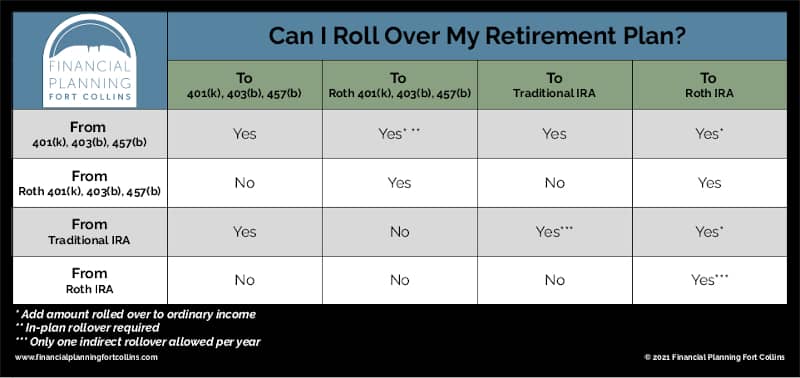

- Direct Rollovers: As mentioned earlier, direct rollovers are not subject to this limitation. You can execute multiple direct rollovers within a year without penalty. This is because the funds never enter your possession.

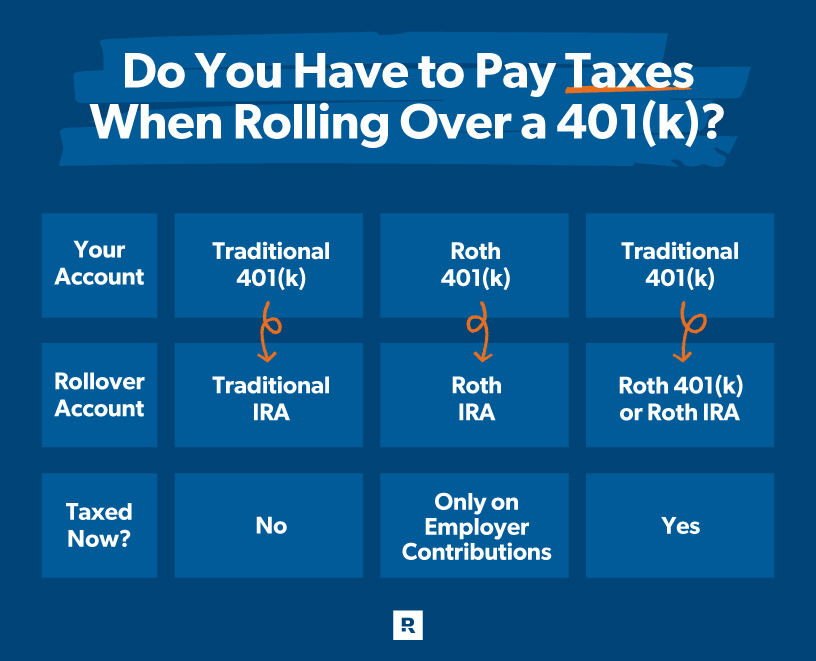

- Rollovers from Traditional IRAs to Roth IRAs (Conversions): Technically, a rollover from a traditional IRA to a Roth IRA is considered a conversion, not a rollover, and is not subject to the one-rollover-per-year rule. You can convert funds from a Traditional IRA to a Roth IRA multiple times throughout the year, although the tax implications should be carefully considered. Keep in mind that once you convert, you generally cannot recharacterize the conversion back to a traditional IRA (this was possible in the past but is no longer the case).

- Rollovers from Qualified Retirement Plans (e.g., 401(k)s) to IRAs: Rollovers from employer-sponsored retirement plans, such as 401(k)s, 403(b)s, or governmental 457(b) plans, to an IRA do not count towards the one-rollover-per-year limit for IRAs. You can roll over funds from a 401(k) to an IRA and still perform an indirect IRA rollover within the same year.

- Rollovers from One Qualified Retirement Plan to Another: Moving funds directly from one 401(k) to another 401(k), or from a 403(b) to another 403(b), is also exempt from the one-rollover-per-year rule.

Potential Consequences of Violating the One-Rollover-Per-Year Rule

Failing to adhere to the one-rollover-per-year rule can have significant consequences. If you violate the rule, the IRS may consider the second (or subsequent) rollover a taxable distribution. This means that the amount rolled over will be subject to income tax, and if you're under age 59 ½, you may also be subject to a 10% early withdrawal penalty.

Furthermore, the IRS may disallow the rollover, meaning that the funds will be treated as if they were never rolled over. This can create significant tax liabilities and penalties.

The 60-Day Rule: A Critical Deadline for Indirect Rollovers

Regardless of the one-rollover-per-year rule, all indirect rollovers must adhere to the 60-day rule. This rule mandates that you reinvest the distributed funds into a new retirement account within 60 days of receiving the distribution. Failure to meet this deadline results in the distribution being treated as a taxable event, subject to income tax and potential penalties. The 60-day window begins the day after you receive the distribution.

Important Note: If unforeseen circumstances prevent you from meeting the 60-day deadline, you may be able to apply for a waiver from the IRS. However, waivers are granted on a case-by-case basis and are not guaranteed. Legitimate reasons for missing the deadline often include serious illness, natural disasters, or errors made by financial institutions.

Seek Professional Advice

Retirement planning and rollover decisions can be complex. Before making any decisions, it is highly recommended to consult with a qualified financial advisor or tax professional. They can help you assess your individual circumstances, understand the potential tax implications of rollovers, and develop a strategy that aligns with your financial goals.

Detailed Example Scenario

John has a Traditional IRA (IRA A) and a SEP IRA (IRA B). On June 1, 2024, John takes a distribution from IRA A and rolls it over into a new Traditional IRA (IRA C) within 60 days. This triggers the one-rollover-per-year rule. Even if John wanted to take a distribution from his SEP IRA (IRA B) and roll it over into a different IRA, say in August 2024, he would be prohibited from doing so until after June 1, 2025. The one-year clock started on June 1, 2024. However, John could perform a direct rollover from his 401(k) at work into an IRA during that time, as that is a separate type of rollover and doesn't fall under the one-rollover-per-year IRA rule.

Key Takeaways: Navigating Rollover Rules Effectively

- The one-rollover-per-year rule applies specifically to indirect rollovers from one IRA to another.

- Direct rollovers, conversions, and rollovers from qualified retirement plans to IRAs are generally exempt from this rule.

- Violating the one-rollover-per-year rule can result in taxable distributions and penalties.

- The 60-day rule requires you to reinvest distributed funds within 60 days to avoid taxes and penalties.

- Consult with a qualified financial advisor or tax professional before making any rollover decisions.