How Accurate Is Kikoff Credit Score

Okay, so picture this: my friend Sarah, who's basically allergic to credit cards (fear of overspending, you know?), was complaining about how she wanted to buy a house but her credit score was... well, let's just say it wasn't "dream home" material. Then, she started telling me about this thing called Kikoff. "It's like, a credit-building loan for $500, but you only buy stuff from their store," she explained, sounding slightly skeptical. My first thought? "Sounds kinda... weird." But then I got curious. Is this really a legit way to boost your score, or is it just another one of those gimmicky things that preys on people desperate for a better credit rating?

That got me thinking: Just how accurate is the credit score Kikoff provides? Does it actually reflect your real creditworthiness, or is it just a "feel-good" number that doesn't mean much in the real world? We're diving deep into that question today, folks. Buckle up!

What Exactly Is Kikoff, Anyway?

For those of you who, like me initially, are scratching your heads, let's break down what Kikoff does. In essence, it's a credit-building platform that offers a few different products designed to help you establish or improve your credit history.

Must Read

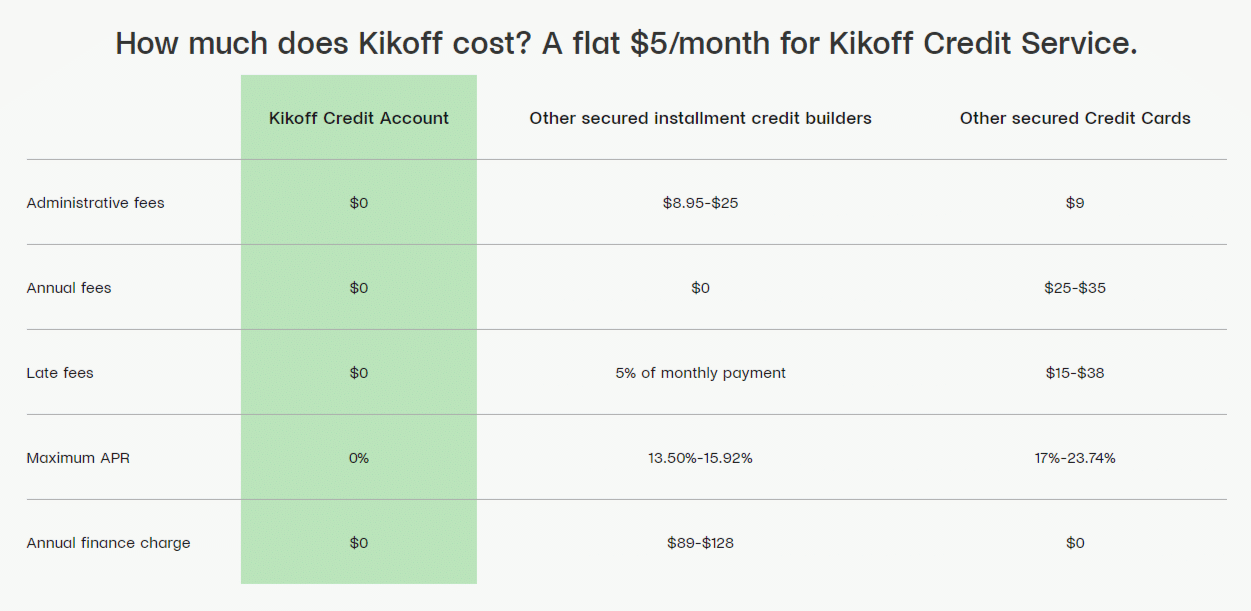

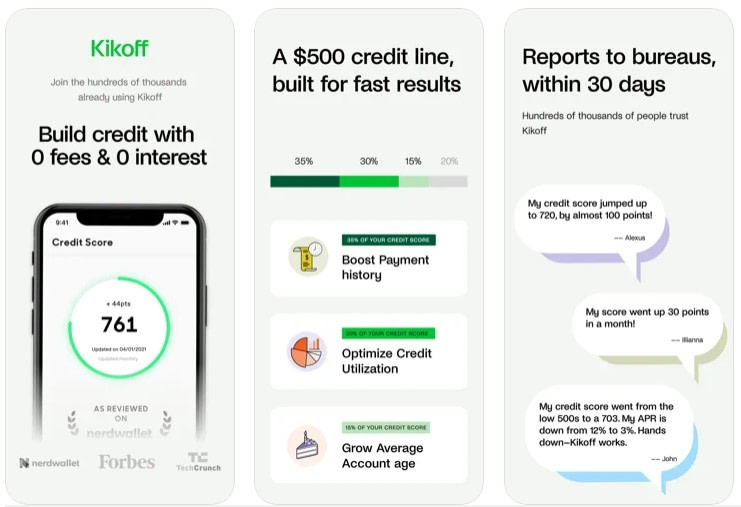

- Kikoff Credit Account: This is their flagship product. You get a $500 line of credit to be used only in the Kikoff store (which mostly sells digital books, online courses, and wellness products). You make small monthly payments (like, $5 small) over a long period. Think of it as a really, really slow-burning store credit card.

- Kikoff Secured Credit Card: Basically, a regular secured credit card where you put down a security deposit, and that deposit becomes your credit limit. This is more in line with traditional credit-building methods.

- Kikoff Credit Builder Loan: Similar to other credit-builder loans, you make payments on a loan, and Kikoff reports those payments to the major credit bureaus. The key difference is the amount - you're usually talking about very small loan amounts.

The idea behind all of these is simple: Consistent, on-time payments are the holy grail of credit building. Kikoff provides a (relatively) low-risk way to achieve that, especially for people who are new to credit or have had trouble managing credit in the past.

Kikoff's Credit Score: A Peek Behind the Curtain

So, Kikoff does show you a credit score, right? But the burning question is: Is it legit? Well, here's the thing:

- They Use a Credit Bureau Score: Kikoff typically uses VantageScore 3.0. This is important because there are different scoring models out there (like FICO, which is arguably the king of credit scores).

- VantageScore vs. FICO: This is where things get a little tricky. While VantageScore is a valid credit scoring model, it's not as widely used by lenders as FICO. Think of it like this: VantageScore is like knowing a second language – it's cool and can be useful, but FICO is like knowing English in the business world – it's practically essential.

What does this mean for you? It means that the score you see on Kikoff is likely an indicator of your credit health, but it might not be the exact same score a lender sees when you apply for a mortgage or a car loan. (Yep, lenders often have their preferred scores, which can be a pain.)

How Accurate Is It Really? Factors to Consider

Alright, let's get down to brass tacks. Here are some factors that influence how well your Kikoff credit score reflects your overall creditworthiness:

1. Credit History Depth

Kikoff, by itself, isn't going to magically erase past credit mistakes. Your overall credit history still matters. If you have a history of late payments, high credit utilization on other accounts, or even bankruptcies, those things will still weigh heavily on your overall credit score, even if Kikoff shows you improvement.

Think of it like this: Kikoff is like putting a fresh coat of paint on a house that has a leaky roof. The paint might make it look better, but it doesn't fix the underlying problem.

2. Reporting Frequency

It's crucial that Kikoff actually reports your payment activity to all three major credit bureaus (Equifax, Experian, and TransUnion). Most of the time, Kikoff reports to all three, which is great. However, always double check on your credit report to make sure that the information is being reported correctly. If it's not, your efforts with Kikoff might be wasted.

You can get free copies of your credit reports from AnnualCreditReport.com. Seriously, check them regularly! It's like flossing – you know you should, but it's easy to forget. Set a reminder!

3. Impact on Credit Utilization

Credit utilization is the amount of credit you're using compared to your total available credit. It's a huge factor in your credit score. Ideally, you want to keep your utilization below 30%, and even lower is better.

Here's the potential problem with Kikoff: If you're only using Kikoff and you have that $500 line of credit, you might think, "Great, my utilization is low!" But if you also have a credit card with a $1,000 limit that you're maxing out, that high utilization is going to drag your score down, regardless of what Kikoff shows. The overall picture matters.

4. New Account Impact

Opening any new credit account, including a Kikoff account, can have a small negative impact on your credit score in the short term. This is because it lowers your average age of accounts, which is a factor in your credit score. However, this impact is usually temporary, and the long-term benefits of building positive credit history should outweigh the initial dip.

5. The Kikoff Store Limitation

Let's be real. The fact that you can only use the Kikoff credit account in their own store is a bit... limiting. It's not like you're building credit by buying groceries or gas, which are things you actually need. You're buying digital books or courses that you might not even use. This can feel a little less "real" than using a regular credit card responsibly.

So, Is Kikoff Worth It? The Million-Dollar Question

Okay, we've covered a lot. Now, for the big decision: Should you use Kikoff? Here's my take:

Pros:

- Easy Entry Point: It's a relatively low-risk way to start building credit, especially if you have no credit history at all. The small monthly payments are manageable for most people.

- Reports to Major Bureaus: Assuming they report correctly (always double-check!), it can help you establish a positive payment history.

- Can Boost VantageScore: If your goal is to see your VantageScore improve, Kikoff can definitely help with that.

Cons:

- Limited Use: The Kikoff store restriction is a major drawback. It's not like you're building credit by making everyday purchases.

- VantageScore Isn't Everything: Remember that lenders often prefer FICO scores. So, while your VantageScore might go up, it might not have as big of an impact on your ability to get approved for loans.

- Doesn't Fix Underlying Problems: Kikoff won't magically erase past credit mistakes. You need to address those issues separately.

My Verdict

Kikoff can be a decent tool for building credit, especially if you're just starting out or need a little boost. However, it's not a replacement for responsible credit management. It's important to:

- Pay all your bills on time. This is the single most important thing you can do for your credit score.

- Keep your credit utilization low. Don't max out your credit cards!

- Regularly check your credit reports. Look for errors and address them promptly.

- Consider other credit-building options. Secured credit cards, credit-builder loans (from a bank or credit union, not just online platforms), and even becoming an authorized user on someone else's credit card can be effective ways to build credit.

Ultimately, the accuracy of Kikoff's credit score is less important than the fact that it can help you build a positive credit history. Just remember to take it with a grain of salt and focus on developing good credit habits across the board. Don't rely solely on one platform – think of Kikoff as one piece of the puzzle in your credit-building journey.

So, what happened to my friend Sarah? Well, she did try Kikoff, and her VantageScore did go up a bit. But more importantly, it motivated her to start paying down her debt and being more mindful of her spending. That's the real key to a good credit score – not just a number on a screen, but a reflection of responsible financial behavior.