Gold Etf In Roth Ira Vs Taxable Account

Investing in gold exchange-traded funds (ETFs) can be a strategic component of a diversified portfolio. However, the tax implications and long-term benefits can vary significantly depending on whether the investment is held within a Roth IRA or a taxable account. Understanding these differences is crucial for making informed investment decisions.

Gold ETFs: A Brief Overview

A gold ETF is an investment fund that holds physical gold or gold futures contracts and tracks the price of gold. These ETFs allow investors to gain exposure to the gold market without directly owning physical gold. Some popular examples include the SPDR Gold Trust (GLD) and the iShares Gold Trust (IAU).

ETFs offer liquidity, diversification (compared to owning single gold bars), and relatively low expense ratios. Investors can buy and sell shares of these ETFs on major stock exchanges, mirroring the trading of stocks. The price of an ETF share typically reflects the current market value of gold, adjusted for the ETF's expense ratio.

Must Read

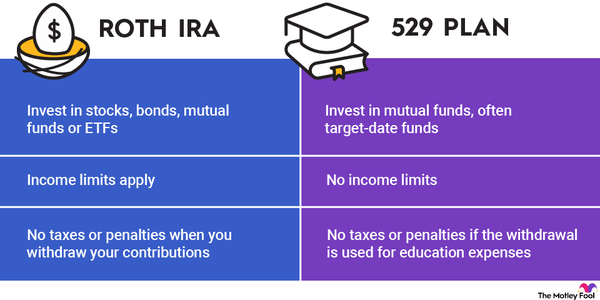

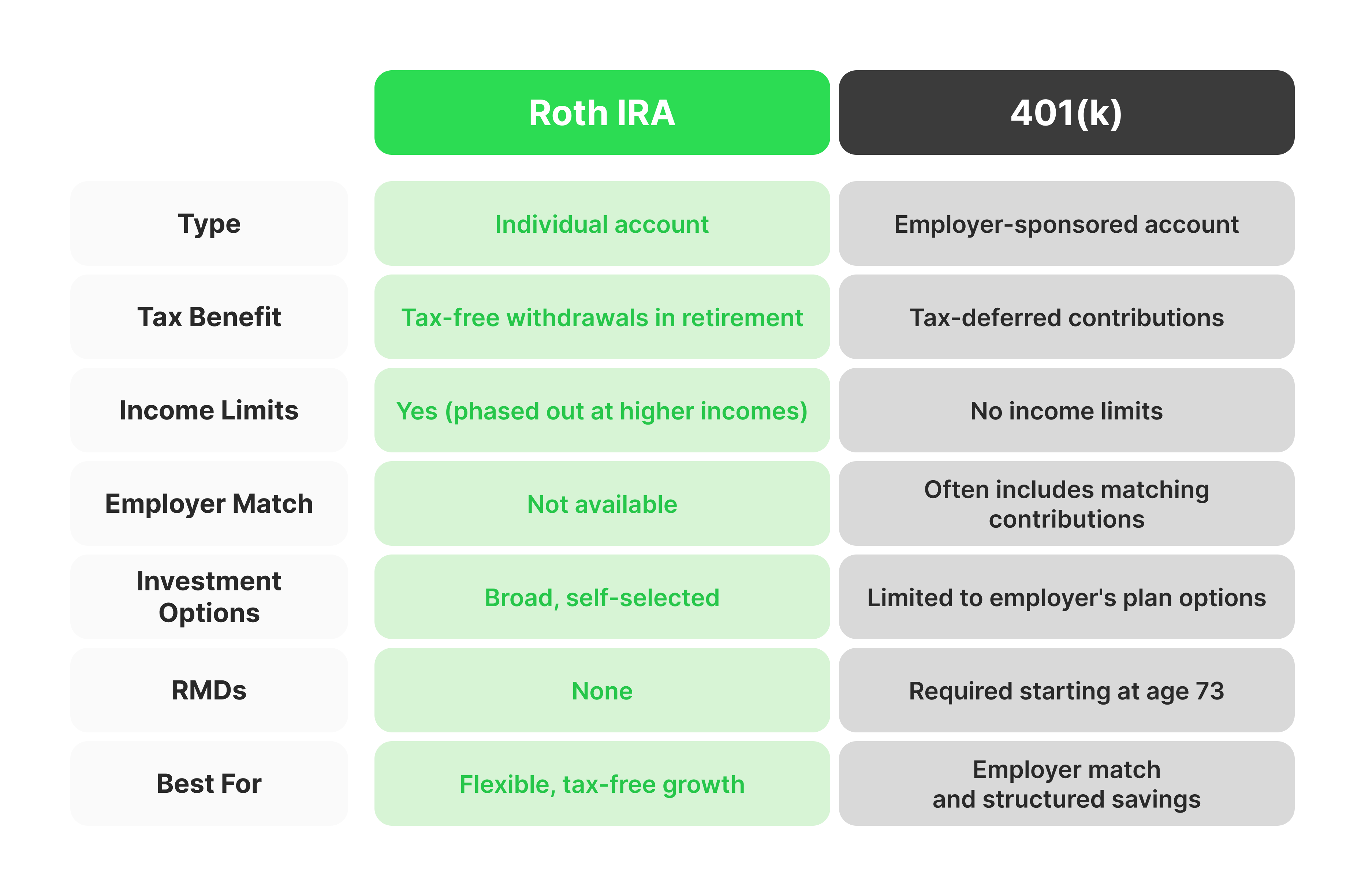

Roth IRA: Tax-Advantaged Retirement Savings

A Roth IRA (Individual Retirement Account) is a retirement savings plan that offers significant tax advantages. Contributions to a Roth IRA are made with after-tax dollars. This means you pay taxes on the money before it goes into the account. However, the benefit is that all qualified withdrawals in retirement, including both contributions and earnings, are tax-free.

Key Features of a Roth IRA:

- Contributions are made with after-tax dollars.

- Qualified withdrawals in retirement are tax-free.

- Earnings and growth within the Roth IRA are tax-free.

- There are income limitations to contribute to a Roth IRA.

- Early withdrawals of contributions are generally tax and penalty-free.

Example: Let’s say you invest $5,000 in a gold ETF within your Roth IRA. Over 30 years, the investment grows to $50,000. When you retire, you can withdraw the entire $50,000 tax-free, assuming you meet the qualified withdrawal requirements (generally, being at least 59 1/2 years old and the account being open for at least five years).

Taxable Account: Standard Investment Account

A taxable account is a standard investment account that does not offer the same tax advantages as a Roth IRA. Investments in a taxable account are subject to taxes on dividends, interest, and capital gains. This means that any profits you earn from selling gold ETFs in a taxable account will be taxed in the year they are realized.

Key Features of a Taxable Account:

- Contributions are made with after-tax dollars.

- Dividends and interest earned are taxable in the year received.

- Capital gains are taxable when the investment is sold.

- No contribution limits or income restrictions (unlike retirement accounts).

- Greater flexibility in withdrawing funds at any time without penalty (though taxes may apply).

Example: You purchase gold ETFs for $5,000 in a taxable account. After several years, you sell the ETFs for $8,000. You have a capital gain of $3,000, which is subject to capital gains tax. The tax rate depends on how long you held the investment (short-term vs. long-term) and your income bracket.

Gold ETF in Roth IRA vs. Taxable Account: A Detailed Comparison

Tax Implications

The most significant difference lies in the tax treatment.

- Roth IRA: No taxes are paid on the gains when the investment is sold in retirement. This is a substantial advantage if you expect the value of your gold ETF to increase significantly over time.

- Taxable Account: Any profits from selling the gold ETF are subject to capital gains tax. The tax rate depends on the holding period:

- Short-term capital gains: Taxed at your ordinary income tax rate (if held for one year or less).

- Long-term capital gains: Taxed at a lower rate, typically 0%, 15%, or 20%, depending on your income (if held for more than one year).

Additionally, within a taxable account, any dividends paid by the gold ETF (although gold ETFs typically don’t pay significant dividends) would be subject to income tax in the year they are received.

Contribution and Withdrawal Rules

Roth IRAs have specific rules regarding contributions and withdrawals.

- Roth IRA: Contributions are limited by annual contribution limits set by the IRS (e.g., $6,500 in 2023, with a catch-up contribution of $1,000 for those age 50 and over). There are also income limitations that may prevent high-income earners from contributing directly to a Roth IRA. Early withdrawals of contributions are tax and penalty-free, but withdrawals of earnings before age 59 1/2 may be subject to taxes and a 10% penalty.

- Taxable Account: There are no contribution limits or income restrictions for taxable accounts. Funds can be withdrawn at any time without penalty, although capital gains taxes may apply if you sell investments at a profit.

Investment Flexibility

Taxable accounts generally offer more investment flexibility.

- Roth IRA: Investment choices within a Roth IRA are typically limited to the options offered by the brokerage firm or custodian. While most major ETFs are available, some specialized investments may not be accessible.

- Taxable Account: Taxable accounts offer a broader range of investment options. Investors can invest in virtually any publicly traded security, including stocks, bonds, ETFs, mutual funds, and options.

Estate Planning

Both Roth IRAs and taxable accounts have implications for estate planning.

- Roth IRA: Roth IRAs can be passed on to beneficiaries. If the beneficiary is a spouse, the Roth IRA can be treated as their own. If the beneficiary is not a spouse, they generally must withdraw the assets within 10 years of the original owner's death (with some exceptions for certain eligible designated beneficiaries). The withdrawals are tax-free to the beneficiary.

- Taxable Account: Assets in a taxable account are included in the estate and may be subject to estate taxes. However, the cost basis of the assets is "stepped up" to the fair market value at the time of death, meaning that beneficiaries will only pay capital gains taxes on any appreciation that occurs after the date of inheritance.

When to Choose a Roth IRA for Gold ETFs

A Roth IRA may be more advantageous for gold ETFs in the following scenarios:

- Long-Term Growth Potential: You believe that the value of gold will increase substantially over the long term. The tax-free growth within a Roth IRA can significantly enhance your returns.

- Expect Higher Future Tax Rates: You anticipate that your tax rate will be higher in retirement than it is now. Paying taxes on contributions now and avoiding taxes on withdrawals later can be beneficial.

- Retirement Savings Focus: You are primarily focused on saving for retirement and want to maximize tax-advantaged growth.

When to Choose a Taxable Account for Gold ETFs

A taxable account may be more suitable for gold ETFs in the following scenarios:

- Need for Liquidity: You may need access to the funds before retirement age. While you can withdraw contributions from a Roth IRA without penalty, withdrawals of earnings may be subject to taxes and penalties.

- Exceed Roth IRA Contribution Limits: You have already maxed out your Roth IRA contributions and want to invest additional funds in gold ETFs.

- Uncertainty about Future Tax Rates: You are unsure whether your tax rate will be higher or lower in retirement.

- Tax-Loss Harvesting: A taxable account allows for tax-loss harvesting, which involves selling investments at a loss to offset capital gains taxes. This strategy is not available within a Roth IRA.

Practical Advice and Insights

Before deciding where to hold your gold ETF investments, consider the following practical advice:

- Diversify Your Investments: Don't put all your eggs in one basket. Gold ETFs should be part of a diversified portfolio that includes stocks, bonds, and other asset classes.

- Consider Your Investment Timeline: How long do you plan to hold the gold ETF? If you have a long-term investment horizon, a Roth IRA may be more beneficial.

- Evaluate Your Risk Tolerance: Gold can be a volatile asset. Make sure you are comfortable with the level of risk associated with investing in gold ETFs.

- Consult a Financial Advisor: A financial advisor can help you assess your individual circumstances and develop a personalized investment strategy.

- Monitor Your Investments: Regularly review your portfolio and make adjustments as needed to ensure it aligns with your financial goals.

Ultimately, the decision of whether to hold gold ETFs in a Roth IRA or a taxable account depends on your individual financial situation, investment goals, and risk tolerance. By carefully considering the tax implications, contribution and withdrawal rules, and investment flexibility of each option, you can make an informed decision that aligns with your long-term financial success.

:max_bytes(150000):strip_icc()/savingsvs.ira_V1-b63b805de8554f589543be193cad9857.png)