Fine Print Credit Report Answer Key

Okay, let's talk about something that might sound about as exciting as watching paint dry: your credit report. I know, I know, bear with me! But trust me, understanding your credit report and especially the "answer key" – what's really going on in that document – is like unlocking a cheat code to a better financial life. And who doesn't want that, right?

Why Should You Even Care About This "Fine Print" Stuff?

Think of your credit report as your financial report card. Lenders, landlords, even some employers, use it to gauge how responsible you are with money. A good credit report means better interest rates on loans (hello, dream house!), easier approvals for rentals, and generally more financial opportunities. A not-so-great report? Well, it can make things…trickier. Which is exactly why you want to be in the know about everything on it.

But here's the thing: credit reports are dense! They’re filled with jargon, codes, and numbers that can make your head spin. That's where understanding the fine print, and finding the "answer key," comes in. It's about deciphering the mystery and taking control of your financial destiny! Pretty dramatic, huh? But it's true!

Must Read

Deciphering the Credit Report Alphabet Soup: The Key Players

First things first, you need to know who is keeping track of all this information. The three main credit bureaus in the US are: Equifax, Experian, and TransUnion. These guys are like the scorekeepers of your financial life.

Each bureau collects information from your creditors (banks, credit card companies, etc.) and compiles it into your credit report. It's crucial to check all three reports because they might contain slightly different information. Why? Because not all creditors report to all three bureaus. Makes sense? Hopefully!

What's Actually On Your Credit Report?

Okay, so what kind of dirt (or gold!) is being tracked? Here’s the breakdown:

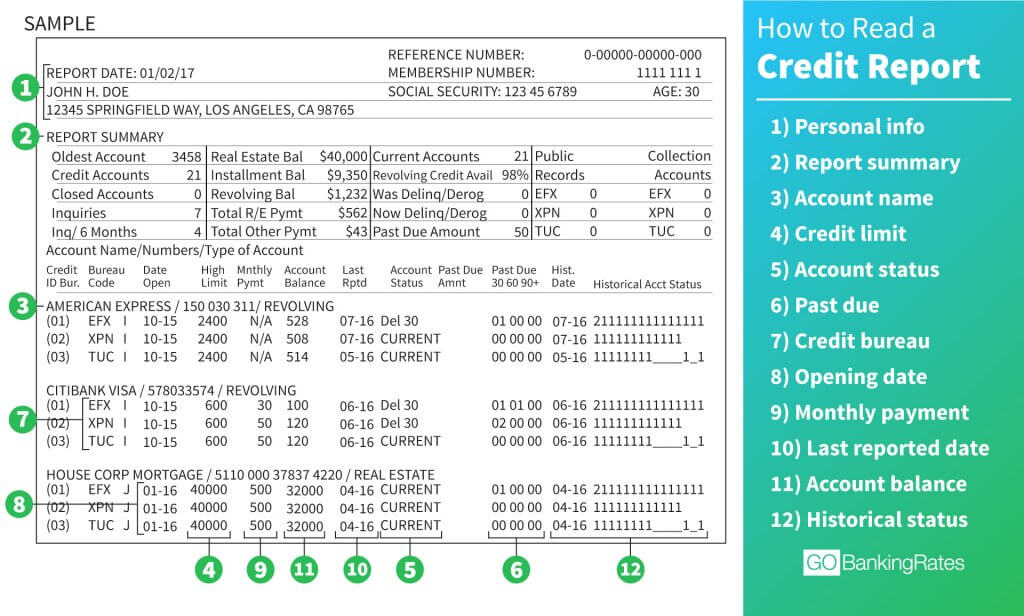

- Personal Information: This is the basic stuff: your name, address, Social Security number, and date of birth. Make sure this information is accurate! Even a small error can cause problems.

- Credit Accounts: This is the heart of your credit report. It lists all your credit cards, loans (student loans, auto loans, mortgages), and other lines of credit. For each account, it shows the creditor's name, account number, credit limit/loan amount, payment history, and current balance.

- Payment History: This is the most important factor in your credit score. It shows whether you've been paying your bills on time. Late payments can seriously ding your credit score.

- Public Records: This section includes information from public records, such as bankruptcies, tax liens, and judgments.

- Inquiries: This lists who has accessed your credit report. There are two types of inquiries: hard inquiries (which can slightly lower your score) and soft inquiries (which don't affect your score). Hard inquiries typically happen when you apply for credit.

The "Answer Key": Decoding the Credit Report Jargon

Alright, now for the fun part – deciphering the code! Let’s break down some common credit report terms and what they really mean:

- Account Status: This tells you the current state of your account. Common statuses include:

- Current: You're up-to-date on your payments. Good job!

- Late (30, 60, 90+ days): You're behind on your payments. This is a red flag to lenders. The longer you're late, the worse it looks.

- Charged Off: The creditor has given up on collecting the debt and written it off as a loss. This doesn't mean you don't owe the money! It just means they've stopped trying to collect it directly. It severely damages your credit.

- In Collections: The creditor has sold your debt to a collection agency, who will now try to collect it. This is also bad news for your credit.

- Closed: The account is no longer active. This can be a good thing (if you paid it off) or a bad thing (if it was closed due to non-payment).

- Credit Limit/Original Loan Amount: This is the maximum amount you can borrow on a credit card or the original amount of a loan.

- Current Balance: This is how much you currently owe on the account.

- Past Due Amount: This is the amount you're behind on your payments.

- Date Opened: The date the account was opened.

- Date Reported: The date the creditor last reported information to the credit bureau.

- High Credit: The highest balance you've ever had on a credit card.

See? It's not so scary once you understand the lingo. Think of it as learning a new language – the language of credit!

Finding Errors and Disputing Them (Your Secret Weapon!)

Here's a critical piece of the puzzle: errors on your credit report are more common than you might think! Studies show that a significant percentage of credit reports contain inaccuracies. That's why it's essential to review your reports carefully and dispute any errors you find.

What kind of errors should you look for?

- Incorrect personal information: Wrong name, address, or Social Security number.

- Accounts that don't belong to you: Fraudulent accounts opened in your name.

- Incorrect payment history: Payments marked as late when you paid on time.

- Duplicate accounts: The same account listed multiple times.

- Incorrect credit limits or loan amounts: The credit limit or loan amount is different from what you actually agreed to.

- Accounts that should have been closed but are still open.

How to Dispute Errors:

- Gather evidence: Collect any documents that support your claim, such as bank statements, payment confirmations, or credit card agreements.

- Write a dispute letter: Clearly explain the error and why you believe it's incorrect. Include copies of your supporting documents.

- Send the dispute letter to the credit bureau: Send the letter by certified mail with return receipt requested so you have proof that they received it.

- The credit bureau has 30 days to investigate: They will contact the creditor to verify the information.

- The credit bureau will notify you of the results: If the error is verified, they will correct your credit report.

Disputing errors can be a bit of a process, but it's absolutely worth it. Correcting even one small error can significantly improve your credit score. It's like finding a typo in your resume – you want to fix it, right?

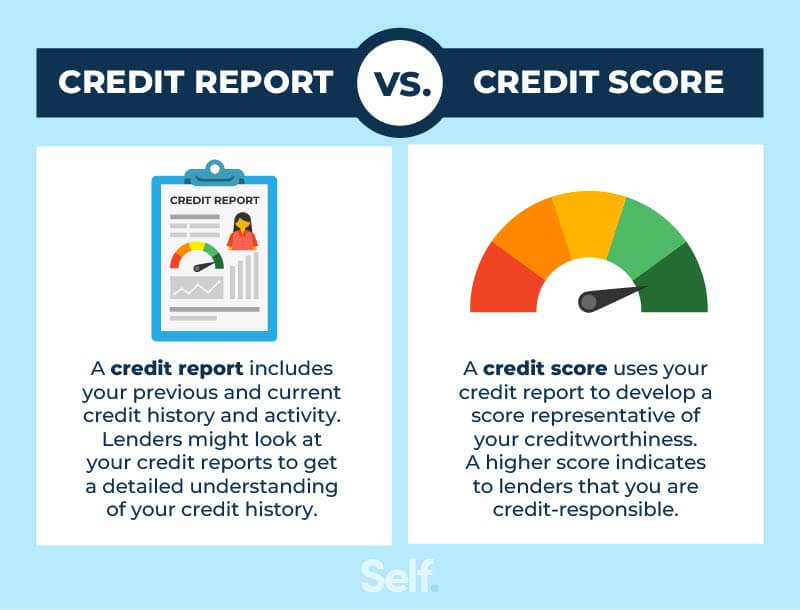

Beyond the Report: Understanding Your Credit Score

Your credit report is the foundation for your credit score. Your credit score is a three-digit number that summarizes your creditworthiness. Lenders use it to quickly assess your risk.

The most common credit scoring model is FICO. FICO scores range from 300 to 850, with higher scores being better.

What factors influence your FICO score?

- Payment History (35%): This is the most important factor. Pay your bills on time!

- Amounts Owed (30%): This is your credit utilization ratio (the amount of credit you're using compared to your total available credit). Keep your credit utilization low (ideally below 30%).

- Length of Credit History (15%): The longer you've had credit, the better.

- Credit Mix (10%): Having a mix of different types of credit (credit cards, loans) can be beneficial.

- New Credit (10%): Opening too many new accounts in a short period of time can lower your score.

Pro Tip: Get Your Free Credit Reports!

You are entitled to a free credit report from each of the three major credit bureaus every 12 months. You can access them at AnnualCreditReport.com. This is the official website authorized by the US government. Don't fall for scam sites that try to sell you something!

Set a reminder to check your credit reports regularly. It's like getting a regular checkup for your financial health.

Making Credit Work For You: It's All About Control!

Understanding your credit report and score isn't just about avoiding mistakes. It's about proactively managing your credit to achieve your financial goals. Think of it this way: you're not just reacting to your credit; you're actively building it, shaping it, and using it as a tool to achieve your dreams.

Here are a few tips for building good credit:

- Pay your bills on time, every time. Set up automatic payments if needed.

- Keep your credit utilization low. Don't max out your credit cards.

- Don't open too many new accounts at once.

- Consider becoming an authorized user on someone else's credit card (if they have good credit).

- If you have trouble managing credit, consider a secured credit card.

The Takeaway: You Got This!

Learning about credit reports and scores might seem daunting at first, but it's a skill that will pay off for the rest of your life. By understanding the "fine print" and taking control of your credit, you can unlock a world of financial opportunities and achieve your dreams. It's like mastering a challenging game – once you know the rules, you can play to win!

So, go forth and conquer your credit report! You've got the knowledge, you've got the tools, and you've got the power to create a brighter financial future. And remember, it's okay to ask for help along the way. There are plenty of resources available to guide you on your journey. Now, go get 'em!