Does Cosigning Affect Your Credit Score

Hey there, friend! Ever been asked to cosign a loan? Maybe for a sibling's car or a friend's apartment? It seems like a nice thing to do, right? But wait! Let's talk about whether cosigning affects your credit score. Buckle up; it's more interesting than you think!

Cosigning 101: What's the Deal?

So, what exactly is cosigning? Think of it like this: you're basically saying, "Hey lender, I trust this person. And if they don't pay, I will!" You're adding your creditworthiness to their application. You're their financial superhero… or maybe their financial safety net.

Why do people need cosigners? Usually, it's because they have thin credit (not much credit history), bad credit, or not enough income. Lenders want assurance they'll get their money back. That's where you come in! You're the guarantor. It's a big responsibility!

Must Read

The Credit Score Rollercoaster: Does Cosigning Affect It?

Okay, the big question: does cosigning impact your credit score? Short answer: yes! But here's the thing: it's complicated. It can affect it positively, negatively, or not at all (though that's rare).

The Good, the Bad, and the Ugly

Let's start with the good (because we're optimists, right?). If the borrower makes all their payments on time, it could potentially help your credit. The loan appears on your credit report as if it were your own. Consistent, on-time payments? Credit score boost! Hooray!

Now, for the bad. Missed payments? Ouch. Those will ding both the borrower's and your credit score. Even one late payment can have a significant impact. It's like a domino effect… a bad credit domino effect.

And the ugly? If the borrower defaults (stops paying altogether), you're on the hook for the entire loan amount. That's potentially thousands of dollars! Plus, your credit score will take a major hit. Collection agencies might come knocking. Foreclosure could even become an issue depending on the nature of the loan. It's a scary thought.

Here's a quirky fact: Did you know that cosigning a loan makes you equally responsible as the primary borrower? It's not just a formality! It's a legally binding agreement. Always read the fine print!

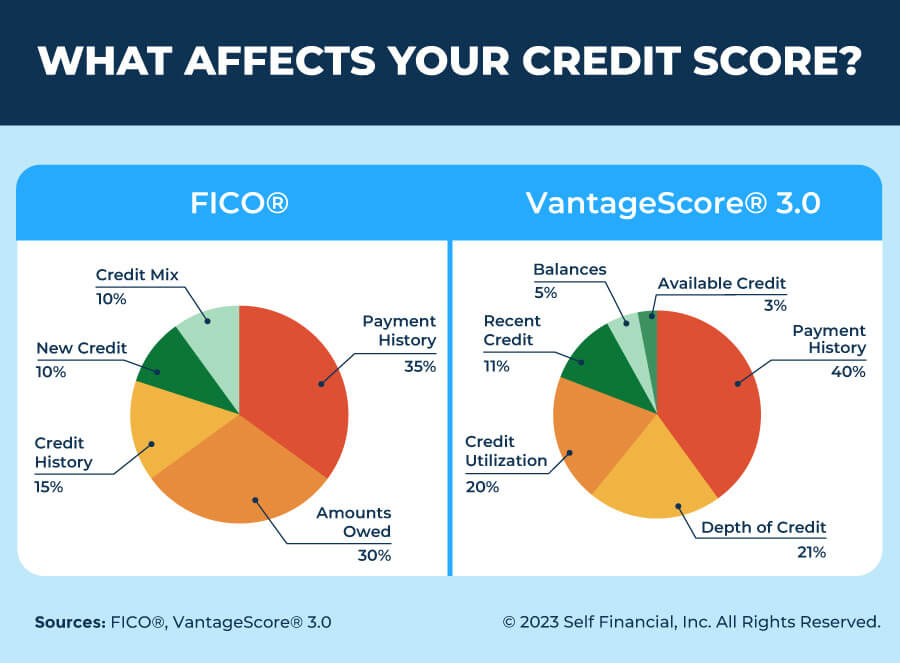

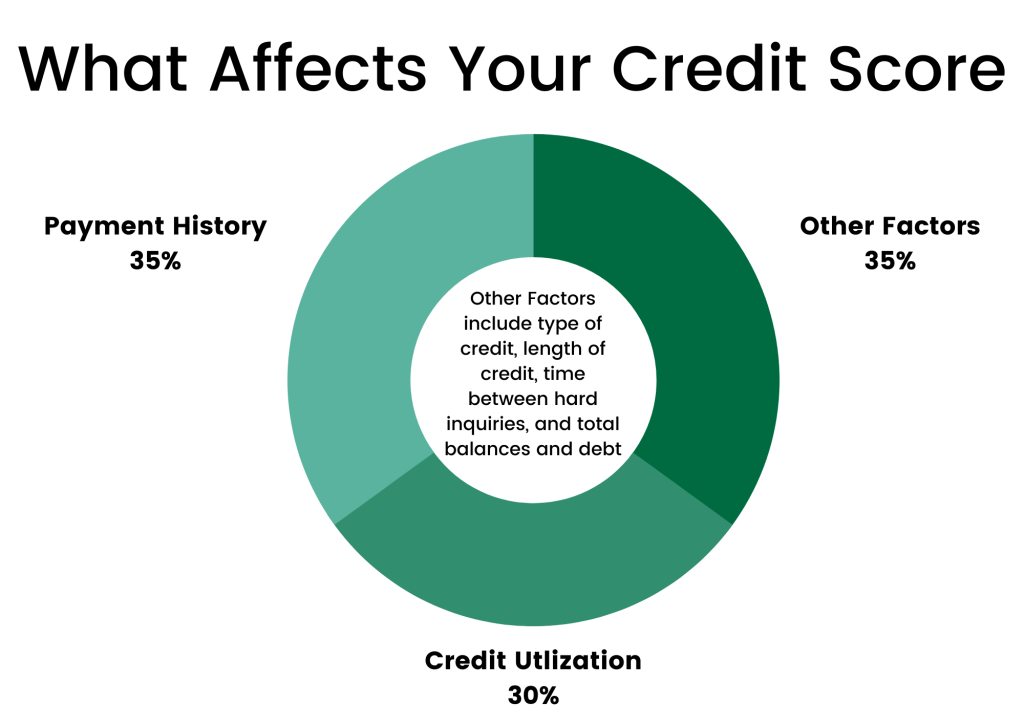

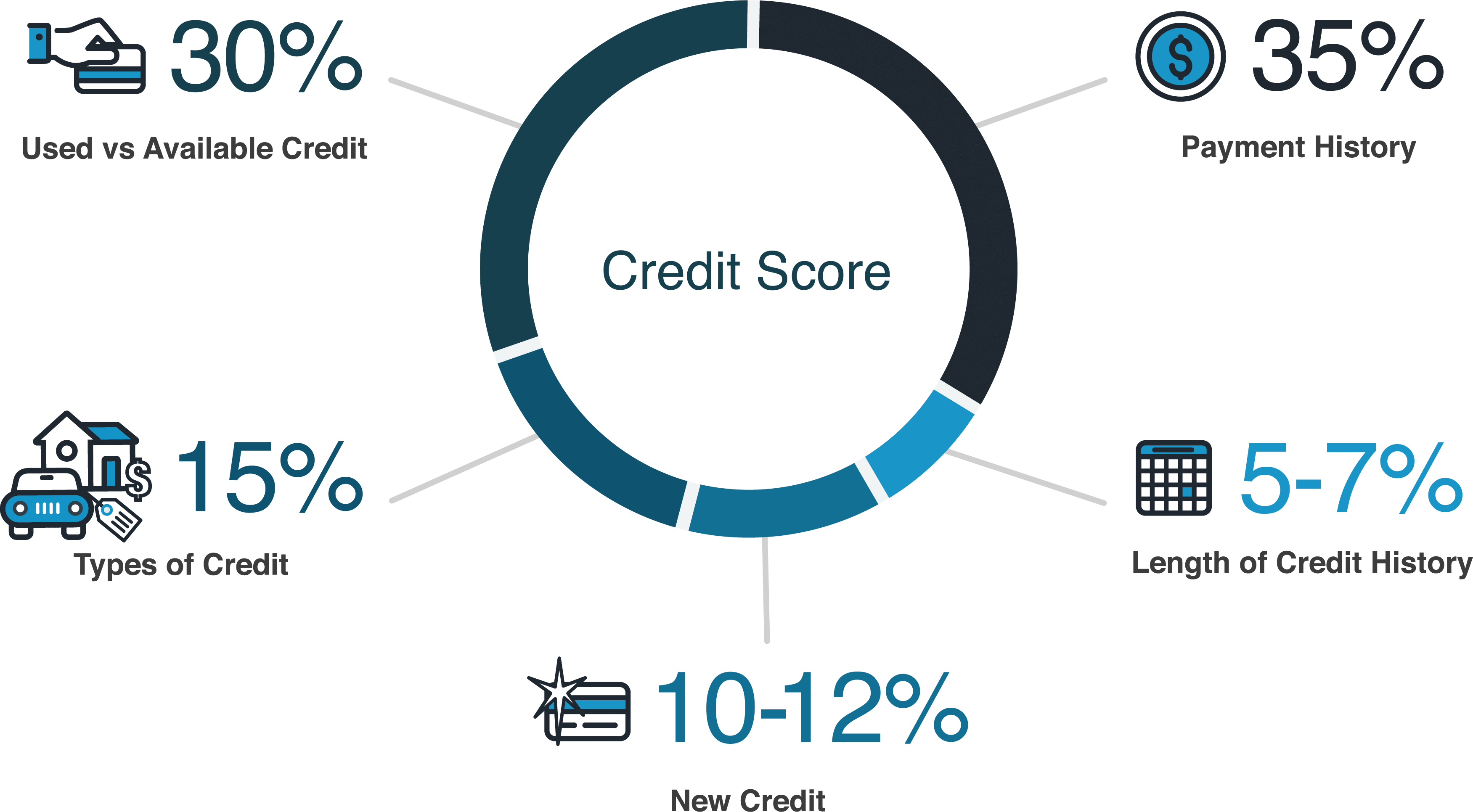

The Credit Bureau Breakdown

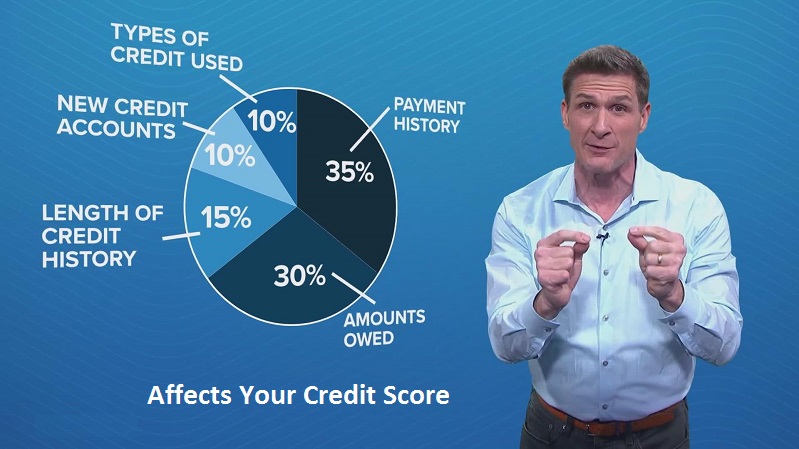

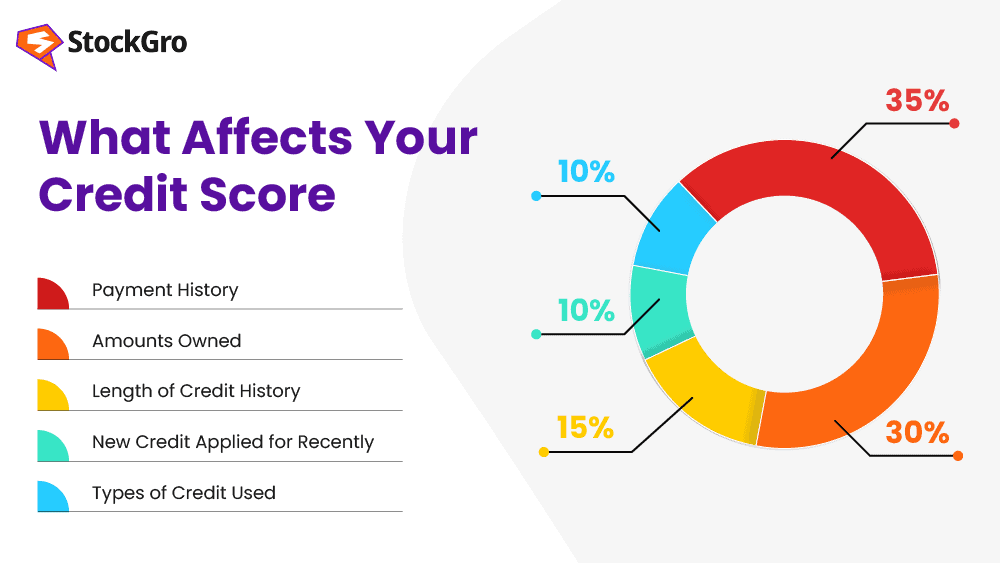

Your credit report is like your financial report card. The three major credit bureaus (Experian, Equifax, and TransUnion) track all your credit activity. When you cosign, the loan typically appears on your credit report as well as the borrower's. This means that it impacts your:

- Payment history: This is the biggest factor in your credit score. Late payments hurt!

- Amounts owed: The loan balance adds to your overall debt.

- Credit utilization ratio: This is the amount of credit you're using compared to your total available credit. A high credit utilization ratio can lower your score.

Think of it like a seesaw. Your credit score is balanced. Cosigning adds weight to one side. Will it tip in a good way, or a bad way? It all depends on the borrower's payment habits.

Beyond the Score: Other Considerations

It's not just about your credit score. Cosigning can impact other areas of your financial life. Consider this:

Your Debt-to-Income Ratio (DTI)

Your DTI is the percentage of your gross monthly income that goes towards paying debts. Lenders look at this when you apply for a loan. Cosigning adds to your debt obligations, which can make it harder to get approved for your own loans, like a mortgage or car loan. It might affect the amount you can borrow or the interest rate you receive.

Your Peace of Mind

Let's be honest. Cosigning can be stressful. You're essentially putting your financial reputation on the line. Are you prepared to potentially pay the loan if the borrower can't? Are you okay with the possibility of strained relationships if things go south? These are tough questions to ask. Think about it long and hard.

Potential Legal Trouble

In a worst-case scenario, if the borrower defaults and you can't pay, you could face legal action. The lender might sue you to recover the debt. This could lead to wage garnishment or even the seizure of assets. Always get legal advice before cosigning anything!

Cosigning Quiz: Are You Ready?

Before you say "yes" to cosigning, ask yourself these questions:

- Do I trust this person implicitly?

- Can I afford to pay the loan if they can't?

- Have I reviewed the loan agreement carefully?

- Have I considered all the risks involved?

- Would I be okay with potentially damaging our relationship?

If you answered "no" to any of these questions, it might be best to politely decline. It's better to protect your credit and your peace of mind.

Alternatives to Cosigning

Want to help a friend or family member without putting your credit on the line? Consider these alternatives:

- Offer financial advice: Help them create a budget and improve their credit score.

- Give them a small loan: Offer a small, manageable loan that you're comfortable with losing.

- Help them find resources: Connect them with credit counseling services or financial assistance programs.

The Bottom Line

Cosigning a loan is a serious decision. It can affect your credit score, your debt-to-income ratio, and your overall financial well-being. Weigh the risks and benefits carefully. Talk to a financial advisor if you're unsure. And remember, saying "no" is perfectly acceptable. Your financial health is important!

So, there you have it! The scoop on cosigning and your credit score. Hopefully, this has helped you understand the potential impacts. Now go forth and make informed decisions! And remember, being financially savvy is always a good look!

:max_bytes(150000):strip_icc()/how-opening-a-new-credit-card-affects-your-credit-score-96050-final-5b60bade46e0fb0025b3bc98.png)