Does A Soft Credit Check Show Defaults

Hey there! Ever wondered about those sneaky little soft credit checks? Like, what secrets are they spilling? Specifically, do they reveal the skeletons in your financial closet – those dreaded defaults?

Let's dive in! Think of credit reports like gossip columns for your money habits. But not all gossip is created equal. Some is juicy, detailed, and a little embarrassing. Other gossip is… watered down. So, is a soft pull like whispering a secret or shouting it from the rooftops?

The Great Credit Check Divide: Soft vs. Hard

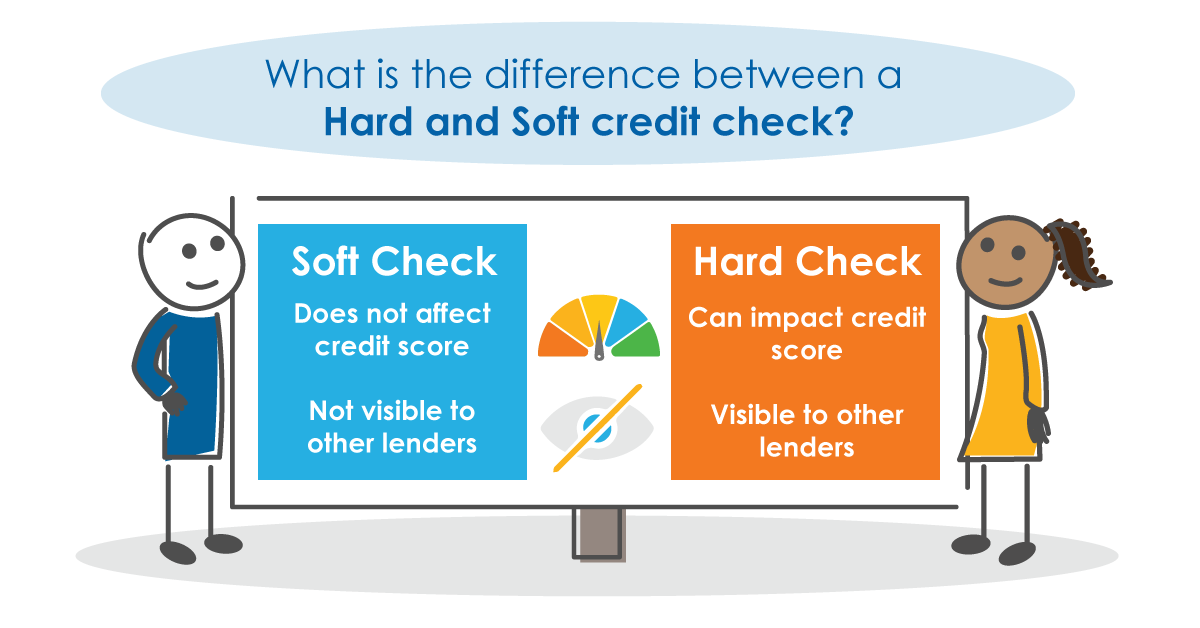

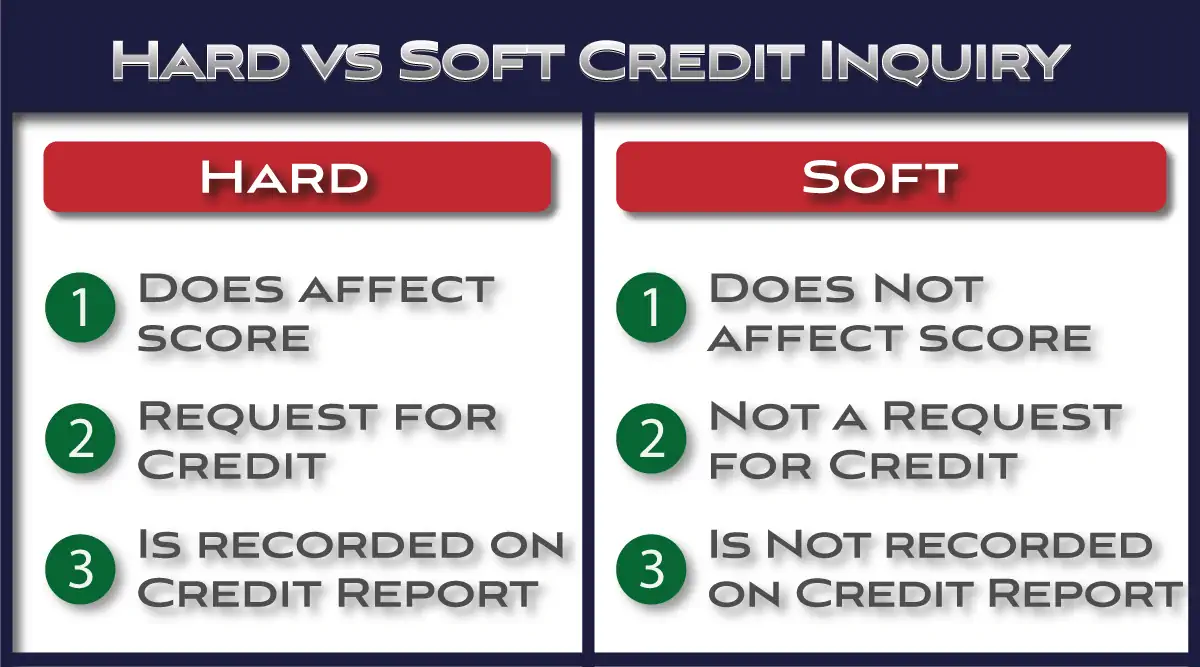

Okay, quick crash course. There are two main types of credit checks: soft and hard. It’s like the difference between a friendly pat on the back and a full-body security scan. Hard inquiries are the serious ones. They happen when you apply for credit: a loan, a credit card, that shiny new car.

Must Read

These hard inquiries do affect your credit score. Too many of them in a short time can make you look desperate for credit. And nobody wants to look desperate, right?

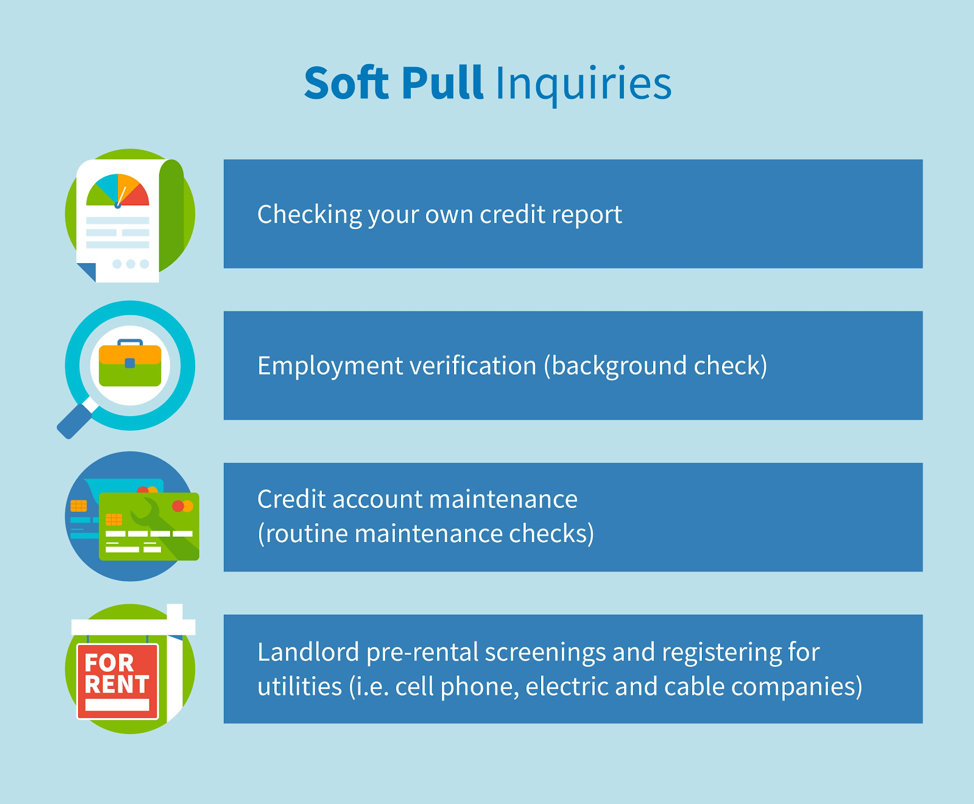

Now, soft inquiries are the chill cousins. They're used for background checks, pre-approved offers, and when you check your own credit. The best part? They don't ding your score. Phew!

So, What About Defaults? The Juicy Details.

Here's the million-dollar question: do soft credit checks show defaults? The answer is… well, it's a bit nuanced.

Generally speaking, soft credit checks can see some information related to your credit history, but not all of it. They can often see your payment history. They can see credit accounts. They can see amounts owed.

Think of it like this: a soft pull might show that you have a credit card with a balance. But it might not show whether you’re consistently late on your payments, or if that credit card is currently in default.

Defaults are serious red flags. They basically scream, "I couldn't pay my bills!" They can seriously damage your credit score and haunt you for years. Lenders definitely want to know about them.

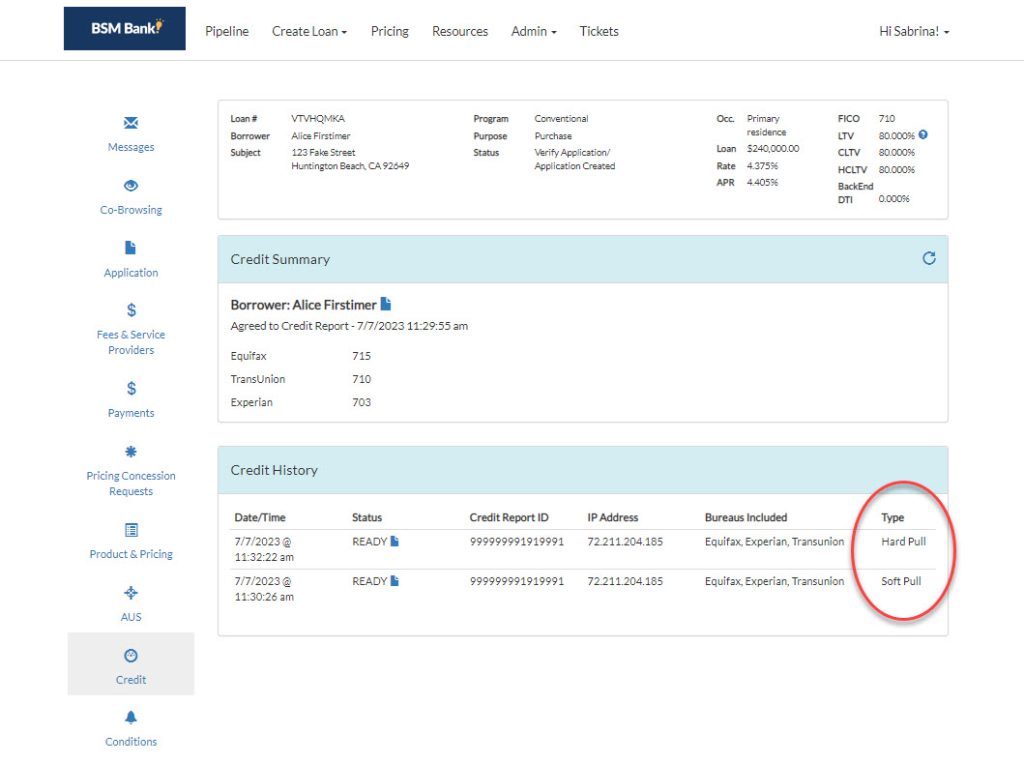

Hard credit checks almost always reveal defaults. These checks are more comprehensive. They pull the full credit report, including all the bad stuff.

Here's where it gets a little trickier. Some soft pulls might show if an account is in collections. Being in collections is a close relative to default. It means you failed to pay a debt, and the creditor sold it to a collections agency.

So, while a soft pull might give a hint of a default, it usually won't spell it out in bold letters. It's more like a subtle eyebrow raise than a full-on accusation.

Why Does It Matter? Understanding the Context

Okay, so why should you care if a soft credit check shows defaults or not? Well, it all depends on who is pulling your credit and why.

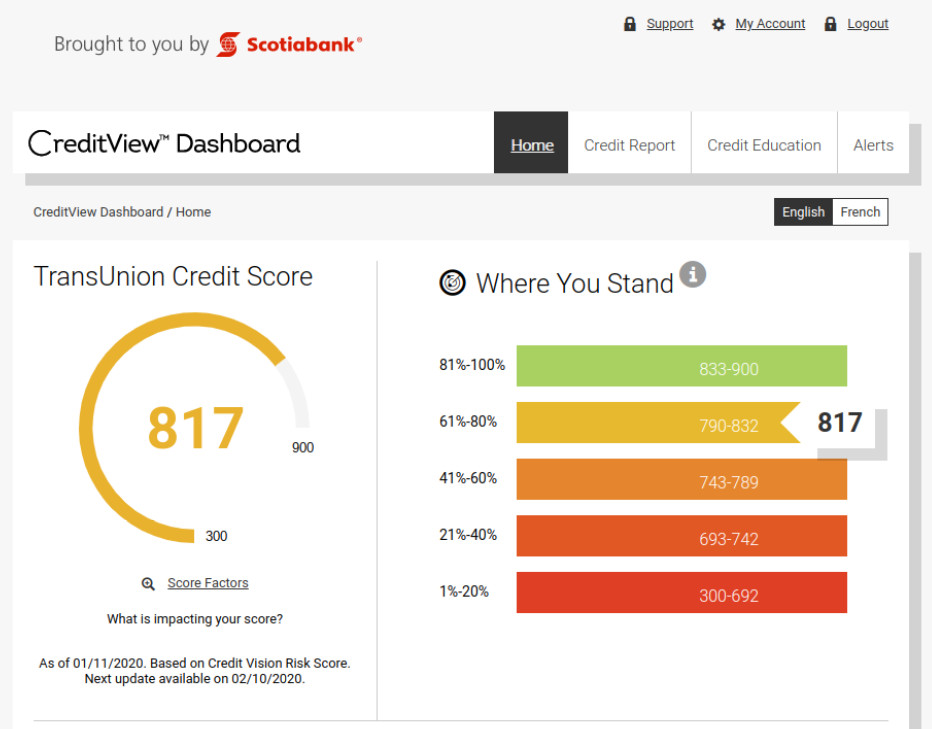

For you: Checking your own credit with a soft pull is a great way to monitor your credit health without hurting your score. You can spot errors, track your progress, and generally stay informed. It's like giving your financial life a little check-up.

If you're worried about defaults showing up, a soft pull can give you a general idea of what lenders might see. But remember, it's not the full picture.

For lenders: Lenders use credit checks to assess risk. They want to know if you're likely to repay a loan. They want to know if you are trustworthy.

For applications, pre-approval credit checks are soft pulls. These are really to check what interest rate they could tentatively offer.

For example, imagine you're applying for a mortgage. The lender will definitely do a hard credit check. They want to see everything, including any defaults. No hiding allowed!

For employers: Some employers might run a soft credit check as part of a background check. This is more common in certain industries, like finance or security. They're not necessarily looking for defaults, but they might be looking for signs of financial irresponsibility.

Fun Fact: Credit Scores Aren't Everything!

Here's a little secret: your credit score isn't the only thing that matters. Lenders also consider other factors, like your income, employment history, and debt-to-income ratio.

Think of it like dating. Your credit score is like your profile picture. It's the first thing people see. But your personality, your job, and your ability to hold a conversation (aka manage your finances) are just as important!

So, even if you have a few blemishes on your credit report (like a past default), you can still get approved for credit. It might just take a little extra effort and some good financial habits.

The Bottom Line: Soft Checks Are Vague, Hard Checks Are Explicit

Let's recap. Soft credit checks generally don't show defaults directly. They might show hints or related information, but they're not as comprehensive as hard credit checks.

Hard credit checks pull your full credit report, including defaults. These are the checks that lenders use when you apply for credit.

So, if you're just curious about your credit health, a soft pull is your friend. If you're applying for credit, be prepared for a hard pull and make sure your financial house is in order.

Remember to always check your credit reports regularly from all three major credit bureaus - Equifax, Experian and TransUnion. You can get free reports from annualcreditreport.com.

And finally, managing your money is about having good spending habits. A good credit score is just a bi-product of good financial habits.

Happy credit checking!

![What is a soft credit check? Soft inquiries explained [2024]](https://www.stilt.com/wp-content/uploads/2023/11/Soft-Inquiry-vs.-Hard-Inquiry-1024x576.png)