Does A Returned Check Affect Credit

:max_bytes(150000):strip_icc()/returned-checks-overview-315276-finalv1-99e973d4a8234bcab3b1973d13f77c64.jpg)

Hey! So, we're chatting about returned checks today, right? Specifically, whether those bouncy little fellas can mess with your precious credit score. Grab your coffee (or maybe something stronger, depending on your past check-bouncing experiences!), because we're diving in.

The Big Question: Does a Returned Check Hurt Your Credit?

Okay, let's get the straight answer out of the way first: Generally, a single returned check won't directly torpedo your credit score. Phew! But, BUT! (There’s always a but, isn't there?) That doesn’t mean you’re totally in the clear. Think of it like this: a returned check itself isn't reported to the major credit bureaus (Equifax, Experian, and TransUnion). It's not like they have a special "Returned Check" section on your credit report, marking you for all eternity.

So, why the big fuss then? Well, the problem isn't the check itself. It's what happens AFTER the check bounces. That’s where things can get a little… sticky.

Must Read

How a Returned Check Can Indirectly Hurt Your Credit

Imagine this: you write a check to pay your electric bill. But oops! You forgot about that online shopping spree (we’ve all been there, right?), and your account is short on funds. The check bounces. What happens next?

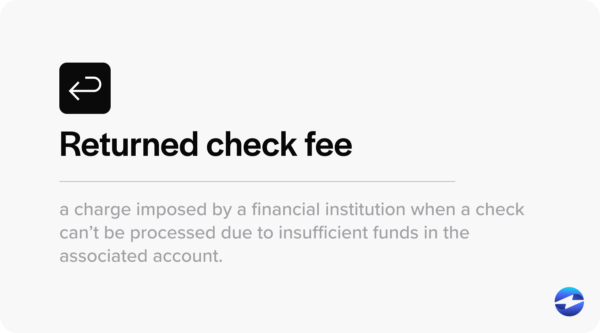

First, the electric company probably isn't going to be thrilled. They'll likely charge you a fee for the returned check. And honestly, who can blame them? They were expecting money, and they got... nothing. Nada. Zilch!

But here’s where it gets credit-relevant: if you don't pay the electric bill (plus the returned check fee!), the electric company might eventually send your account to a collection agency. And guess what they do? Yep, they often report the unpaid debt to the credit bureaus.

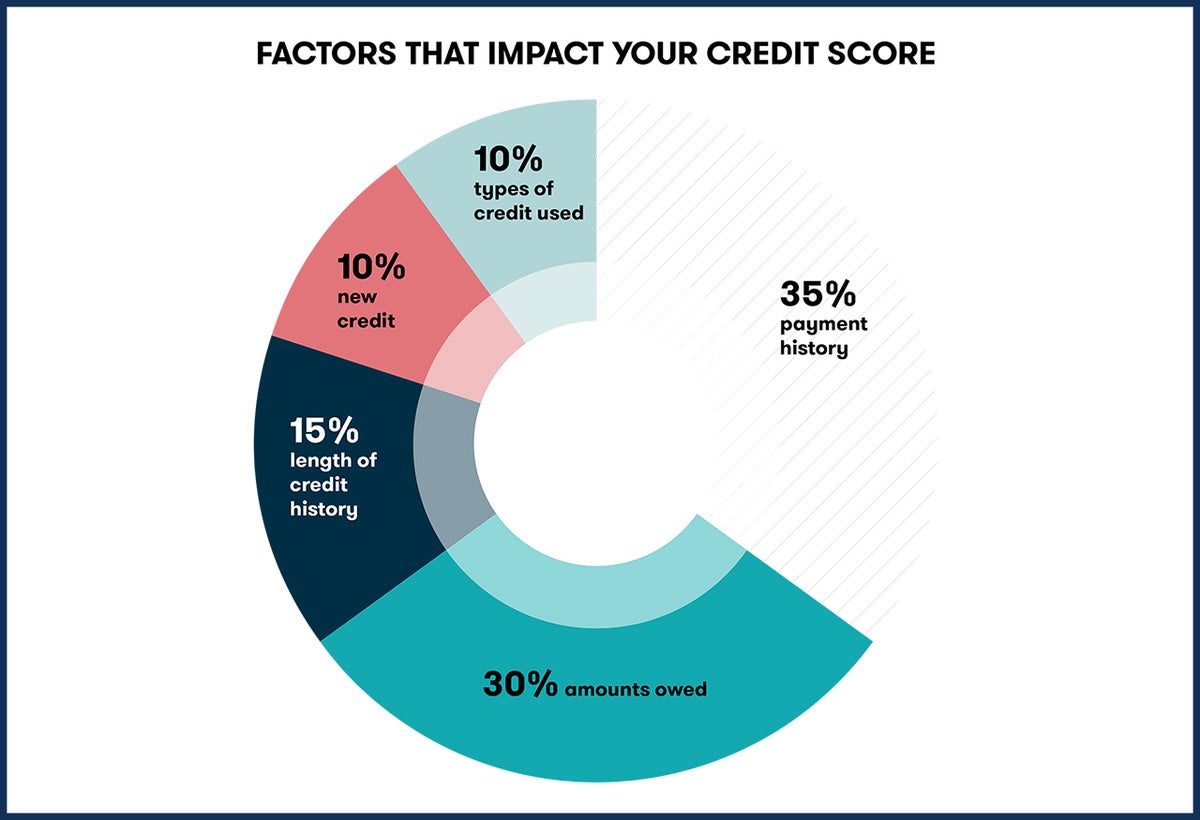

A collection account on your credit report is a major red flag. It can significantly lower your credit score. We're talking potentially a drop of dozens, even hundreds, of points, depending on your credit history. Ouch!

Think of it like a domino effect. The bounced check is just the first domino. If you don't address the issue, it can knock over a whole line of dominoes, ultimately leading to a damaged credit score. Not fun.

What About Other Types of Checks?

Okay, so we talked about utility bills. But what about other situations? Does it matter who you wrote the check to? The short answer is... mostly, no. The principle is the same, whether you bounced a check to your landlord, your dentist, or your local pizza joint (though, let's be honest, bouncing a check to the pizza place feels extra-shameful, doesn't it?).

:max_bytes(150000):strip_icc()/a-man-writing-a-check-for-78765999-573355703df78c6bb079a326.jpg)

If you don't resolve the issue, whoever you wrote the check to could eventually send the debt to collections. And that's what you want to avoid.

The Exception: Check Verification Services

Now, here’s a slightly less common, but still important, scenario. Some businesses use check verification services. These services track bounced checks and can deny you the ability to pay by check at participating merchants in the future. This doesn't directly affect your credit score, but it can make your life significantly more inconvenient.

Imagine trying to pay for groceries with a check, and the cashier says, "Sorry, your check has been flagged by our verification service." Awkward! And it means you're stuck paying with cash or a card. Annoying, right?

So, What Can You Do? (Prevention and Damage Control!)

Alright, so we’ve established that bounced checks, while not directly impacting your credit, can lead to problems that definitely will. So, what can you do to avoid this whole mess in the first place? And what should you do if you've already bounced a check?

Prevention is Key:

- Track Your Spending: This seems obvious, but seriously, know where your money is going! Use a budgeting app, a spreadsheet, or even just a good old-fashioned notebook. Awareness is half the battle.

- Monitor Your Bank Account: Check your balance regularly. Don’t just assume you have enough money. Double-check! Especially before writing a check or scheduling an online payment.

- Set Up Overdraft Protection: Many banks offer overdraft protection, which can cover you if you accidentally overdraw your account. It usually involves linking your checking account to a savings account or a line of credit. There are often fees involved, so weigh the cost versus the potential headache of a bounced check.

- Consider Using Online Bill Pay: Automate your bill payments! This can help you avoid forgetting to pay bills and accidentally bouncing a check due to insufficient funds. Just make sure you have enough money in your account when the payment is scheduled.

Damage Control (You Already Bounced a Check!):

- Act Fast: As soon as you realize you bounced a check, contact the recipient (the person or company you wrote the check to). Explain the situation and apologize (sincerity goes a long way!).

- Make Immediate Payment: Pay the original amount of the check plus any returned check fees as quickly as possible. Use a method that guarantees immediate payment, like a credit card, debit card, or money order. Don't write another check!

- Get Confirmation: Once you've made the payment, get written confirmation from the recipient that the debt is satisfied and that they won't be pursuing further action (like sending the debt to collections). This is crucial!

- Monitor Your Credit Report: Even if you think you've resolved the issue, check your credit report regularly (you can get a free copy from each of the major credit bureaus once a year at AnnualCreditReport.com). Look for any new collection accounts. If you see one related to the bounced check, dispute it immediately with the credit bureau.

Disputing a Collection Account

Speaking of disputes, let's say you find a collection account on your credit report that you believe is inaccurate (maybe you did pay the bill, but the collection agency didn't get the memo). Here’s how to dispute it:

- Gather Your Evidence: Collect any documentation that supports your claim, such as proof of payment, bank statements, or correspondence with the original creditor.

- Write a Dispute Letter: Send a written dispute letter to the credit bureau that's reporting the inaccurate information. You can find templates online. Be clear and concise, and include copies (not originals!) of your supporting documentation.

- Send the Letter via Certified Mail: This gives you proof that the credit bureau received your dispute.

- Follow Up: The credit bureau has 30 days to investigate your dispute. They'll contact the creditor to verify the information. If the information is found to be inaccurate, the credit bureau must remove it from your credit report.

The Bottom Line (Because We All Need One!)

So, to recap: a bounced check itself doesn't directly hurt your credit score. But failing to address the underlying debt can lead to collection accounts, which definitely will damage your credit. Think of it as a slippery slope! Avoid bouncing checks whenever possible by tracking your spending and monitoring your bank account. And if you do bounce a check, act quickly to resolve the issue and prevent it from turning into a credit-damaging nightmare.

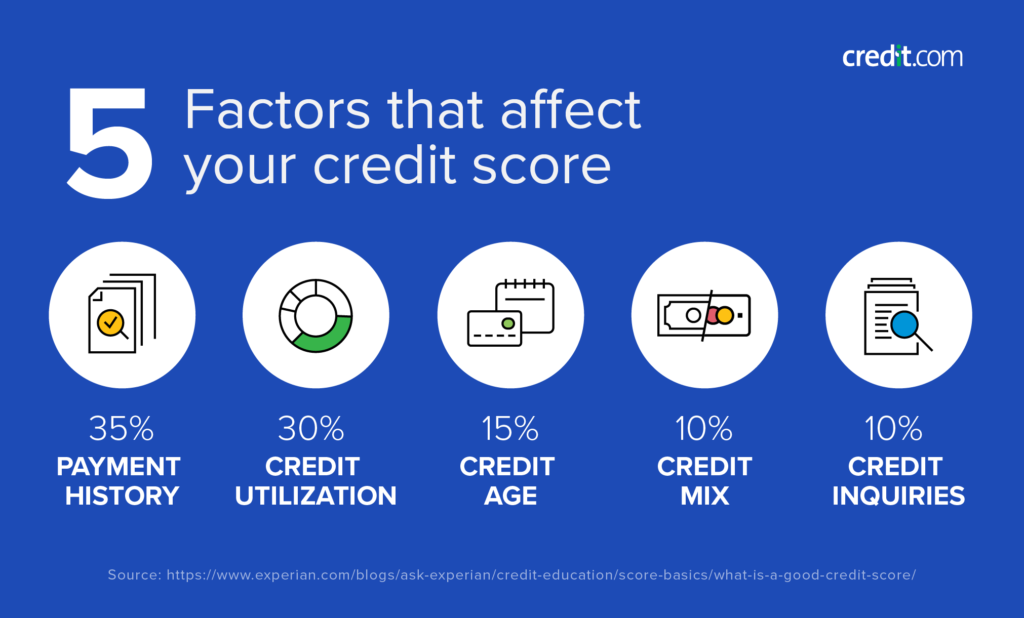

Ultimately, managing your finances responsibly is the best way to protect your credit. Pay your bills on time, keep your credit utilization low, and monitor your credit report regularly. Your credit score will thank you for it!

Now, go forth and conquer your financial world! And maybe double-check your bank balance before you order that extra-large pizza. Just sayin'. 😉

:max_bytes(150000):strip_icc()/how-opening-a-new-credit-card-affects-your-credit-score-96050-final-5b60bade46e0fb0025b3bc98.png)