Do Payday Loans Show On Credit Report

Okay, picture this: it's Friday afternoon, your stomach's rumbling, and payday is so close you can almost taste that celebratory pizza. But then… BAM! The car decides to throw a tantrum and needs a sudden, expensive repair. Cue the internal screaming and frantic calculations. This is where the dreaded thought of a payday loan creeps in, right? We've all been there (or know someone who has!). But the big question looming in the background is: will this little financial fix mess with my precious credit score?

The short answer is: it depends. But, because life is rarely that simple, let's dive deeper into the complicated world of payday loans and credit reports. Because, let's be honest, understanding your credit score is like deciphering ancient hieroglyphics sometimes. You're not alone in feeling confused!

Payday Loans 101: A Quick Refresher

First things first, let's get on the same page. What exactly is a payday loan? Well, it's a short-term, high-interest loan, usually for a small amount, intended to be repaid on your next payday. They're often marketed as a quick and easy solution for unexpected expenses. Think of them as a financial band-aid, but one that can potentially rip off a lot of hair when you remove it... if you're not careful.

Must Read

- Short-term: We're talking weeks, not months or years.

- High-interest: Brace yourself. These rates can be eye-watering. Seriously, do your research!

- Small amount: Usually a few hundred dollars. Enough to cover a minor emergency, but not a major financial crisis.

- Payday repayment: The loan is due on your next payday. Miss that date, and things can get ugly fast.

The appeal is obvious: quick cash, no credit check required (often!). But that convenience comes at a price. And part of that price could be your credit score. Dun dun DUN!

Credit Reports: The Good, The Bad, and The Ugly

Now, let's talk about credit reports. These are essentially detailed records of your credit history, maintained by credit bureaus like Experian, Equifax, and TransUnion. They contain information about your credit accounts, payment history, and any public records like bankruptcies. Think of it as your financial resume. Lenders use these reports to assess your creditworthiness – your ability to repay borrowed money. A good credit report = lower interest rates and better loan terms. A bad credit report? Well, let's just say it's not a party.

Fun fact: Did you know you're entitled to a free copy of your credit report from each of the major credit bureaus once a year? Take advantage of it! Knowledge is power, people!

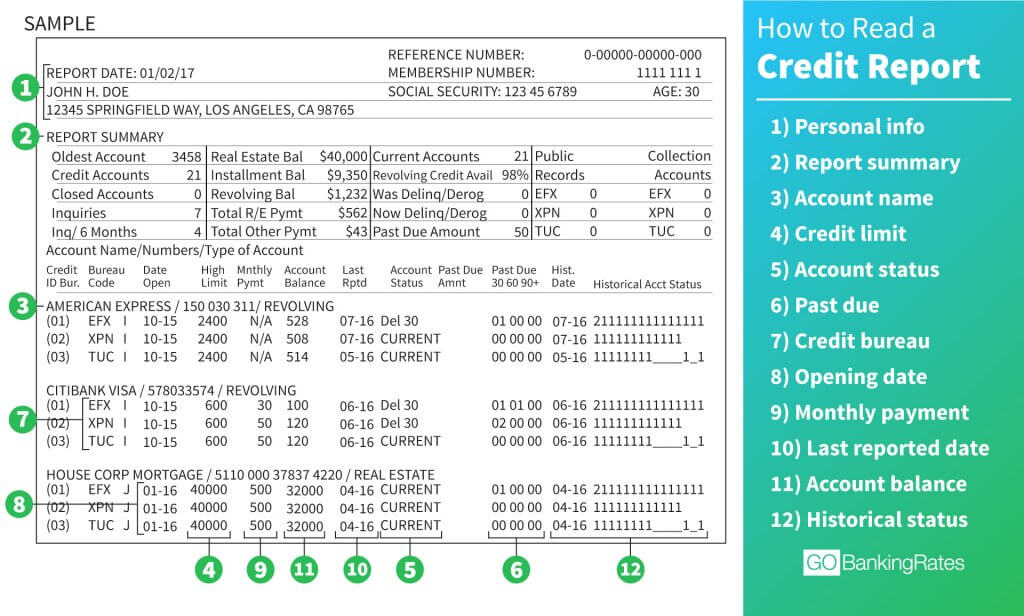

What goes on a credit report? Here's a brief rundown:

- Personal information: Name, address, Social Security number, etc. (Make sure it's accurate!)

- Credit accounts: Credit cards, loans, mortgages – anything you've borrowed money for.

- Payment history: This is HUGE. Do you pay your bills on time? Late payments ding your score.

- Credit utilization: How much of your available credit are you using? Maxing out your cards is a big no-no.

- Public records: Bankruptcies, foreclosures, judgments – things you definitely want to avoid.

- Inquiries: Every time you apply for credit, it generates an inquiry on your report. Too many inquiries in a short period can lower your score.

The Connection: Do Payday Loans Show Up?

Here's the million-dollar question: Will taking out a payday loan automatically trash your credit score? The (frustratingly) nuanced answer is: not directly, usually.

Most traditional payday lenders don't report to the major credit bureaus. Why? Because they often cater to borrowers with less-than-stellar credit, and reporting to the credit bureaus would require them to adhere to stricter regulations and potentially scare away customers. They operate in a slightly different realm.

So, if the payday lender doesn't report your loan, it won't show up on your credit report, right? Wrong. There's a catch (of course there is!).

The Catch: When Payday Loans Do Affect Your Credit

Even if the payday lender doesn't report to the major credit bureaus, there are still ways a payday loan can negatively impact your credit score. Here's how:

1. Failure to Repay: The Downward Spiral

This is the big one. If you fail to repay your payday loan (and let's face it, that's easier said than done with those sky-high interest rates), the lender will likely send your debt to a collection agency. And that is when things get real. Collection agencies do report to the credit bureaus. So, a previously invisible payday loan suddenly becomes a big, ugly mark on your credit report, significantly lowering your score. Think of it as a financial ghost coming back to haunt you.

Seriously, avoid this at all costs!

2. Lawsuits and Judgments: The Legal Nightmare

If the collection agency can't get you to pay, they might sue you. If they win the lawsuit, they'll obtain a judgment against you. Judgments are public records and will show up on your credit report, causing significant damage. Plus, they can garnish your wages, which is never a fun experience. Imagine explaining that to your boss! Yikes!

3. Alternative Credit Bureaus: The Hidden Threat

While most payday lenders don't report to the major credit bureaus, some may report to alternative credit bureaus, like Clarity Services or DataX. These bureaus specialize in tracking short-term, high-risk loans. While these bureaus aren't as widely used as Experian, Equifax, and TransUnion, some lenders do use them. So, even if your payday loan doesn't show up on your traditional credit report, it could still affect your ability to get other loans in the future, especially from lenders who specialize in short-term financing.

4. Bank Account Overdrafts: The Domino Effect

Often, payday lenders require access to your bank account to automatically withdraw the loan amount on your payday. If you don't have sufficient funds in your account, you'll incur overdraft fees from your bank. These fees, while not directly impacting your credit score, can quickly snowball and make it even harder to repay the payday loan, increasing the likelihood of default and ultimately leading to collection agencies and negative credit reporting.

Protecting Your Credit: A Few Words of Wisdom

So, what's the takeaway? Payday loans can indirectly affect your credit score, even if they don't always show up directly on your credit report. The key is to be responsible and avoid getting trapped in a cycle of debt.

Here are a few tips to protect your credit:

- Avoid payday loans if possible: Explore other options first, like borrowing from friends or family, negotiating with creditors, or exploring credit union loans. Trust me, your future self will thank you.

- If you must take out a payday loan, borrow only what you can afford to repay: Be realistic about your budget and ensure you have a plan to repay the loan on time.

- Pay on time, every time: This is crucial! Late payments are a credit score killer.

- Monitor your credit report regularly: Check for any errors or suspicious activity. You can get a free copy of your credit report from each of the major credit bureaus annually.

- Consider credit counseling: If you're struggling with debt, a credit counselor can help you develop a budget and explore debt management options.

The Bottom Line: Proceed with Caution

Payday loans can be a tempting quick fix, but they come with significant risks. While they may not always directly impact your credit score, the potential for negative consequences is very real. So, before you sign on the dotted line, think carefully about whether you can truly afford the loan and whether there are other, less risky options available. Your credit score (and your financial sanity) will thank you for it. Consider payday loan as a last resort, and make sure you are taking the needed precautions.

And remember, a little planning and responsible financial behavior can go a long way in building and maintaining a healthy credit score. Good luck out there!

/CreditReport_SpiffyJ_E--56a1deaa5f9b58b7d0c4000c.jpg)