Do I Need Flood Insurance In Florida

Alright, settle in, grab your iced coffee (or maybe something a little stronger, depending on how your last hurricane season went), because we're about to tackle a topic that's drier than a saltine cracker but more important than your sunscreen collection: Flood insurance in Florida. Now, I know what you're thinking: "Ugh, insurance. Snoozeville." But trust me, this is a story worth hearing, especially if you own property in the Sunshine State. Think of it as a disaster preparedness comedy, with you playing the starring role of the savvy homeowner who's totally got this.

The Big Question: To Flood or Not to Flood (Insurance-wise, That Is)

So, do you need flood insurance in Florida? Short answer: Probably. Long answer: Picture this: you're relaxing on your porch, sipping sweet tea, when suddenly, BAM! A rogue wave (okay, maybe not a rogue wave, but definitely a significant amount of water) decides your living room is its new vacation destination. Is your homeowner's insurance going to cover that delightful indoor swimming pool situation? Nope. Nada. Zilch. Homeowner's insurance typically covers things like fire, theft, and maybe that time a squirrel decided to remodel your attic. But flood? That's a whole different ballgame.

Think of homeowner’s insurance as your basic defense, like a butter knife in a sword fight. Flood insurance? That's your bazooka. You might not need it every day, but when you do, you'll be really glad you have it.

Must Read

But I Don't Live Near the Ocean!

Ah, the classic misconception! Look, Florida is basically a giant sponge. Even if you're miles inland, nestled amongst orange groves and confused tourists, you're still at risk. We're talking heavy rainfall, overflowing rivers, drainage issues that would make an engineer weep, and the occasional sinkhole that opens up like a surprise party you definitely didn't RSVP to. Basically, water finds a way.

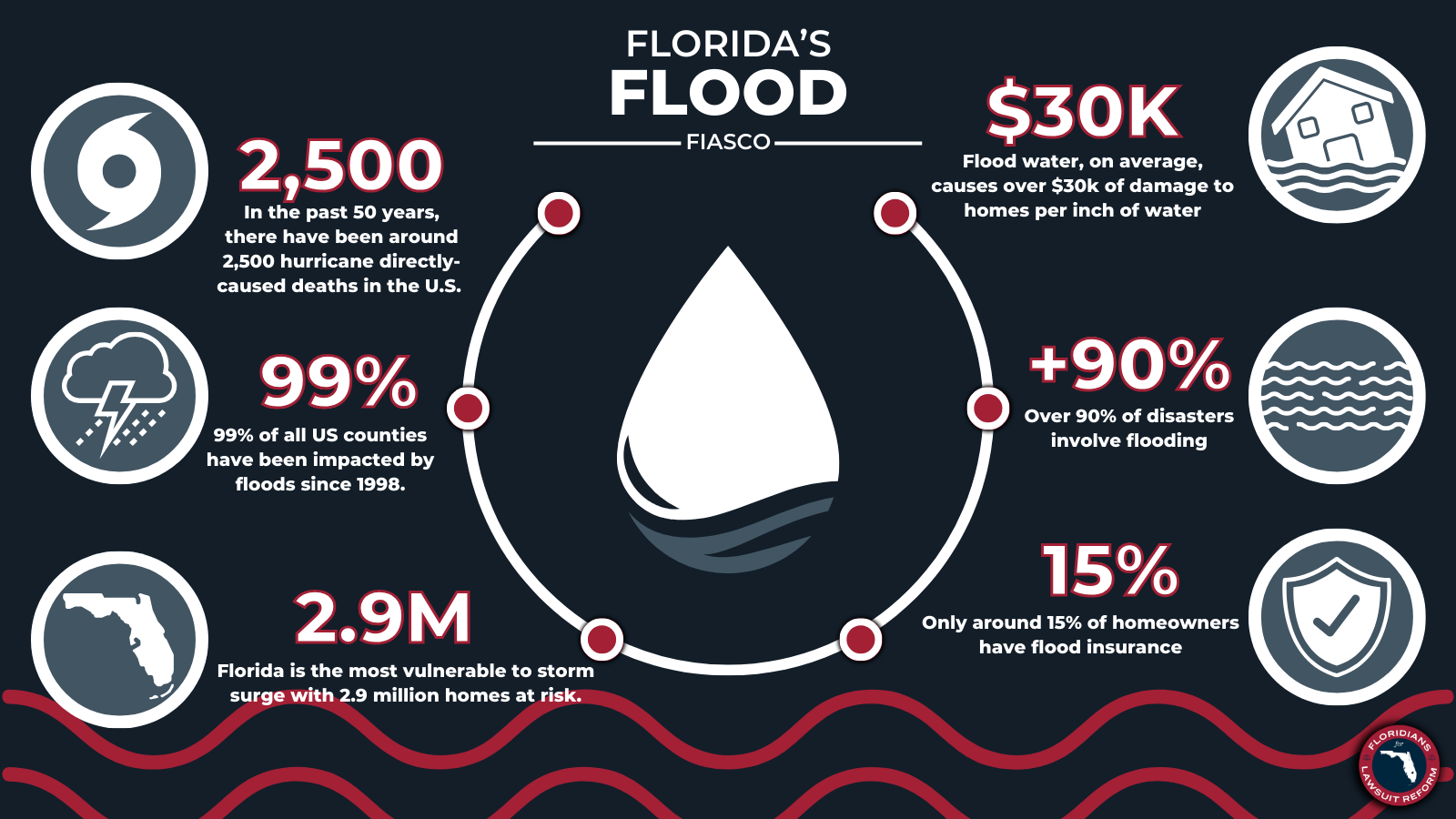

A surprising fact: More than 20% of flood claims come from areas considered low-risk. Twenty percent! That's like saying 20% of unicorns wear tiny hats. Unexpected, right?

Understanding Flood Zones: It's Not Just About Being Waterfront

Alright, let's talk flood zones. The Federal Emergency Management Agency (FEMA) has meticulously mapped out areas based on their flood risk. These zones range from high-risk (think beachfront property that's practically begging to be submerged) to low-risk (think… well, think somewhere that still probably needs flood insurance, because, Florida).

Here's a simplified breakdown:

- High-Risk Zones (e.g., Zones AE, VE): These are areas with a 1% or greater chance of flooding in any given year. Sounds small, right? But over the life of a 30-year mortgage, that's a 26% chance! If you're in one of these zones and have a mortgage from a federally regulated lender, flood insurance is mandatory.

- Moderate-Risk Zones (e.g., Zones B, X): These areas have a lower, but still present, risk of flooding. Flood insurance isn't federally required, but it's strongly recommended. Think of it as preventative medicine for your wallet.

- Low-Risk Zones (e.g., Zone C, X): Even in these zones, flooding is still possible. While not federally mandated, you can still purchase flood insurance, and it's often cheaper than in higher-risk zones. Don't be fooled by the "low-risk" label – it doesn't mean "no risk."

How do you find your flood zone? Great question! You can check FEMA's Flood Map Service Center online. Just type in your address, and it will tell you your flood zone designation. It's like a treasure map, except instead of gold, you're finding out how likely your house is to become an impromptu swimming pool.

The Cost of Not Having Flood Insurance: A Horror Story (But Hopefully Not Your Story)

Let's say you decide to roll the dice and skip the flood insurance. "It'll never happen to me!" you declare confidently, right before the heavens open up and your living room transforms into a murky lagoon. Now what?

Well, here's the grim reality. Without flood insurance, you're on the hook for all the damages. We're talking:

- Structural damage: Walls collapsing, foundations cracking, your house potentially deciding to relocate to a nearby canal.

- Personal property loss: Furniture floating away, electronics taking an unscheduled bath, your prized collection of porcelain cats turning into soggy lumps of clay.

- Mold: Oh, the mold. That insidious, silent killer that thrives in damp environments and makes your allergies sing opera.

The average flood claim in Florida can run into the tens of thousands of dollars. Can you afford to shell out that kind of cash out of pocket? Probably not. Even if you can, wouldn't you rather spend it on something more enjoyable, like a lifetime supply of key lime pie?

Getting Flood Insurance: It's Easier Than You Think (Probably)

Okay, so you're convinced. You need flood insurance. Now what? Fortunately, getting flood insurance isn't as painful as, say, wrestling an alligator. (Please don't wrestle alligators.)

Here are your main options:

- The National Flood Insurance Program (NFIP): This is a federal program administered by FEMA. It's the most common way to get flood insurance. You can purchase NFIP coverage through most insurance companies.

- Private Flood Insurance: This is an alternative to the NFIP. Private insurers may offer different coverage options, limits, and prices. Shop around to see what works best for you.

The cost of flood insurance varies depending on several factors, including:

- Your flood zone: Higher-risk zones generally have higher premiums.

- Your property's elevation: A house built on stilts (or pilings, if you want to be fancy) will typically have lower premiums than a house at ground level.

- Your coverage amount: The more coverage you buy, the more you'll pay.

- Your deductible: A higher deductible means lower premiums, but it also means you'll have to pay more out of pocket if you file a claim.

Talk to your insurance agent to get a quote and find the best coverage for your needs. And don't be afraid to ask questions! They're there to help you navigate the murky waters of flood insurance. (Pun intended.)

Final Thoughts: Don't Be a Florida Flood Statistic

Look, Florida is an amazing place to live. Sunshine, beaches, theme parks, questionable fashion choices… we've got it all! But we also have hurricanes, heavy rainfall, and a landscape that's basically begging to be flooded. Don't let a flood wipe out your savings and turn your dream home into a watery nightmare.

Investing in flood insurance is an investment in your peace of mind. It's like having a superhero on standby, ready to swoop in and save the day (or at least your bank account) when disaster strikes. So, do yourself a favor and get covered. You'll thank yourself later, especially when you're watching the news and feeling smugly secure while everyone else is scrambling to bail out their flooded living rooms with buckets and a whole lot of regret.

Now go forth, Floridians, and conquer the world… or at least protect your home from the next big rainstorm. And remember, always keep a kayak handy, just in case!