Do I Get My Husband's Social Security When He Dies

So, your amazing husband, the king of the grill and master of the remote, is thinking about the future (as he should!). And maybe, just maybe, you’re wondering what happens to his Social Security when he, heaven forbid, kicks the bucket. Let’s dive into this, shall we?

The short answer? Potentially, yes! But like everything in life, it’s not quite as simple as snapping your fingers and suddenly swimming in Social Security checks. Think of it more like winning a mini-lottery – there are some rules to play by.

Widow(er)'s Benefits: Your Social Security Safety Net

The Social Security Administration (SSA) has something called widow(er)'s benefits. It's basically a safety net designed to help surviving spouses after their partner passes away.

Must Read

It’s not just for widows, mind you! Widowers, we see you and your amazing beards! These benefits are available to both, regardless of gender.

Am I Eligible for These Magical Benefits?

Okay, so you're thinking, "Sounds fantastic! Sign me up!" Hold your horses (or unicorns, whatever you prefer). There are a few boxes you need to tick before you qualify for widow(er)'s benefits.

First, you and your dearly departed (but hopefully not for a long time!) must have been married for at least nine months. Think of it as a Social Security "trial period" – gotta make sure it's the real deal!

There are exceptions, of course. If you have a child together, that marriage length requirement is generally waived. Also, if his death was accidental or occurred in active military service, the nine-month rule is out the window.

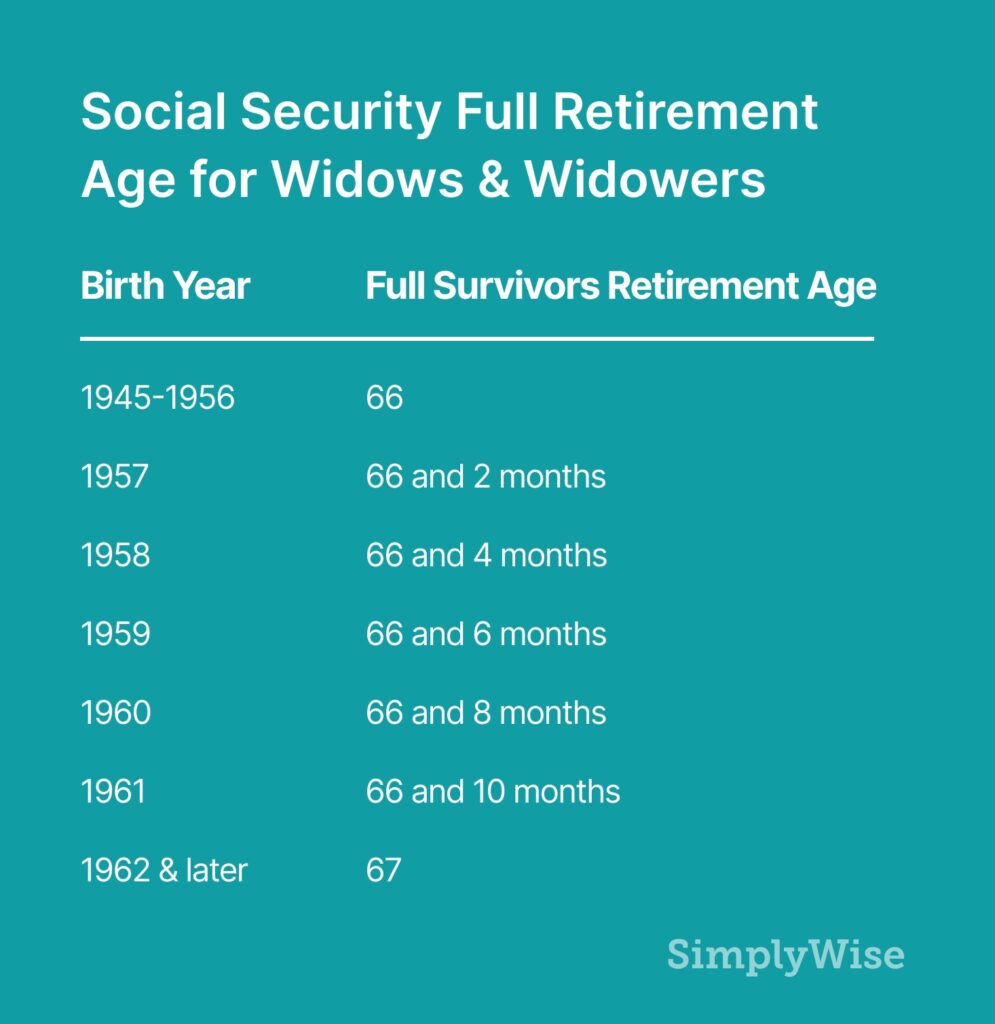

Second, you need to be a certain age. Generally, you can start receiving benefits as early as age 60. But here’s the kicker: if you start before your full retirement age (which is likely 66 or 67, depending on when you were born), your benefits will be reduced. Boo!

Third, you can receive benefits at age 50 if you are disabled. The disability requirements are stringent, so make sure you meet them.

How Much Money Are We Talking About?

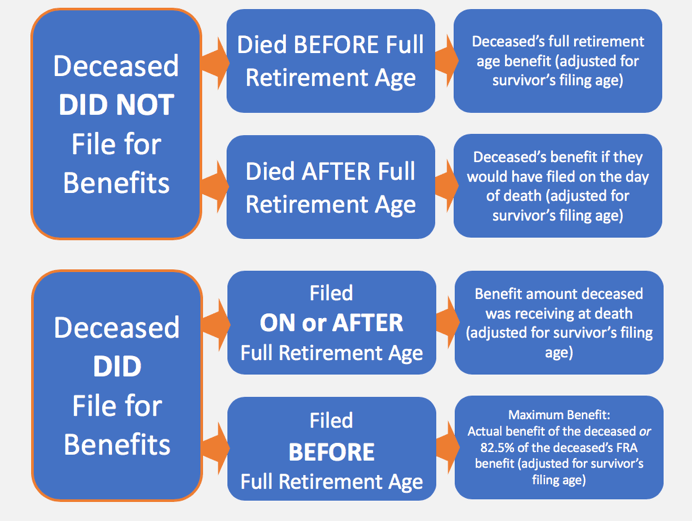

This is where it gets interesting! The amount you receive depends on a few things, most notably your husband’s earning record and when he started taking Social Security. It also depends on your age when you start receiving widow(er)'s benefits.

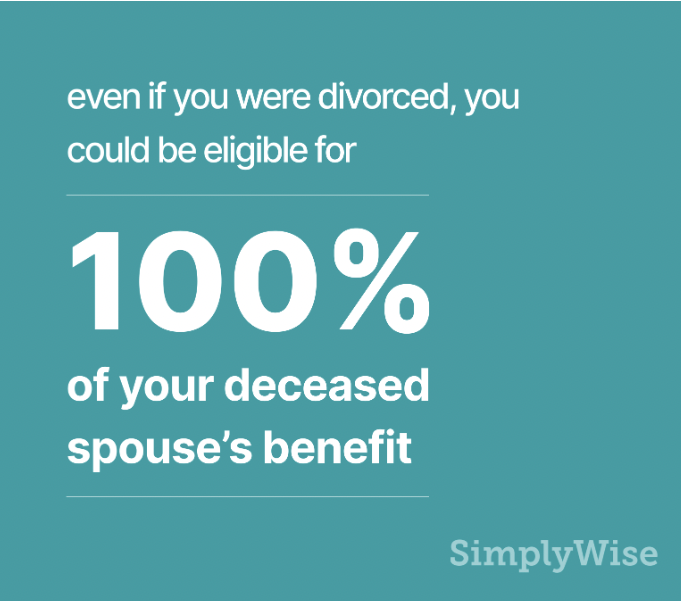

In some cases, you might even get 100% of what your husband was receiving. Imagine! But, again, that’s usually if you wait until your full retirement age. Start earlier, and you’ll get a reduced amount.

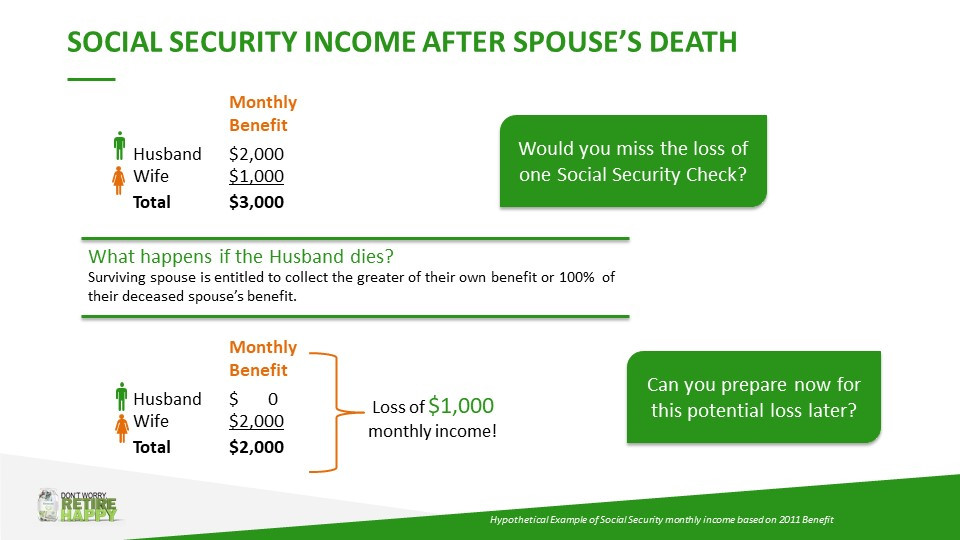

But what if you also worked and earned Social Security? This is where things get a little more complex. You can't just double-dip and get both your full benefit and his full benefit. The Social Security Administration will generally pay you whichever benefit is higher.

Let's say your benefit is $1,000 and your husband's was $1,500. You'd likely get the $1,500 (his benefit) as a widow(er). If your benefit was $2,000 and his was $1,500, you'd continue receiving your own $2,000.

Remarriage Rules: A Social Security Soap Opera!

Hold on to your hats; here comes a plot twist! If you remarry before age 60, you generally lose your widow(er)'s benefits. I know, harsh, right?

However, if you remarry after age 60 (or 50 if disabled), you can still receive benefits based on your deceased husband's record! So, go forth and find love (if that's what you want!) – just maybe wait until after your 60th birthday.

Don't Be Afraid to Ask!

The world of Social Security can feel like a confusing maze. Don't be shy about contacting the Social Security Administration directly. They're there to help (even if it sometimes feels like they’re speaking a different language).

You can visit their website (ssa.gov) or call them directly. Just be prepared for a potentially long wait time – maybe grab a good book and a cup of tea.

Remember, planning for the future isn't morbid; it's responsible. By understanding your potential widow(er)'s benefits, you can ensure a more secure future for yourself. And that’s something to smile about! So, talk to your husband, do your research, and get ready to navigate the world of Social Security like a boss!

Disclaimer: This article is for informational purposes only and is not financial advice. Consult with a qualified professional for personalized guidance.

:max_bytes(150000):strip_icc()/social-security-survivor-benefits-for-a-spouse-2388918-v3-5bc644f846e0fb0026f5c3e2.png)