In accounting, understanding the normal balance of accounts is crucial for maintaining accurate financial records. One fundamental account is Common Stock, which represents the ownership interest in a corporation. Knowing that Common Stock has a normal credit balance is essential for properly recording transactions and preparing financial statements.

Understanding the Basic Accounting Equation

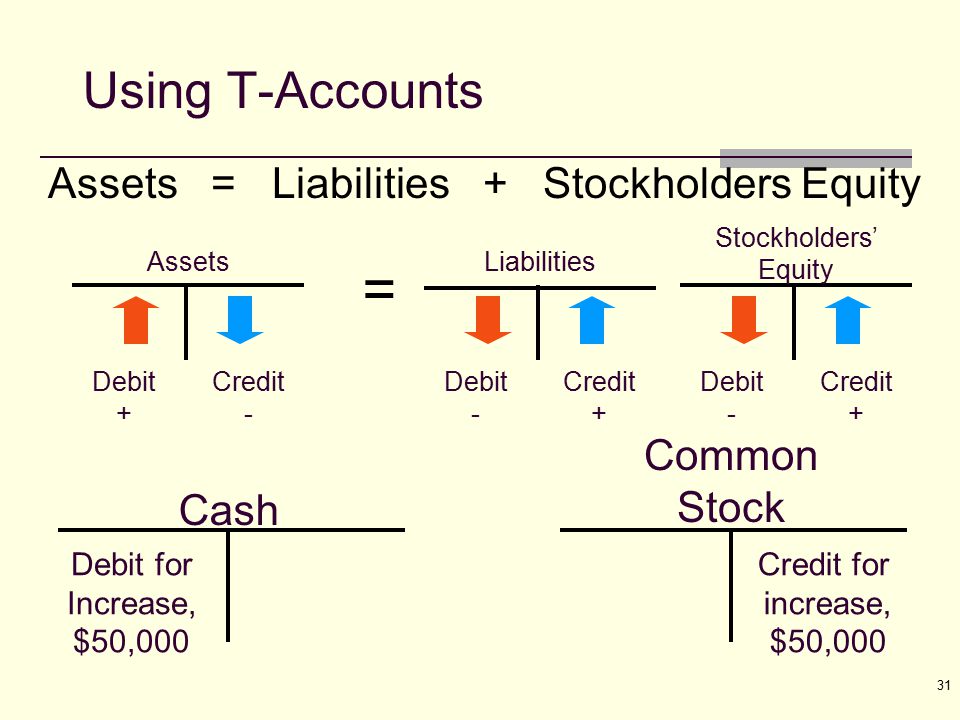

Before delving into Common Stock, it's vital to grasp the basic accounting equation: Assets = Liabilities + Equity. This equation forms the bedrock of the double-entry bookkeeping system, which mandates that every transaction affects at least two accounts. Assets represent what a company owns, liabilities represent what it owes to others, and equity represents the owners' stake in the company.

The accounting equation must always remain in balance. Any increase on one side of the equation must be offset by an equal increase on the other side, or by an equal decrease on the same side. This principle ensures that the financial records remain consistent and accurate.

The terms "debit" and "credit" are the language accountants use to record changes in accounts. They don't inherently mean "increase" or "decrease," but their effect depends on the type of account being affected. Here's a simple way to remember the rules for increases:

Assets: Increase with a Debit, Decrease with a Credit

Liabilities: Increase with a Credit, Decrease with a Debit

Equity: Increase with a Credit, Decrease with a Debit

Debits are recorded on the left side of a journal entry, and credits are recorded on the right side. For every transaction, the total debits must equal the total credits to keep the accounting equation in balance.

What is Common Stock?

Common Stock represents the basic ownership interest in a corporation. When a company issues common stock, it's essentially selling a piece of itself to investors. These investors, known as shareholders, become part-owners of the company and are entitled to certain rights, such as voting on important company matters and receiving dividends (if declared by the board of directors).

Normal Balance of Accounts | Double Entry Bookkeeping

Unlike preferred stock, which often carries a fixed dividend rate and preferential rights, common stock typically has more upside potential but also greater risk. Common stockholders are last in line to receive assets in the event of liquidation, after creditors and preferred stockholders have been paid.

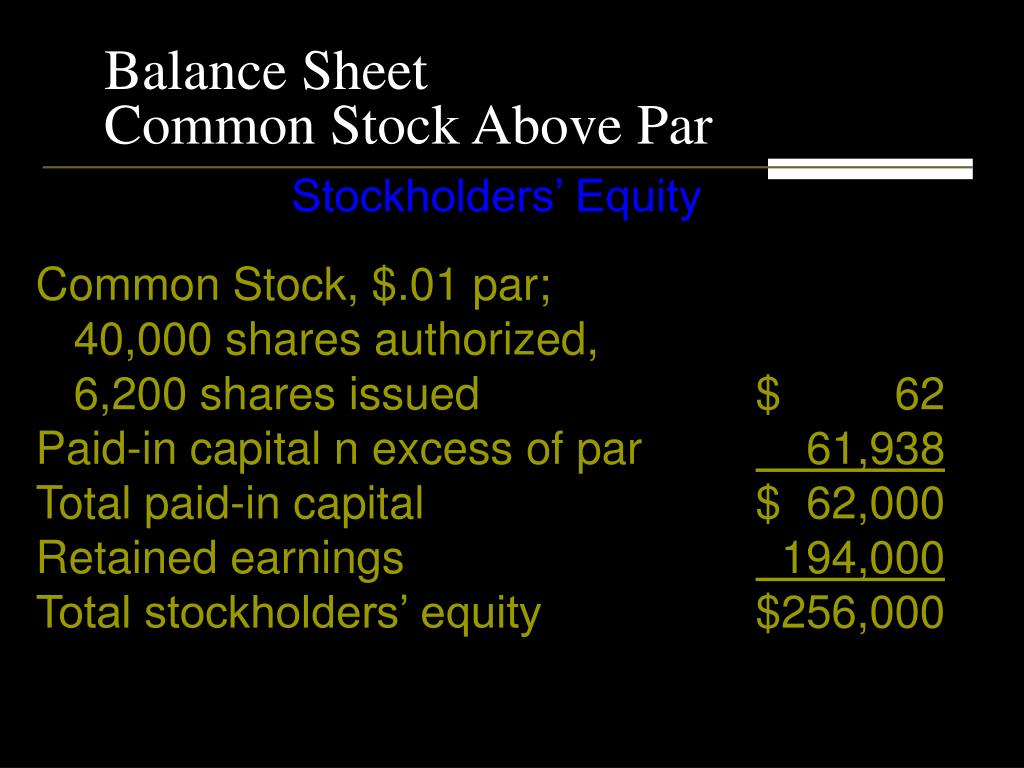

The Common Stock account on the balance sheet represents the total par value of the shares issued. Par value is an arbitrary value assigned to each share of stock in the company's charter. It's usually a nominal amount (e.g., $0.01 per share).

Additional Paid-In Capital

Often, shares are sold for more than their par value. The amount above the par value is recorded in an account called Additional Paid-In Capital (APIC). For instance, if a company sells 1,000 shares of common stock with a par value of $1 per share for $10 per share, the Common Stock account is credited for $1,000 (1,000 shares x $1 par value), and the Additional Paid-In Capital account is credited for $9,000 (1,000 shares x ($10 - $1)).

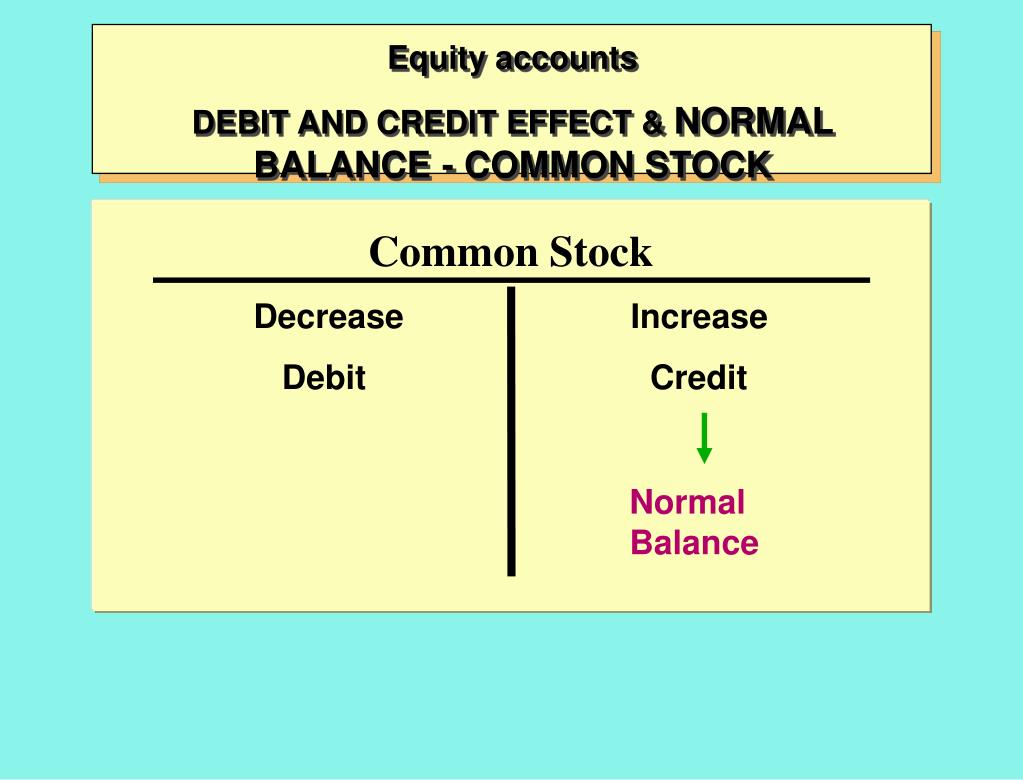

The Normal Balance of Common Stock: A Credit

Common Stock is an equity account. As mentioned earlier, equity accounts increase with credits and decrease with debits. Therefore, the normal balance of Common Stock is a credit. This means that when a company issues new shares of common stock, the Common Stock account is credited to reflect the increase in equity.

Common Stock Formula | Calculator (Examples with Excel Template)

Think of it this way: When a company sells stock, it receives cash (an asset), and in exchange, it gives up a portion of its ownership (equity). The increase in cash is recorded as a debit, and the increase in equity (represented by the Common Stock account) is recorded as a credit, maintaining the balance of the accounting equation.

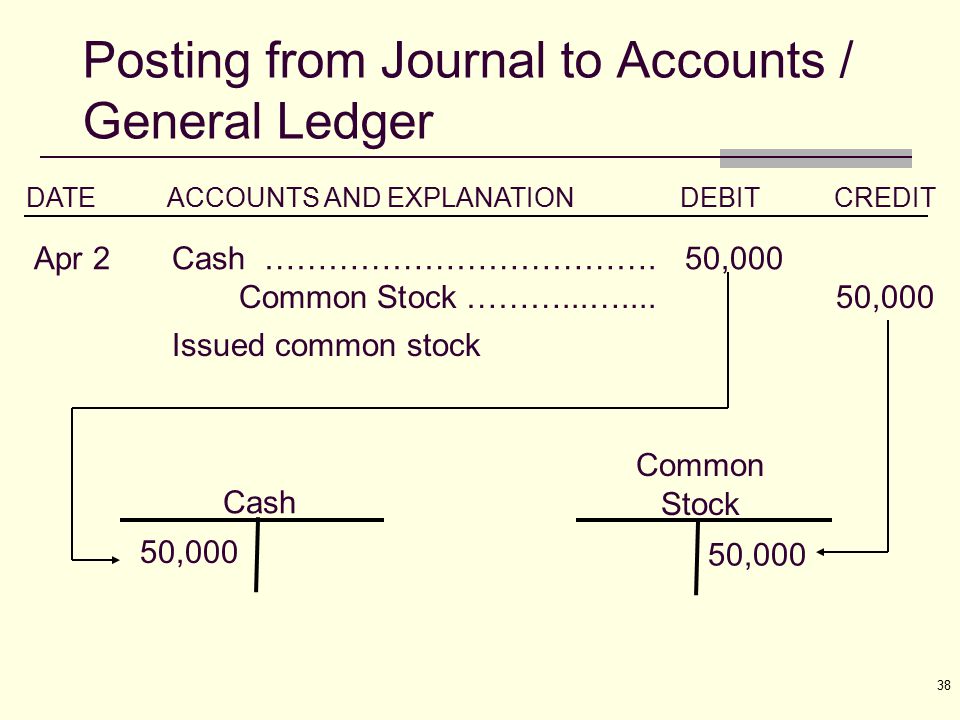

Example Journal Entry

Let's illustrate with an example. Suppose a company issues 5,000 shares of common stock with a par value of $0.50 per share for $8 per share. The journal entry would be:

Debit: Cash $40,000 (5,000 shares x $8)

Credit: Common Stock $2,500 (5,000 shares x $0.50)

[Solved] The following table summarizes the rules | SolutionInn

Credit: Additional Paid-In Capital $37,500 (5,000 shares x ($8 - $0.50))

In this entry, Cash (an asset) is debited to show the increase in the company's cash balance. Common Stock (an equity account) is credited to show the increase in the par value of issued shares. Additional Paid-In Capital is also credited to account for the amount received above the par value. The total debits ($40,000) equal the total credits ($2,500 + $37,500 = $40,000), ensuring the accounting equation remains balanced.

Why Understanding the Normal Balance Matters

Knowing that Common Stock has a normal credit balance is critical for several reasons:

Accurate Financial Reporting: Incorrectly recording transactions involving Common Stock can distort the balance sheet and other financial statements, leading to inaccurate portrayals of the company's financial position.

Error Detection: Understanding normal balances helps in identifying errors. If the Common Stock account has a debit balance (which is unusual), it signals a potential mistake that needs to be investigated.

Proper Journal Entries: When preparing journal entries, knowing the normal balance helps you determine whether to debit or credit the Common Stock account, ensuring the accounting equation remains in balance.

Financial Analysis: Stakeholders, including investors, creditors, and management, rely on accurate financial statements to make informed decisions. Misstating the Common Stock balance can lead to flawed analysis and poor decision-making.

Maintaining the Accounting Equation: The entire accounting system relies on the accurate application of debits and credits. Erroneously using the debit/credit rules for Common Stock throws off the accounting equation and results in inaccurate financial statements.

For example, imagine a company incorrectly debits the Common Stock account when issuing new shares. This would understate the company's equity and overstate its assets, leading to an inaccurate balance sheet. Investors relying on this information might underestimate the company's value and make incorrect investment decisions.

PPT - Acct 310 Accounting Review Part I PowerPoint Presentation, free

Exceptions and Considerations

While Common Stock typically has a credit balance, there can be scenarios where the balance is reduced or even temporarily shows a debit impact. This most commonly occurs through treasury stock transactions.

Treasury Stock

Treasury stock refers to shares of a company's own stock that it has repurchased from the open market. When a company buys back its own stock, it decreases both assets (cash) and equity. The Treasury Stock account is a contra-equity account, meaning it reduces the overall equity of the company. The purchase of treasury stock is recorded with a debit to Treasury Stock. While the Common Stock account itself usually maintains its credit balance (representing the total number of shares issued), the Treasury Stock account effectively offsets a portion of that equity.

When treasury stock is resold, the Treasury Stock account is credited, increasing equity again. This does not directly impact the Common Stock account unless new shares are issued beyond the initially authorized amount.

Conclusion

In summary, Common Stock represents the ownership interest in a corporation and has a normal credit balance. This means that increases in Common Stock are recorded as credits. Understanding this fundamental principle is essential for maintaining accurate financial records, detecting errors, and ensuring the proper application of accounting principles. By correctly recording transactions related to Common Stock, companies can provide reliable financial information to stakeholders, enabling them to make informed decisions. A clear understanding of the normal balance of Common Stock, and how it interacts with related accounts like Additional Paid-In Capital and Treasury Stock, is crucial for anyone involved in accounting or financial analysis.

![[Solved] The following table summarizes the rules | SolutionInn](https://s3.amazonaws.com/si.question.images/images/question_images/1564/4/8/2/6285d401c448a62e1564465762716.jpg)

:max_bytes(150000):strip_icc()/dotdash_Final_Common_Stock_2020-01-03fbeb0664c74b71aa025dcfd7661c82.jpg)