Coastal Credit Union Money Market Rates

Okay, so picture this: I'm cleaning out my junk drawer (we all have one, right? Don't lie!), and I stumble across a stack of old birthday cards. Grandparents are generous. Inside, nestled amongst the glitter and questionable life advice, are checks. Real, actual, uncashed checks. Some dating back to... well, let's just say Y2K was a thing. Panic ensues. After a flurry of mobile deposits (and a minor heart attack when one bounced because, apparently, my grandma decided to switch banks 15 years ago), I’m suddenly flush. Flush-ish. Enough to make me think, "Okay, where's the smartest place to put this so it doesn't just... vanish?"

That’s when I started diving deep into the wonderful (and sometimes terrifying) world of savings. And that’s also when I stumbled upon the alluring promise of money market accounts. And, being a local myself, naturally, I looked into Coastal Credit Union. So, let's talk Coastal Credit Union money market rates, shall we? Because who doesn't want their money to work a little harder, right?

What Exactly Is a Money Market Account? (And Why Should I Care?)

Alright, before we dive into the specifics of Coastal, let's quickly level-set. A money market account (MMA) is basically a hybrid. It's not quite a savings account, but it's also not quite an investment account. Think of it as a souped-up savings account. (Side note: "Souped-up" is a highly technical financial term. Just kidding. Sort of.)

Must Read

Here's the deal:

- Higher Interest Rates: Generally, MMAs offer higher interest rates than traditional savings accounts. This is the main draw! You're getting a better return on your cash just sitting there.

- FDIC Insured: Like savings accounts at most banks and credit unions, your money in a Coastal Credit Union MMA is typically FDIC insured up to $250,000 per depositor, per insured bank. (Double check on Coastal's site for their specific insurance.) This means your money is safe(ish). (Okay, very safe, as long as you stay under that limit.)

- Limited Transactions: MMAs typically have limits on the number of withdrawals and transfers you can make per month. This isn't a checking account; they don't want you using it for daily purchases.

- Minimum Balance Requirements: Often (though not always), MMAs require a minimum balance to open the account or to avoid fees. Pay attention to this! Nothing is worse than getting dinged with fees that eat away at your interest.

So, why should you care? If you have a chunk of cash that you want to keep relatively safe but also want to earn more interest than you would in a regular savings account, an MMA might be a good fit. Think emergency fund, down payment savings, or, you know, accidentally discovered birthday check windfall.

Coastal Credit Union Money Market Accounts: A Closer Look

Okay, now to the juicy part: Coastal Credit Union. They’re pretty popular in the area, and I’ve heard good things about their service. But what about their MMAs? Let's investigate! (Cue dramatic music.)

Checking Coastal's Website (Because That's What Responsible Adults Do)

The first step? Head to Coastal's website. Most credit unions and banks are pretty transparent about their rates and fees. (At least, they try to be. Sometimes it feels like they're intentionally hiding it in the fine print.) Look for a "Savings" or "Deposit Accounts" section. Often, there will be a specific page dedicated to money market accounts.

When you find the MMA information, here's what you want to be on the lookout for:

- Current Interest Rates (APY): This is the most important! APY stands for Annual Percentage Yield, and it tells you how much interest you'll earn in a year, taking into account compounding. Higher APY = more money for you. (Duh.) Pay close attention to tiered rates, which we'll discuss in a bit.

- Minimum Balance Requirements: What's the minimum amount you need to open the account? What's the minimum amount you need to maintain to avoid fees or get the advertised APY?

- Fees: Are there any monthly maintenance fees? Are there fees for excessive withdrawals? Read the fine print!

- Transaction Limits: How many withdrawals or transfers can you make per month? What happens if you exceed that limit?

- How Interest is Compounded: Is it daily, monthly, quarterly? The more frequently it's compounded, the faster your money grows (though the difference might be negligible depending on the amount).

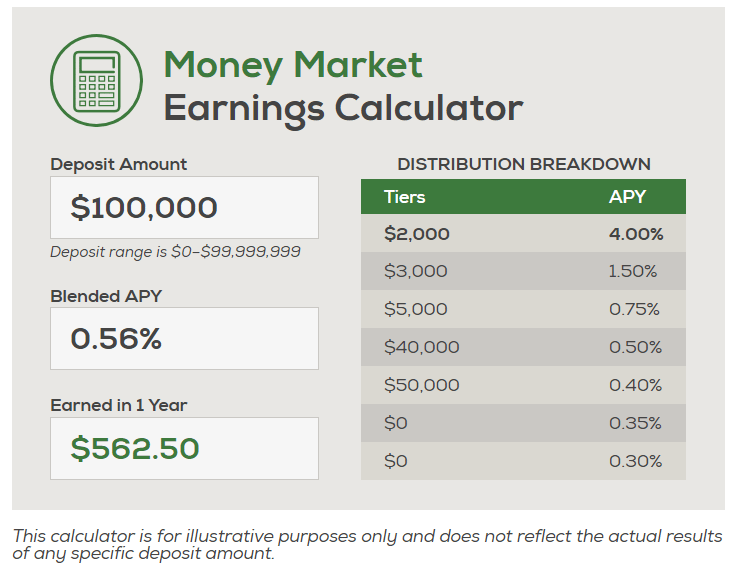

Understanding Tiered Interest Rates (The Secret Sauce)

Here's a key thing to understand about money market accounts: they often have tiered interest rates. This means the interest rate you earn depends on your account balance. The higher your balance, the higher the rate. (Makes sense, right?) It's like they're rewarding you for keeping more money with them.

For example, Coastal might have a rate structure that looks something like this (these are just examples, always check their website for the most up-to-date information!):

- Balance: $0 - $9,999: 0.50% APY

- Balance: $10,000 - $49,999: 1.00% APY

- Balance: $50,000+: 1.50% APY

See how the APY increases as your balance goes up? This is important to consider when deciding how much to deposit. If you only have $9,000, you're stuck with the lower rate. But if you can scrape together $10,000, you'll jump up to the higher rate. (Sometimes it's worth finding those extra dollars under the couch cushions!)

Pro Tip: Don't just focus on the highest advertised rate. Figure out which tier your balance will fall into and compare that rate to the rates offered by other banks and credit unions.

Comparing Coastal's MMA Rates to the Competition (The Smart Shopper's Move)

Speaking of comparing, don't just blindly trust that Coastal has the best MMA rates in town. Do your homework! (I know, it's boring. But it's also financially responsible.)

Here's how to compare:

- Online Research: Use websites like Bankrate, NerdWallet, and Deposit Accounts to compare MMA rates from different banks and credit unions. These sites often have handy comparison tools that let you filter by location and account type.

- Local Credit Unions: Don't forget to check out other local credit unions in your area. They might offer competitive rates and better customer service than the big national banks.

- Online Banks: Online banks often offer higher rates because they have lower overhead costs. However, you'll sacrifice the convenience of having a physical branch.

When comparing, make sure you're comparing apples to apples. Consider:

- Minimum Balance Requirements: Are you comparing accounts with similar minimum balance requirements?

- Fees: Are you factoring in any fees that might eat into your earnings?

- Accessibility: How easy is it to access your money? Does the bank have convenient branches or ATMs? Is their online banking platform user-friendly?

Irony Alert: Sometimes, the highest advertised rate comes with so many strings attached (high minimum balance, hefty fees, etc.) that it's not actually the best deal. Be skeptical! (But not too skeptical. Just a healthy dose.)

Beyond Interest Rates: Other Factors to Consider

Okay, so the interest rate is important, but it's not the only thing that matters. (I know, I know, you just want to find the highest rate and be done with it. But trust me, there's more to it.)

Here are some other factors to consider when choosing a Coastal Credit Union money market account (or any MMA, for that matter):

- Customer Service: How responsive and helpful is Coastal's customer service? Can you easily reach someone by phone, email, or in person if you have a question or problem? (This is especially important if you're not a financial wizard.)

- Online Banking: Is Coastal's online banking platform easy to use and secure? Can you easily transfer money, pay bills, and track your account balance?

- Mobile App: Does Coastal have a mobile app? Is it well-designed and functional? (Let's be real, we all do our banking on our phones these days.)

- Branch Access: If you prefer to bank in person, how convenient are Coastal's branch locations? Are they open during hours that work for you?

- Relationship Banking: Do you already have other accounts with Coastal? Sometimes, having a strong relationship with a bank or credit union can lead to perks like waived fees or preferential treatment.

Basically, think about the overall banking experience. A slightly lower interest rate might be worth it if you get exceptional customer service or a really user-friendly online banking platform.

Is a Coastal Credit Union Money Market Account Right for You? (The Big Question)

So, after all this, the million-dollar question (or, you know, the accidentally-discovered-birthday-check question): is a Coastal Credit Union money market account the right choice for you?

Here's a quick checklist to help you decide:

- Do you have a chunk of cash you want to keep relatively safe? If you're looking to invest in the stock market or other high-risk assets, an MMA is probably not the right choice.

- Do you want to earn more interest than you would in a traditional savings account? If you're happy with the rates you're getting in your current savings account, an MMA might not be necessary.

- Are you okay with limited withdrawals and transfers? If you need frequent access to your money, an MMA might not be the best option. A high-yield savings account might be better.

- Can you meet the minimum balance requirements? If you can't meet the minimum balance, you'll either earn a lower rate or get hit with fees.

- Have you compared Coastal's rates to the competition? Don't just assume Coastal has the best rates in town. Do your research!

- Are you happy with Coastal's customer service and online banking platform? Consider the overall banking experience, not just the interest rate.

If you answered "yes" to most of these questions, a Coastal Credit Union money market account might be a good fit for you. But ultimately, the decision is yours. (And mine, too. I'm still trying to figure out what to do with those birthday checks!)

Final Thought: Don't be afraid to ask questions! Call Coastal, talk to a representative, and get all the information you need before making a decision. They're there to help (hopefully). And remember, your financial situation is unique, so what works for one person might not work for another. Good luck with your savings journey! (And maybe check your junk drawer for forgotten treasure. You never know.)