Cash Reconciliations Can Be Tested Via

A cash reconciliation is a critical process in accounting that ensures the accuracy of a company's cash balance. It involves comparing the cash balance reported on the company's balance sheet to the corresponding information on the bank statement. Discrepancies can arise due to timing differences, errors, or even fraudulent activities. Therefore, testing the effectiveness of cash reconciliation procedures is essential for maintaining financial integrity. Several methods can be employed to test these reconciliations, providing reasonable assurance that they are performed correctly and effectively.

Understanding the Cash Reconciliation Process

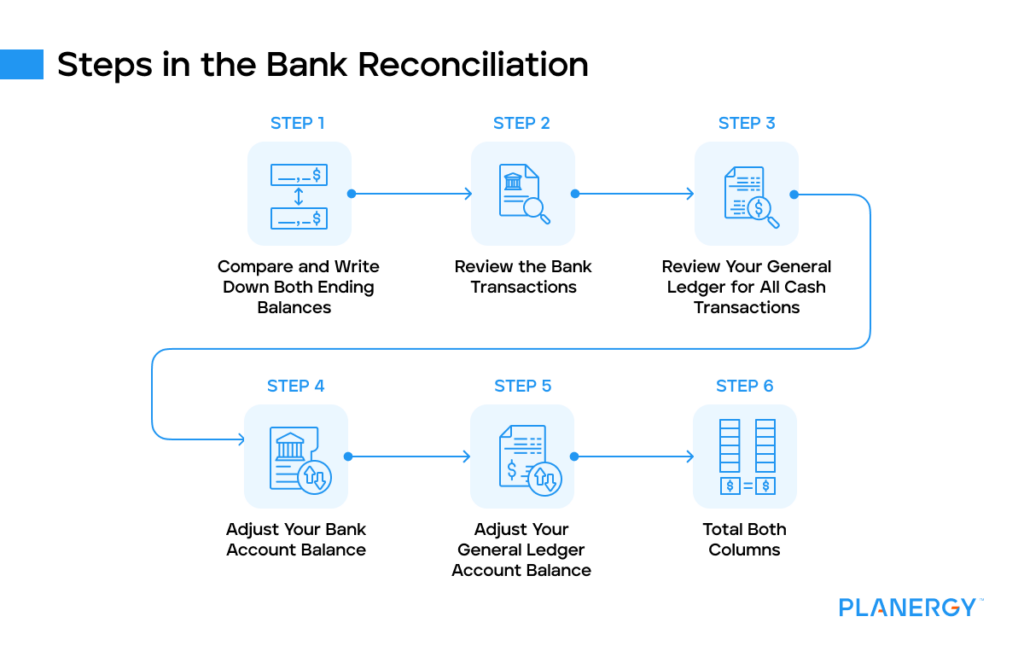

Before delving into the testing methodologies, it's vital to have a clear understanding of the cash reconciliation process itself. Typically, it involves the following steps:

- Obtaining the Bank Statement: This is the official record of all transactions that have occurred in the company's bank account during a specific period.

- Obtaining the General Ledger Cash Balance: This represents the company's internal record of cash transactions.

- Identifying Reconciling Items: These are items that cause differences between the bank statement and the general ledger cash balance. Common reconciling items include:

- Outstanding Checks: Checks issued by the company but not yet cashed by the payee.

- Deposits in Transit: Deposits made by the company but not yet credited by the bank.

- Bank Charges: Fees charged by the bank that the company may not be aware of until receiving the bank statement.

- Bank Credits: Deposits made directly into the company's account by customers or other parties that the company may not be aware of until receiving the bank statement.

- Errors: Mistakes made by either the bank or the company in recording transactions.

- Preparing the Reconciliation: This involves adjusting either the bank balance or the book balance (or both) to arrive at an adjusted cash balance. The goal is to ensure that the adjusted bank balance and the adjusted book balance agree.

- Review and Approval: A designated individual should review the reconciliation for accuracy and completeness, and then approve it.

Testing Methodologies for Cash Reconciliations

Several techniques can be utilized to test the effectiveness of cash reconciliation processes. These tests can be performed by internal auditors, external auditors, or even management personnel responsible for oversight.

Must Read

1. Review of Reconciliation Documentation

This is a fundamental step in testing cash reconciliations. It involves examining the reconciliation documents to assess their completeness, accuracy, and compliance with established procedures.

Testing Steps:

- Verify completeness: Ensure that all necessary supporting documentation, such as bank statements and general ledger reports, are included.

- Examine the reconciliation format: Assess whether the reconciliation follows a standard format and includes all essential elements, such as the beginning balances, reconciling items, and adjusted balances.

- Trace reconciling items: Trace selected reconciling items from the reconciliation to their supporting documentation (e.g., tracing outstanding checks to copies of the checks, tracing deposits in transit to deposit slips).

- Verify calculations: Recalculate the reconciliation to ensure that the mathematical calculations are accurate.

- Review for unusual or significant items: Identify any unusual or significant reconciling items that warrant further investigation.

- Inspect the approval process: Verify that the reconciliation has been reviewed and approved by a designated individual.

2. Testing the Existence of Reconciling Items

This test focuses on verifying the existence of reconciling items that appear on the reconciliation. This helps to confirm that the items are legitimate and not fictitious.

Testing Steps:

- Outstanding Checks: Select a sample of outstanding checks from the reconciliation and trace them to the subsequent month's bank statement to verify that they cleared. If a check remains outstanding for a prolonged period (e.g., six months), investigate the reason and consider writing it back into the general ledger.

- Deposits in Transit: Select a sample of deposits in transit from the reconciliation and trace them to the subsequent month's bank statement to verify that they were credited.

- Bank Charges and Credits: Examine the bank statement to verify the existence and accuracy of bank charges and credits recorded on the reconciliation. Ensure that these items are properly reflected in the general ledger.

- Investigate unusual items: Thoroughly investigate any unusual or large reconciling items to determine their nature and validity.

3. Testing the Completeness of Reconciling Items

This test aims to ensure that all reconciling items are identified and included on the reconciliation. It's designed to detect any omissions that could lead to an inaccurate cash balance.

Testing Steps:

- Review bank statement activity: Examine the bank statement for any transactions that have not been recorded in the general ledger. This could include direct debits, direct credits, or bank charges.

- Review general ledger activity: Examine the general ledger for any cash transactions that have not been reflected on the bank statement, such as outstanding checks or deposits in transit.

- Perform a cutoff test: Compare transactions recorded shortly before and after the reconciliation date to ensure that they have been recorded in the correct period. This is particularly important for outstanding checks and deposits in transit.

- Analyze prior period reconciliations: Review prior period reconciliations to identify any recurring reconciling items that may indicate a systemic issue.

4. Substantive Testing of Cash Balances

This involves directly verifying the ending cash balance with the bank. This provides independent confirmation of the accuracy of the reported cash balance.

Testing Steps:

- Obtain a bank confirmation: Send a bank confirmation request directly to the bank to confirm the ending cash balance as of the reconciliation date. The bank confirmation should be sent directly to the auditor or tester, not to the company.

- Compare the bank confirmation to the reconciliation: Compare the ending cash balance reported on the bank confirmation to the ending cash balance reported on the reconciliation. Investigate any discrepancies.

- Perform a bank reconciliation independently: Independently prepare a bank reconciliation using the bank statement and the general ledger. Compare this independent reconciliation to the company's reconciliation.

5. Evaluating the Internal Controls Over Cash Reconciliations

This involves assessing the effectiveness of the internal controls designed to prevent and detect errors in the cash reconciliation process.

Testing Steps:

- Review the company's policies and procedures: Examine the company's written policies and procedures for cash reconciliations to ensure that they are comprehensive and up-to-date.

- Observe the reconciliation process: Observe the individuals performing the cash reconciliation to assess whether they are following the established policies and procedures.

- Inquire of management and staff: Inquire of management and staff about their understanding of the cash reconciliation process and their roles in ensuring its accuracy.

- Test the segregation of duties: Verify that there is adequate segregation of duties between the individuals who handle cash, record cash transactions, and prepare cash reconciliations.

- Test the approval process: Verify that all cash reconciliations are reviewed and approved by a designated individual.

Practical Advice and Insights

The principles of cash reconciliation, and the importance of verifying financial data, extend beyond the realm of corporate accounting. In everyday life, similar concepts can be applied to manage personal finances effectively.

- Regularly reconcile your bank statements: Just as companies reconcile their bank statements, individuals should regularly reconcile their personal bank statements to identify any unauthorized transactions, errors, or discrepancies.

- Keep accurate records of your spending: Maintaining accurate records of your income and expenses allows you to track your cash flow and identify areas where you can save money.

- Monitor your credit card statements: Regularly review your credit card statements for any fraudulent activity or unauthorized charges.

- Be vigilant about online security: Protect your personal financial information by using strong passwords, avoiding phishing scams, and monitoring your credit report regularly.

By applying these principles, individuals can gain better control over their finances and minimize the risk of financial fraud or errors.