Can You Spend Money After 341 Meeting

So, you've braved the 341 meeting? Phew! That's a big step in bankruptcy. You're probably wondering... now what? Specifically, can you, like, finally buy that giant inflatable unicorn you've been eyeing?

Let's dive into the wonderful world of post-341 spending. Think of it as navigating a financial maze. Fun, right? (Okay, maybe not always fun.)

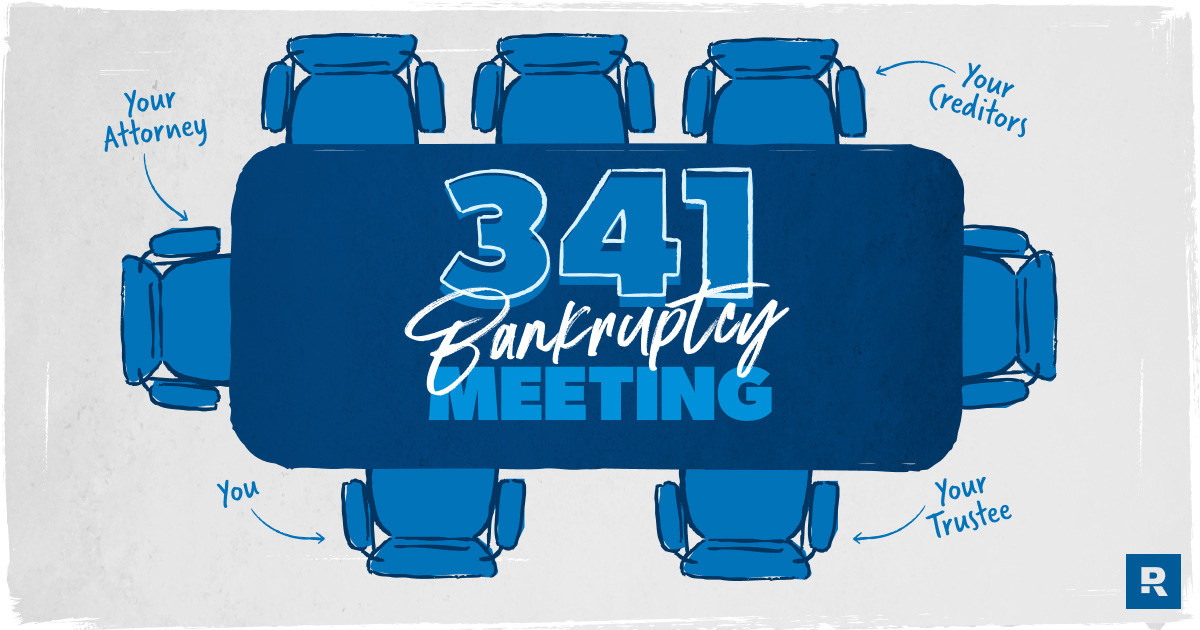

What's the 341 Meeting, Anyway?

First, a quick recap. The 341 meeting, also known as the meeting of creditors, is where you, the debtor, meet with your creditors (the people you owe money to) and a trustee. It's basically a Q&A session about your finances.

Must Read

Think of it like a job interview, but for your money woes. Except, instead of showcasing your skills, you're explaining your debt. Not exactly a party, but hey, you got through it!

The Big Question: Spend or Save?

Alright, the suspense is killing us (and probably you too). Can you spend money after the 341 meeting? The short answer: it depends.

Yep, the lawyer's favorite phrase. But bear with us! It's not entirely murky.

Here’s the thing: the 341 meeting isn't the end of your bankruptcy case. It’s just one stage in the process. You're still under the watchful eye of the court.

What Influences Your Spending Freedom?

Several factors come into play. Let’s break them down into bite-sized chunks:

- Type of Bankruptcy: Chapter 7 vs. Chapter 13 makes a HUGE difference.

- Your Budget: Are you sticking to it? The trustee will want to see responsible behavior.

- The Trustee: This person is in charge of your case. What do they say? Listen to them!

- Unexpected Windfalls: Did you suddenly win the lottery? (Hey, it could happen!) That changes things.

Let's say you're in Chapter 7. Generally, after the 341 meeting, you can spend money. But! Avoid major purchases or taking on new debt. Why? Because anything you acquire could potentially be considered part of your bankruptcy estate until your case is officially discharged. This is especially true if the Trustee still has concerns.

Now, if you're in Chapter 13, things are a bit different. You're likely on a repayment plan. Sticking to your budget is crucial. New, significant spending can throw a wrench into your plan and potentially jeopardize your bankruptcy.

The "Giant Inflatable Unicorn" Rule

Okay, there's no actual "Giant Inflatable Unicorn Rule," but it's a good example. Think about it. Is buying a massive, sparkly unicorn really the wisest financial decision right now? Probably not.

The key is to exercise restraint and common sense. Think of this period as financial training. You're building new, healthier habits.

Talking to the Professionals

Seriously, talk to your attorney. They know the specifics of your case inside and out. They can give you tailored advice based on your situation.

Don't rely solely on internet articles (even this delightfully informative one!). Your lawyer is your financial guru during this time.

Building a Brighter Financial Future

Bankruptcy can be tough. But it’s also an opportunity for a fresh start. Use this time to learn about budgeting, saving, and responsible spending.

Think of your post-341 meeting life as a financial reboot. You're wiping the slate clean and building a stronger foundation for the future.

So, can you spend money after the 341 meeting? Maybe. Carefully. Consciously. And maybe hold off on that giant inflatable unicorn... for now. Focus on building a solid financial base. You got this!

Remember, the goal isn't just to get through bankruptcy. It's to emerge stronger and more financially savvy on the other side. Now go forth and conquer your financial future (responsibly, of course)!

:max_bytes(150000):strip_icc()/GettyImages-944515884-59aab1c65c094d959db3e27bf8ebf3e2.jpg)